Last Update 15 Dec 25

Fair value Increased 5.22%PXT: Upcoming Exploration Alliance And Guidance Will Drive Bullish Performance Outlook

Analysts have nudged their average price target for Parex Resources higher, from about C$19.80 to roughly C$20.83, citing a modestly stronger profit margin outlook and slightly lower forward valuation multiples.

Analyst Commentary

Recent research updates reflect a cautiously constructive stance on Parex Resources, with higher price targets signaling improved confidence in the company’s near term earnings power and balance sheet resilience.

Bullish Takeaways

- Bullish analysts highlight that the move in price targets to around C$20 suggests the stock now embeds more realistic assumptions on commodity prices, narrowing the gap between intrinsic value estimates and the current share price.

- Upward revisions are being framed as a response to better than expected margin durability, as cost control and capital discipline support free cash flow generation even under conservative production scenarios.

- Some see room for further upside if management can convert its portfolio opportunities into sustained production growth, which would justify a higher earnings multiple relative to historical averages.

- The reaffirmed neutral style ratings are being interpreted by bullish analysts as signaling limited downside risk at current levels, with a more attractive risk reward skew as execution proves consistent.

Bearish Takeaways

- Bearish analysts caution that, despite higher targets, the retained neutral style recommendations indicate lingering concerns about execution risks in delivering consistent volume and cash flow growth.

- There is a view that valuation has become less compelling after the recent re rating, with the stock trading closer to peers on cash flow and earnings multiples, leaving less margin of safety if commodity prices soften.

- Some remain wary that the company’s growth outlook is still heavily dependent on a narrow geographic and asset base, which could constrain multiple expansion until diversification or scale improves.

- Macro and regulatory uncertainty in the company’s operating regions continue to be cited as overhangs that could cap near term upside, even as fundamentals incrementally improve.

What's in the News

- Parex and Ecopetrol have effectively completed a full strategic alliance across the Llanos Foothills exploration trend, reinforcing their joint position in a basin recognized for world class exploration potential and Colombia's long term energy security (company update).

- Regulators approved the extension of the Piedemonte Convenio into part of the Niscota block, with Parex securing a 50% share of future production in exchange for funding 100% of the Floreña Huron exploration well, which is planned to spud after civil works in the 2026 program (company update).

- The Farallones exploration prospect is advancing, with all regulatory approvals in place and initial works underway as Parex prepares to fund and drill the Farallones exploration well on a 100% capital basis in its 2026 program (company update).

- Parex reported strong recent operating trends, with production averaging 49,300 boe/d in October 2025 and 50,300 boe/d in November 2025, driven by high rate new wells at LLA 32 and LLA 74 that are now stabilizing (company update).

- With year to date 2025 average production of 44,550 boe/d, Parex expects to deliver around the midpoint of its 2025 annual production guidance of 45,000 boe/d within the 43,000 to 47,000 boe/d range, and it plans to release its 2026 guidance after markets close on January 19, 2026 (company update).

Valuation Changes

- Consensus Analyst Price Target has risen modestly from CA$19.80 to approximately CA$20.83, implying a slightly higher assessed fair value for Parex shares.

- Discount Rate is effectively unchanged, edging down only fractionally from 6.12% to 6.12%, indicating a stable perceived risk profile.

- Revenue Growth expectations are essentially flat, with projected growth holding steady at about 1.63% year over year.

- Net Profit Margin has increased meaningfully from roughly 22.1% to about 23.8%, reflecting an improved outlook for underlying profitability.

- Future P/E has edged lower from about 7.34x to 7.29x, indicating a slightly cheaper forward earnings multiple despite the higher price target.

Key Takeaways

- Enhanced efficiency and cost reductions support resilient earnings and margins, strengthening the company's position amid changing oil prices and energy market dynamics.

- Expansion into new reserves, gas monetization, and a focus on low-emission operations drive growth, revenue diversification, and improved investor appeal.

- Heavy reliance on mature Colombian assets exposes Parex to regulatory, operational, and energy transition risks that threaten long-term growth prospects and margin stability.

Catalysts

About Parex Resources- Engages in the exploration, development, production, and marketing of oil and natural gas in Colombia.

- The company is rapidly expanding production capacity through successful development drilling, secondary recovery (EOR), and near-field exploration across its core Colombian assets, positioning it to capitalize on persistent global energy demand growth and potential oil supply tightness-this should drive revenue and free funds flow growth as production volumes rise.

- Meaningful internal cost optimizations, infrastructure upgrades, and lower normalized power costs have structurally reduced operating expenses, enhancing netbacks and driving higher net margins-enabling more resilient earnings even in a lower oil price environment.

- Accelerated near-field and greenfield exploration (e.g., Putumayo, Llanos Foothills, VIM area) are expected to open up new reserves and production streams, leveraging technological advancements and offering visible production and revenue upside in 2026 and beyond.

- The upcoming monetization of significant natural gas volumes (e.g., La Belleza block), supported by new pipeline infrastructure in a Colombian market experiencing gas shortages, represents a forward-looking catalyst for revenue diversification and margin expansion.

- Parex's commitment to low-emission operations and the release of its annual sustainability report reinforce its ability to attract capital and maintain regulatory favor, positioning the company to benefit from the industry's shift toward higher environmental standards and supporting long-term cost of capital and share price potential.

Parex Resources Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Parex Resources's revenue will decrease by 0.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 13.5% today to 25.5% in 3 years time.

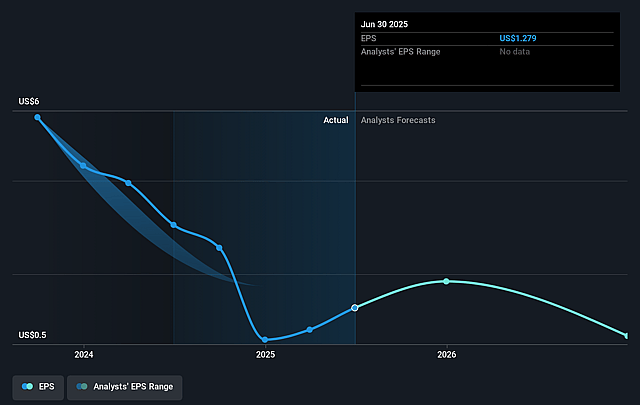

- Analysts expect earnings to reach $243.7 million (and earnings per share of $0.46) by about September 2028, up from $126.5 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 5.5x on those 2028 earnings, down from 9.7x today. This future PE is lower than the current PE for the CA Oil and Gas industry at 12.2x.

- Analysts expect the number of shares outstanding to decline by 2.26% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.97%, as per the Simply Wall St company report.

Parex Resources Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Parex's exclusive focus and asset concentration in Colombia exposes it to significant geographic and political risk, making it vulnerable to changes in local regulatory, tax, and royalty policies, which could directly impact revenue stability and increase the possibility of future asset impairments.

- The company's strategy relies on continued development of existing mature assets, such as Cabrestero and Llanos 34, which are subject to natural production decline rates that may require continually higher capital expenditures to simply maintain output, potentially leading to lower free cash flow and squeezed net margins over the long term.

- Planned production growth and future gas monetization projects depend on successful acquisition and timely renewal of exploration licenses, ongoing community engagement, and complex infrastructure builds, introducing execution and bureaucratic risks that could delay or reduce future earnings.

- Long-term secular trends favoring global decarbonization, accelerating renewable energy adoption, and the increasing electrification of transportation threaten to structurally reduce oil demand and prices, putting sustained pressure on Parex's revenue and profit outlook.

- Heightened investor and regulatory focus on ESG standards could raise capital costs, constrain access to financing, and shrink the potential investor pool for oil producers; coupled with the potential implementation of stricter emissions regulations, this could increase compliance and operating costs and erode long-term net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of CA$17.167 for Parex Resources based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $956.5 million, earnings will come to $243.7 million, and it would be trading on a PE ratio of 5.5x, assuming you use a discount rate of 6.0%.

- Given the current share price of CA$17.51, the analyst price target of CA$17.17 is 2.0% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Parex Resources?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.