Stock Analysis

- United States

- /

- Pharma

- /

- NasdaqGM:RETA

Here's Why We're Not At All Concerned With Reata Pharmaceuticals' (NASDAQ:RETA) Cash Burn Situation

There's no doubt that money can be made by owning shares of unprofitable businesses. By way of example, Reata Pharmaceuticals (NASDAQ:RETA) has seen its share price rise 331% over the last year, delighting many shareholders. But the harsh reality is that very many loss making companies burn through all their cash and go bankrupt.

In light of its strong share price run, we think now is a good time to investigate how risky Reata Pharmaceuticals' cash burn is. For the purpose of this article, we'll define cash burn as the amount of cash the company is spending each year to fund its growth (also called its negative free cash flow). First, we'll determine its cash runway by comparing its cash burn with its cash reserves.

Check out our latest analysis for Reata Pharmaceuticals

SWOT Analysis for Reata Pharmaceuticals

- Currently debt free.

- Shareholders have been diluted in the past year.

- Trading below our estimate of fair value by more than 20%.

- Has less than 3 years of cash runway based on current free cash flow.

- Total liabilities exceed total assets, which raises the risk of financial distress.

- Not expected to become profitable over the next 3 years.

How Long Is Reata Pharmaceuticals' Cash Runway?

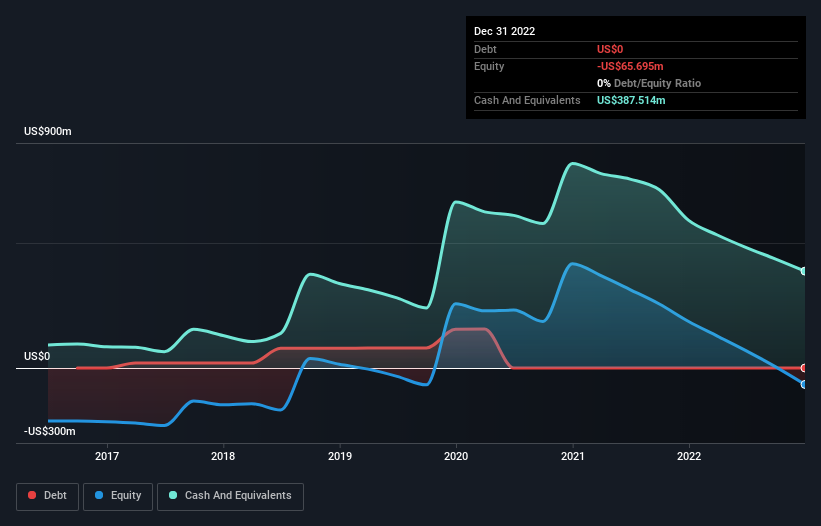

A company's cash runway is calculated by dividing its cash hoard by its cash burn. In December 2022, Reata Pharmaceuticals had US$388m in cash, and was debt-free. Looking at the last year, the company burnt through US$208m. Therefore, from December 2022 it had roughly 22 months of cash runway. Notably, however, analysts think that Reata Pharmaceuticals will break even (at a free cash flow level) before then. In that case, it may never reach the end of its cash runway. Depicted below, you can see how its cash holdings have changed over time.

How Well Is Reata Pharmaceuticals Growing?

Reata Pharmaceuticals reduced its cash burn by 12% during the last year, which points to some degree of discipline. But it makes us pessimistic to see that operating revenue slid 80% in that time. Considering both these metrics, we're a little concerned about how the company is developing. While the past is always worth studying, it is the future that matters most of all. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

Can Reata Pharmaceuticals Raise More Cash Easily?

While Reata Pharmaceuticals seems to be in a fairly good position, it's still worth considering how easily it could raise more cash, even just to fuel faster growth. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. Commonly, a business will sell new shares in itself to raise cash and drive growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Since it has a market capitalisation of US$4.0b, Reata Pharmaceuticals' US$208m in cash burn equates to about 5.2% of its market value. Given that is a rather small percentage, it would probably be really easy for the company to fund another year's growth by issuing some new shares to investors, or even by taking out a loan.

Is Reata Pharmaceuticals' Cash Burn A Worry?

As you can probably tell by now, we're not too worried about Reata Pharmaceuticals' cash burn. In particular, we think its cash burn relative to its market cap stands out as evidence that the company is well on top of its spending. While we must concede that its falling revenue is a bit worrying, the other factors mentioned in this article provide great comfort when it comes to the cash burn. It's clearly very positive to see that analysts are forecasting the company will break even fairly soon. Taking all the factors in this report into account, we're not at all worried about its cash burn, as the business appears well capitalized to spend as needs be. On another note, we conducted an in-depth investigation of the company, and identified 6 warning signs for Reata Pharmaceuticals (2 can't be ignored!) that you should be aware of before investing here.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies insiders are buying, and this list of stocks growth stocks (according to analyst forecasts)

Valuation is complex, but we're helping make it simple.

Find out whether Reata Pharmaceuticals is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:RETA

Reata Pharmaceuticals

Reata Pharmaceuticals, Inc., a clinical-stage biopharmaceutical company, identifies, develops, and commercializes novel therapeutics for patients with serious or life-threatening diseases.

High growth potential with excellent balance sheet.