Stock Analysis

- Taiwan

- /

- Renewable Energy

- /

- TWSE:8926

Taiwan Cogeneration Corporation's (TWSE:8926) Stock Going Strong But Fundamentals Look Weak: What Implications Could This Have On The Stock?

Taiwan Cogeneration's (TWSE:8926) stock is up by a considerable 22% over the past three months. However, we decided to pay close attention to its weak financials as we are doubtful that the current momentum will keep up, given the scenario. In this article, we decided to focus on Taiwan Cogeneration's ROE.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

View our latest analysis for Taiwan Cogeneration

How Do You Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Taiwan Cogeneration is:

8.0% = NT$1.2b ÷ NT$16b (Based on the trailing twelve months to December 2023).

The 'return' is the profit over the last twelve months. One way to conceptualize this is that for each NT$1 of shareholders' capital it has, the company made NT$0.08 in profit.

Why Is ROE Important For Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Taiwan Cogeneration's Earnings Growth And 8.0% ROE

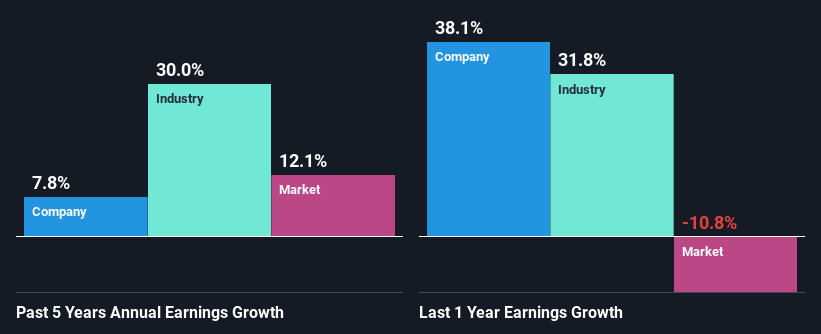

When you first look at it, Taiwan Cogeneration's ROE doesn't look that attractive. Next, when compared to the average industry ROE of 11%, the company's ROE leaves us feeling even less enthusiastic. However, the moderate 7.8% net income growth seen by Taiwan Cogeneration over the past five years is definitely a positive. We reckon that there could be other factors at play here. Such as - high earnings retention or an efficient management in place.

Next, on comparing with the industry net income growth, we found that Taiwan Cogeneration's reported growth was lower than the industry growth of 30% over the last few years, which is not something we like to see.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. Is Taiwan Cogeneration fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Taiwan Cogeneration Efficiently Re-investing Its Profits?

Taiwan Cogeneration's high three-year median payout ratio of 115% suggests that the company is paying out more to its shareholders than what it is making. In spite of this, the company was able to grow its earnings respectably, as we saw above. Although, the high payout ratio is certainly something we would keep an eye on if the company is not able to keep up its growth, or if business deteriorates. To know the 2 risks we have identified for Taiwan Cogeneration visit our risks dashboard for free.

Moreover, Taiwan Cogeneration is determined to keep sharing its profits with shareholders which we infer from its long history of paying a dividend for at least ten years.

Conclusion

On the whole, Taiwan Cogeneration's performance is quite a big let-down. Although the company has shown a fair bit of growth in earnings, yet the low ROE and the low rate of reinvestment makes us skeptical about the continuity of that growth, especially when or if the business comes to face any threats. Until now, we have only just grazed the surface of the company's past performance by looking at the company's fundamentals. To gain further insights into Taiwan Cogeneration's past profit growth, check out this visualization of past earnings, revenue and cash flows.

Valuation is complex, but we're helping make it simple.

Find out whether Taiwan Cogeneration is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:8926

Taiwan Cogeneration

Taiwan Cogeneration Corporation, together with its subsidiaries, operates and manages cogeneration plants in Taiwan.

Solid track record with mediocre balance sheet.