Stock Analysis

Just Four Days Till Opter AB (publ) (STO:OPTER) Will Be Trading Ex-Dividend

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Opter AB (publ) (STO:OPTER) is about to go ex-dividend in just four days. The ex-dividend date occurs one day before the record date which is the day on which shareholders need to be on the company's books in order to receive a dividend. The ex-dividend date is an important date to be aware of as any purchase of the stock made on or after this date might mean a late settlement that doesn't show on the record date. This means that investors who purchase Opter's shares on or after the 26th of April will not receive the dividend, which will be paid on the 3rd of May.

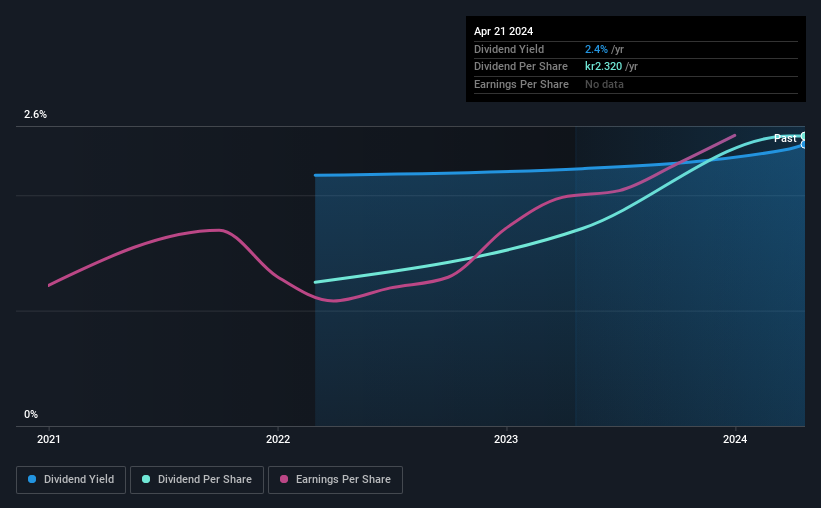

The company's upcoming dividend is kr02.32 a share, following on from the last 12 months, when the company distributed a total of kr2.32 per share to shareholders. Calculating the last year's worth of payments shows that Opter has a trailing yield of 2.4% on the current share price of kr095.00. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. That's why we should always check whether the dividend payments appear sustainable, and if the company is growing.

View our latest analysis for Opter

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Last year Opter paid out 100% of its profits as dividends to shareholders, suggesting the dividend is not well covered by earnings. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. Dividends consumed 69% of the company's free cash flow last year, which is within a normal range for most dividend-paying organisations.

It's good to see that while Opter's dividends were not well covered by profits, at least they are affordable from a cash perspective. Still, if this were to happen repeatedly, we'd be concerned about whether the dividend is sustainable in a downturn.

Click here to see how much of its profit Opter paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. It's encouraging to see Opter has grown its earnings rapidly, up 27% a year for the past three years.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Opter has delivered 42% dividend growth per year on average over the past two years. Both per-share earnings and dividends have both been growing rapidly in recent times, which is great to see.

Final Takeaway

Is Opter worth buying for its dividend? Growing earnings per share and a normal cashflow payout ratio is an ok combination, but we're concerned that the company is paying out such a high percentage of its income as dividends. It might be worth researching if the company is reinvesting in growth projects that could grow earnings and dividends in the future, but for now we're not all that optimistic on its dividend prospects.

If you're not too concerned about Opter's ability to pay dividends, you should still be mindful of some of the other risks that this business faces. To help with this, we've discovered 3 warning signs for Opter (2 make us uncomfortable!) that you ought to be aware of before buying the shares.

If you're in the market for strong dividend payers, we recommend checking our selection of top dividend stocks.

Valuation is complex, but we're helping make it simple.

Find out whether Opter is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:OPTER

Opter

Opter AB (publ), a SaaS company, provides transport planning solutions primarily in Sweden, Norway, Finland, Denmark, and other Nordic countries.

Outstanding track record with flawless balance sheet.