Key Takeaways

- Strategic acquisitions and investments across diverse sectors, including aviation and environmental solutions, are set to significantly boost Exchange Income's revenue and geographical reach.

- Positive market demand and operational expansions position Exchange Income for sustained growth and improved profitability, with strong contributions from Canada and international markets.

- Challenges such as trade wars, labor shortages, and political uncertainties could negatively impact operational efficiency, revenue, and profit margins for Exchange Income.

Catalysts

About Exchange Income- Engages in aerospace and aviation services and equipment, and manufacturing businesses worldwide.

- The strategic acquisition of Canadian North is a significant catalyst poised to enhance Exchange Income’s Essential Air Services business. The acquisition merges complementary routes with no overlap and includes substantial infrastructure, which should expand geographical reach and future revenue streams.

- Positive momentum in the Multi-Storey Windows business, demonstrated by record levels of inquiries converting to bookings, should bolster production and revenue in 2026 and beyond, especially given demand in the U.S. and Eastern Canada.

- The investments in Aerospace & Aviation, particularly the medevac contracts in Manitoba and BC, as well as future deployments in Newfoundland and Australia, are set to drive revenue growth. The addition of new King Air aircraft and associated contracts is likely to increase earnings as well.

- The growth in Aircraft Sales & Leasing, spurred by recent investments in the lease portfolio and heightened demand for parts due to supply chain issues, is expected to sustain revenue momentum and improve net margins moving forward.

- The continued expansion in the Environmental Access Solutions business due to strategic acquisitions like Spartan and Duhamel, coupled with product innovations such as the SYSTEM7-XT mat, positions the segment for increased revenue and profitability in Eastern Canada and the U.S. market.

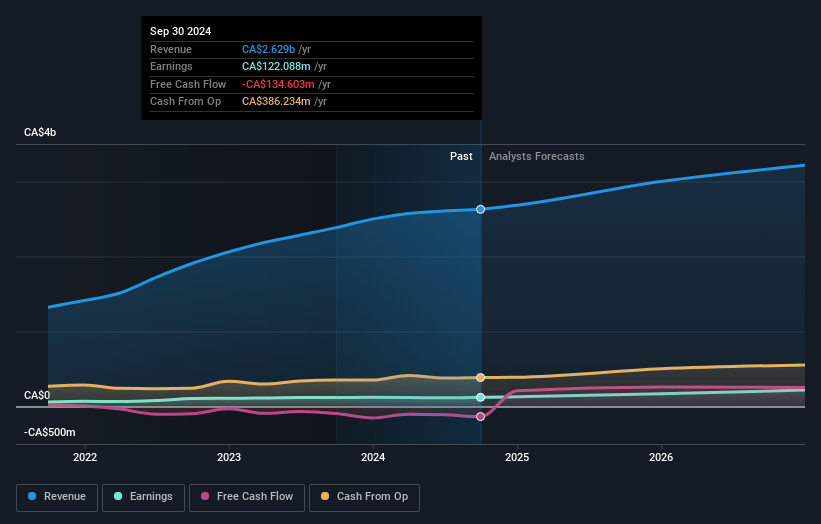

Exchange Income Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Exchange Income's revenue will grow by 6.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.6% today to 8.1% in 3 years time.

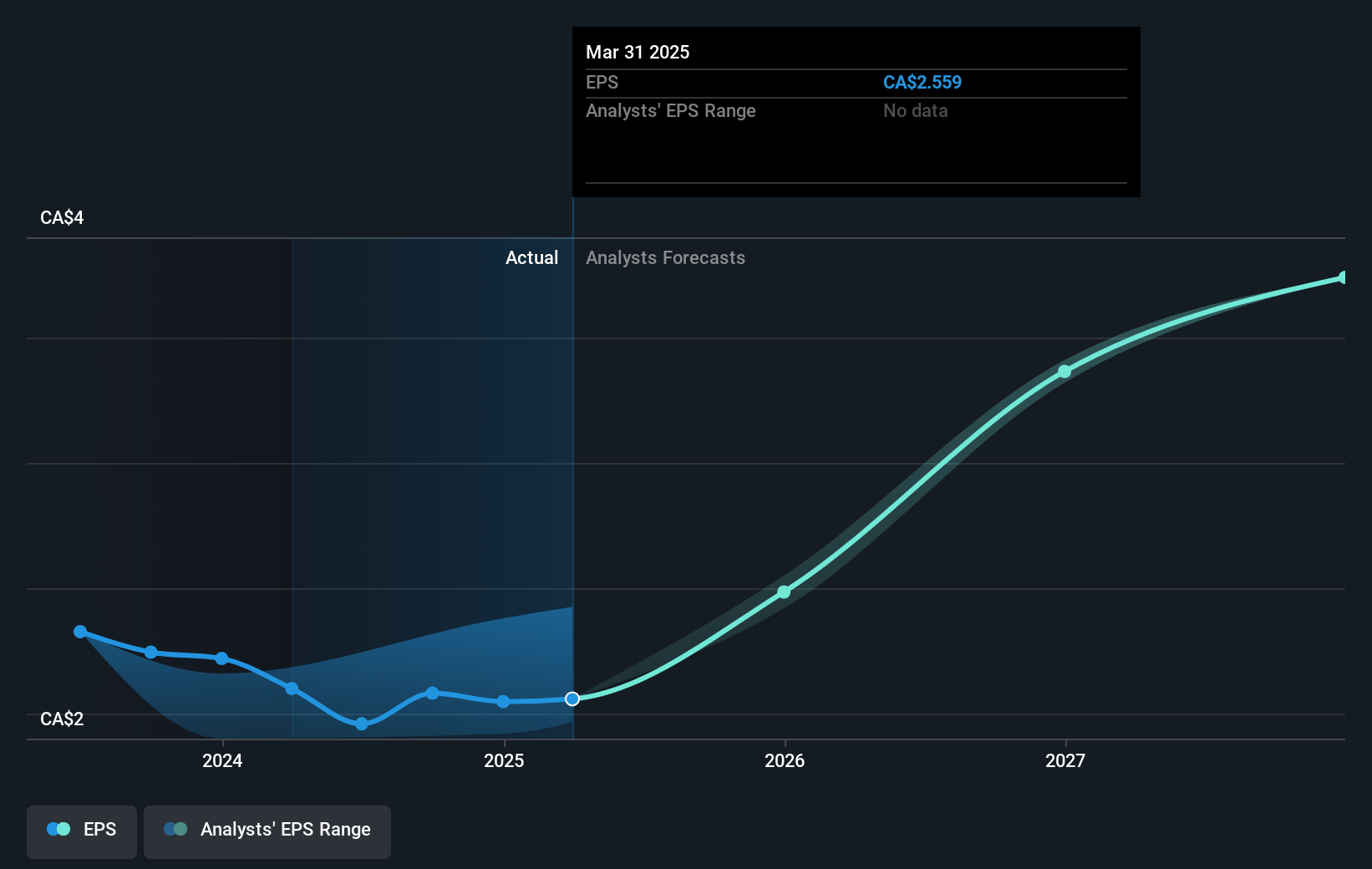

- Analysts expect earnings to reach CA$257.3 million (and earnings per share of CA$5.05) by about April 2028, up from CA$121.2 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 19.7x on those 2028 earnings, down from 20.9x today. This future PE is greater than the current PE for the CA Airlines industry at 11.8x.

- Analysts expect the number of shares outstanding to grow by 4.91% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.49%, as per the Simply Wall St company report.

Exchange Income Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- There is significant uncertainty around the potential trade wars due to tariffs, which could affect business and consumer confidence, impacting future revenues and earnings.

- The Aerospace segment faces challenges with labor shortages and supply chain issues, particularly in aircraft parts, which could negatively affect operational efficiency and net margins.

- Ongoing political uncertainties and the potential impact on tariffs and exchange rates present risks to the company’s financial stability, affecting revenue and profit margins.

- Delayed aircraft deliveries due to manufacturing strikes present risks to fulfilling contracts on time, potentially impacting revenue and overall profitability.

- The transition of certain contracts in the Aerospace segment from performance-based to time-and-materials arrangements introduces revenue and profitability variability, potentially affecting earnings stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of CA$69.273 for Exchange Income based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CA$3.2 billion, earnings will come to CA$257.3 million, and it would be trading on a PE ratio of 19.7x, assuming you use a discount rate of 7.5%.

- Given the current share price of CA$49.37, the analyst price target of CA$69.27 is 28.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.