Key Takeaways

- Strategic investments in deepwater fields and productive assets aim to improve margins and reduce operational costs.

- Restructuring and low debt maintenance bolster financial stability, supporting growth opportunities and potential future EPS increases.

- Lower Brent crude and diesel prices, coupled with operational and regulatory challenges, threaten Petrobras' profitability and future earnings potential amidst economic uncertainties and increased costs.

Catalysts

About Petróleo Brasileiro - Petrobras- Explores, produces, and sells oil and gas in Brazil and internationally.

- The advancement of major production projects such as FPSO Almirante Tamandare and Maria Quiteria in the Buzios field suggests that Petrobras is anticipating significant increases in oil production capacity, which could lead to higher future revenues.

- The company's strategic decision to accelerate investments in high-return deepwater oil fields and the expansion of its most productive assets could improve net margins by optimizing production efficiency and reducing future operational costs.

- Efforts to mitigate financial risks by restructuring investments and maintaining a strategic approach to CapEx allocation might enhance earnings stability and predictability in future periods.

- Petrobras is potentially restrengthening its liquidity by maintaining low financial debt levels, which helps the company preserve capital for profitable growth opportunities, potentially boosting future earnings per share (EPS).

- The commitment to continued production growth and exploration in high-potential areas like the Equatorial Margin indicates a focus on enhancing long-term reserves, supporting sustained revenue growth and stabilized earnings.

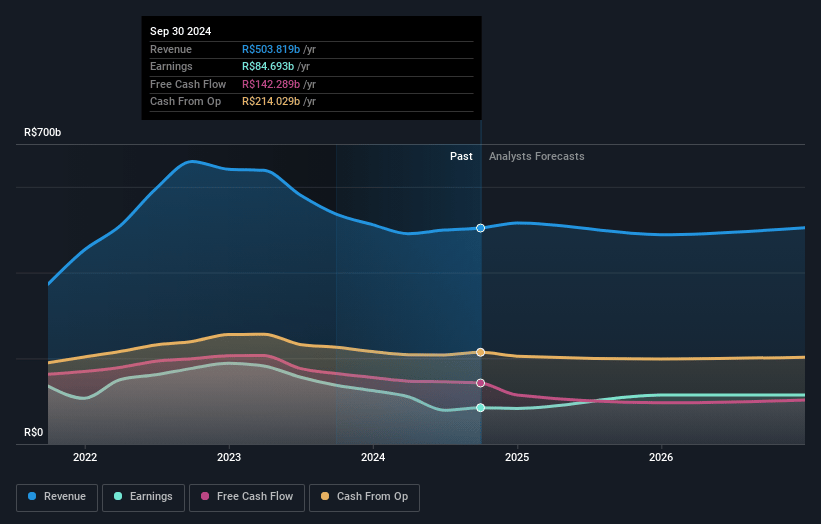

Petróleo Brasileiro - Petrobras Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Petróleo Brasileiro - Petrobras's revenue will grow by 1.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.5% today to 19.6% in 3 years time.

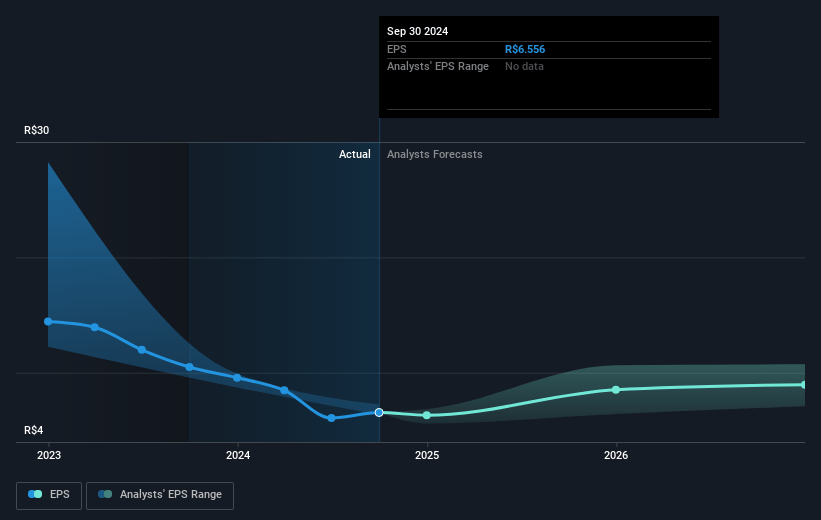

- Analysts expect earnings to reach R$100.2 billion (and earnings per share of R$7.41) by about May 2028, up from R$36.6 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting R$118.8 billion in earnings, and the most bearish expecting R$80.5 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 9.6x on those 2028 earnings, down from 10.8x today. This future PE is greater than the current PE for the US Oil and Gas industry at 8.5x.

- Analysts expect the number of shares outstanding to decline by 0.16% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 19.92%, as per the Simply Wall St company report.

Petróleo Brasileiro - Petrobras Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The lower Brent crude and diesel crack spread prices, key revenue drivers for Petrobras, have negatively impacted the company due to global economic uncertainties and lower demand, affecting overall industry profitability.

- The company experienced a R$17 billion loss in Q4 due to foreign exchange rate variations impacting debt, indirectly affecting Petrobras' earnings despite not involving cash outflow.

- Scheduled maintenance shutdowns, including effects from industry agency strikes, led to decreased production which could impact revenues and lead to unpredictable production schedules.

- Increased costs of new projects and operational rigs, possibly due to industry-wide inflation and design complexities, may lead to higher future CapEx impacting Petrobras' financial flexibility.

- Environmental licensing delays and stringent requirements in the Equatorial Margin and other basins could slow down future exploration and production, possibly risking future earnings potential.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of R$43.509 for Petróleo Brasileiro - Petrobras based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of R$48.5, and the most bearish reporting a price target of just R$35.6.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be R$511.4 billion, earnings will come to R$100.2 billion, and it would be trading on a PE ratio of 9.6x, assuming you use a discount rate of 19.9%.

- Given the current share price of R$30.56, the analyst price target of R$43.51 is 29.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.