Key Takeaways

- LATAM's capacity expansion and strong cost management may boost revenues and improve net margins through increased demand and efficiency gains.

- Strong international bookings and a focus on sustainability can enhance revenues and brand reputation, attracting environmentally-conscious stakeholders.

- Competitive market pressures, currency depreciation, and operational challenges threaten LATAM's revenue growth and margin stability amidst economic and industry uncertainties.

Catalysts

About LATAM Airlines Group- Provides passenger and cargo air transportation services in Chile, Argentina, Peru, Colombia, Ecuador, Brazil, the United States, other Latin American countries, the Caribbean, Europe, and Oceania.

- LATAM Airlines Group anticipates continued capacity growth supported by the addition of 22 new aircraft in 2025, which is expected to increase ASKs by 7% to 9%. This expansion may boost future revenues by catering to rising demand and increasing the route offerings.

- LATAM has successfully implemented cost efficiencies, with the adjusted passenger CASK ex fuel showing competitive figures. This disciplined cost management could enhance net margins and overall earnings as capacity and efficiency improvements take effect.

- The successful refinancing exercise conducted in the fourth quarter of 2024 reduced the cost of non-fleet debt, strengthening LATAM’s balance sheet. This could improve net margins by decreasing interest expenses, positively impacting earnings.

- The international segment shows strong booking levels for the current high season, which could further increase revenues. LATAM’s diversified portfolio and flexibility in asset management help to capitalize on this strong demand environment.

- LATAM’s incorporation into the Dow Jones Sustainability Index and its focus on sustainable finance positions it as a leader in sustainability, potentially attracting more environmentally-conscious investors and customers, enhancing future revenues and brand reputation.

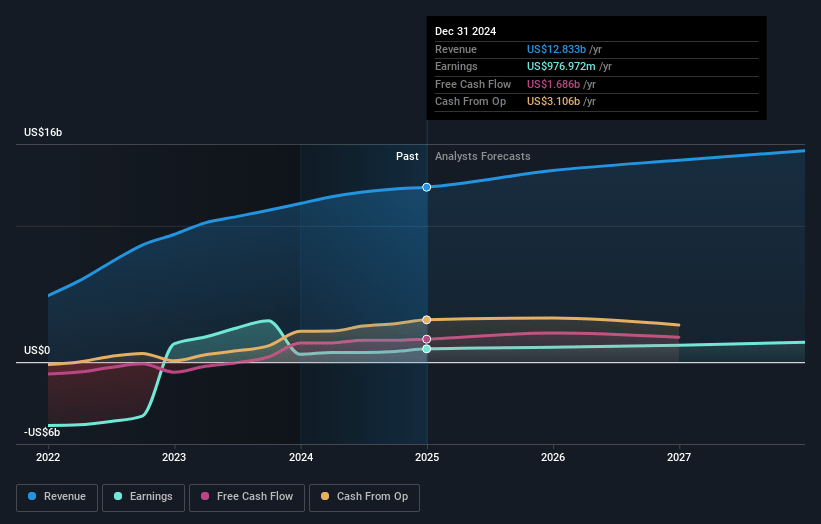

LATAM Airlines Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming LATAM Airlines Group's revenue will grow by 7.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.6% today to 8.4% in 3 years time.

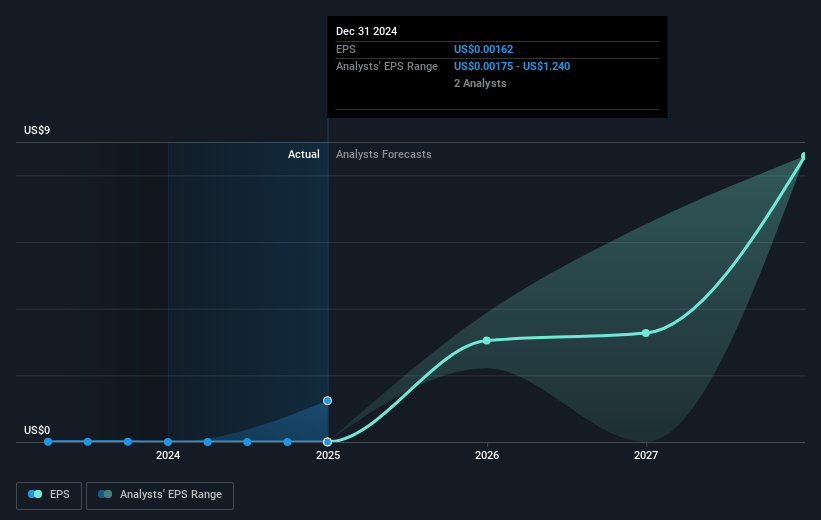

- Analysts expect earnings to reach $1.3 billion (and earnings per share of $0.0) by about March 2028, up from $977.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 13.2x on those 2028 earnings, up from 10.1x today. This future PE is greater than the current PE for the US Airlines industry at 10.1x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.24%, as per the Simply Wall St company report.

LATAM Airlines Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The depreciation of local currencies, such as the Brazilian real, could negatively impact revenues presented in USD, potentially reducing net margins and earnings if costs remain constant.

- Delays in aircraft deliveries, especially from Boeing, and issues with supply chains for engine maintenance could constrain growth plans, affecting capacity expansion and related revenue generation.

- Excessive capacity, particularly in domestic markets like Colombia, could lead to price competition and pressure on fares, impacting overall revenue and net margins.

- Potential mergers or market changes, such as the combination of Azul and Gol, might disrupt competitive dynamics in key markets like Brazil, challenging LATAM's market share and affecting revenue streams.

- Fluctuations in fuel prices and economic conditions could increase operational costs, pressuring LATAM to maintain its cost discipline to protect net margins and earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of CLP18.995 for LATAM Airlines Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CLP22.93, and the most bearish reporting a price target of just CLP15.59.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $15.8 billion, earnings will come to $1.3 billion, and it would be trading on a PE ratio of 13.2x, assuming you use a discount rate of 12.2%.

- Given the current share price of CLP14.96, the analyst price target of CLP19.0 is 21.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.