Key Takeaways

- Strategic geographic diversification in South America enhances revenue growth and export volume through market penetration and supply-demand mismatches.

- Sustainability initiatives and infrastructure projects aim to boost brand value, exports, and net revenue by appealing to environmentally conscious buyers and favorable demand from major markets.

- Operational and financial challenges linked to new asset integration and geopolitics could affect Minerva's profitability and revenue stability.

Catalysts

About Minerva- Produces and sells fresh beef, livestock, and by-products in South America and internationally.

- Minerva's recent acquisition of new plants in Brazil, Argentina, and Chile, along with planned integration and operational efficiency programs, are expected to unlock synergies and improve operational performance. This will potentially enhance revenue and EBITDA margins in upcoming quarters.

- The company's strategic geographic diversification, particularly in South America, positions Minerva to capitalize on global supply and demand mismatches in the beef market. This is anticipated to drive revenue growth through increased export volume and market penetration.

- The ongoing integration of acquired plants and ramp-up to optimal utilization levels is projected to incrementally enhance EBITDA. Management anticipates these assets will operate at the profitability levels of Minerva’s historical plants within two to three quarters.

- Minerva's focus on sustainability through initiatives like obtaining the ISO 14001 standard, along with successful integration of sustainability programs in Argentina and Uruguay, could enhance its brand value and potentially expand revenue from environmentally conscious buyers.

- The completion of key infrastructure projects, like the Rolim de Moura facility opening for the U.S. market, and favorable global beef demand dynamics, particularly from North America and China, are expected to boost exports and improve net revenue.

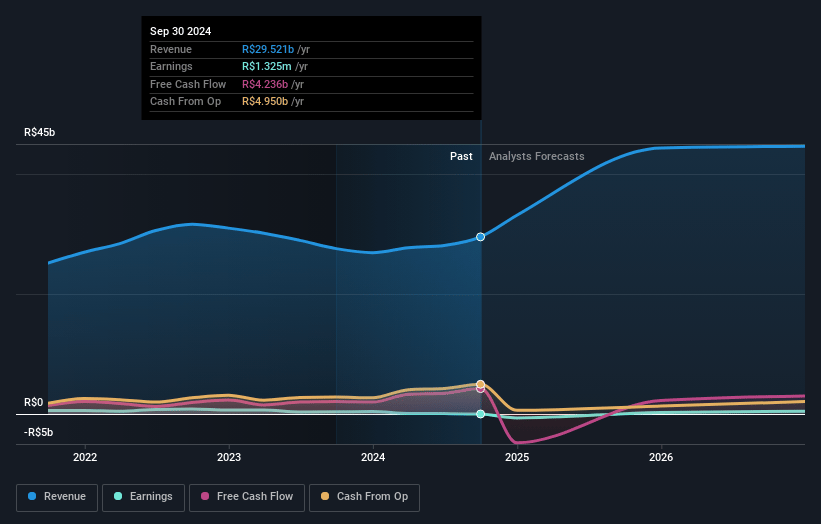

Minerva Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Minerva's revenue will grow by 16.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from -4.6% today to 1.8% in 3 years time.

- Analysts expect earnings to reach R$979.0 million (and earnings per share of R$0.84) by about May 2028, up from R$-1.6 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 9.3x on those 2028 earnings, up from -2.7x today. This future PE is lower than the current PE for the BR Food industry at 10.9x.

- Analysts expect the number of shares outstanding to grow by 0.26% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 25.29%, as per the Simply Wall St company report.

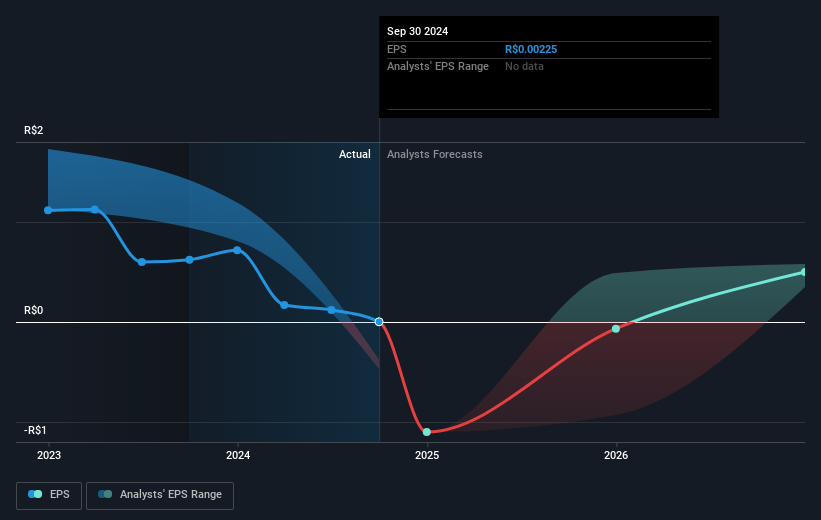

Minerva Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The integration of new plants in Brazil, Argentina, and Chile could face challenges, as evidenced by some facilities needing operational upgrades and delays, which may impact expected synergies and thus influence EBITDA margins and net earnings.

- Minerva's reliance on geopolitical dynamics, like trade expectations with the U.S. and China, introduces uncertainties in its revenue projections, given potential shifts in tariffs and market access.

- High concentration of exports (over 60% of revenue), particularly towards volatile markets such as China, makes the company susceptible to external disruptions which could result in inconsistent revenue streams.

- The integration of new assets has increased Minerva’s leverage to 3.7x net debt over adjusted EBITDA, raising financial risk and the need for effective debt management to maintain net margins and profitability.

- Operational ramp-up challenges and underutilization of new facilities, with capacity currently at 45-50% and potential delay in realizing full synergies, could pressure profitability and delay anticipated earnings enhancements.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of R$7.823 for Minerva based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of R$11.0, and the most bearish reporting a price target of just R$5.5.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be R$53.6 billion, earnings will come to R$979.0 million, and it would be trading on a PE ratio of 9.3x, assuming you use a discount rate of 25.3%.

- Given the current share price of R$7.27, the analyst price target of R$7.82 is 7.1% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.