Key Takeaways

- Expansion into Vietnam and Germany is likely to drive revenue growth through strategic location and innovation in label production.

- Consolidation of ventures and reduced corporate expenses could enhance net earnings and margins, ensuring financial stability and growth.

- Inflationary pressures, significant capital expenditures, and currency volatility present risks to margins and revenue growth, while increased debt may strain future financials.

Catalysts

About CCL Industries- Manufactures and sells labels, consumer printable media products, technology-driven label solutions, polymer banknote substrates, and specialty films.

- The establishment of a new apparel label plant in Vietnam, a key location for apparel sourcing, is expected to start operations in the first quarter of 2025, potentially contributing to increased revenue through expanded market presence in a vital region.

- The full consolidation of the Pac-Man CCL joint venture in 2024, following the acquisition of the remaining 50% interest, could potentially enhance net earnings through integrated operations and synergies from a fully owned subsidiary.

- The company's investment in a significant new site in Germany for low-gauge film label production, expected to start in Q2 2025, may drive future revenue growth through innovations in pressure-sensitive labels and increased production capacity.

- CCL Industries’ continued growth in the RFID business, especially in the apparel and retail segments, indicates potential revenue uplift given the significant expansion in capacity and anticipated market share gains from new and existing clients.

- The reduction in corporate expenses due to decreased long-term variable compensation, alongside a robust balance sheet, may allow for future improvements in net margins and earnings stability moving forward.

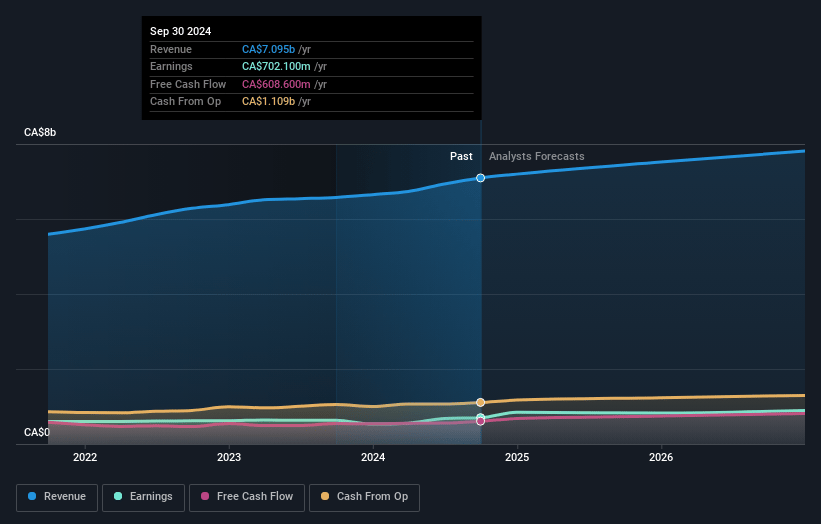

CCL Industries Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming CCL Industries's revenue will grow by 4.0% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 11.6% today to 10.6% in 3 years time.

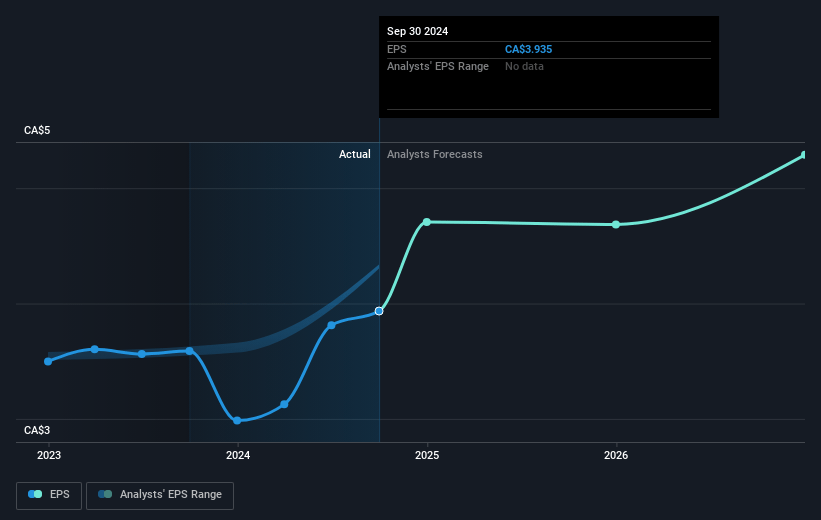

- Analysts expect earnings to reach CA$865.8 million (and earnings per share of CA$5.49) by about April 2028, up from CA$843.1 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 21.0x on those 2028 earnings, up from 14.4x today. This future PE is greater than the current PE for the CA Packaging industry at 9.3x.

- Analysts expect the number of shares outstanding to decline by 1.41% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.88%, as per the Simply Wall St company report.

CCL Industries Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's operating environment could be impacted by potential inflationary or deflationary pressures that are difficult to manage, which may affect margins and revenue stability.

- The start-up costs and significant capital expenditures in places like Vietnam and Germany may impact short-term net earnings if returns on these investments do not materialize as expected.

- The foreign exchange impact, particularly highlighted in Checkpoint's operations in Turkey, could continue to be a risk to profitability if currency volatility persists.

- The challenging RFID market environment and competitive elements, especially with larger competitors scaling back growth outlooks, could present headwinds to revenue growth if similar conditions affect CCL's operations.

- The increased net debt to fund capital expenditures, acquisitions, and share buybacks might pressure financials if interest rates move unfavorably, potentially impacting net margins and future earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of CA$90.8 for CCL Industries based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CA$8.1 billion, earnings will come to CA$865.8 million, and it would be trading on a PE ratio of 21.0x, assuming you use a discount rate of 5.9%.

- Given the current share price of CA$68.87, the analyst price target of CA$90.8 is 24.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.