Stock Analysis

- Qatar

- /

- Energy Services

- /

- DSM:GISS

Recent 3.9% pullback isn't enough to hurt long-term Gulf International Services Q.P.S.C (DSM:GISS) shareholders, they're still up 96% over 5 years

Stock pickers are generally looking for stocks that will outperform the broader market. Buying under-rated businesses is one path to excess returns. For example, long term Gulf International Services Q.P.S.C. (DSM:GISS) shareholders have enjoyed a 75% share price rise over the last half decade, well in excess of the market decline of around 9.1% (not including dividends). On the other hand, the more recent gains haven't been so impressive, with shareholders gaining just 43% , including dividends .

In light of the stock dropping 3.9% in the past week, we want to investigate the longer term story, and see if fundamentals have been the driver of the company's positive five-year return.

Check out our latest analysis for Gulf International Services Q.P.S.C

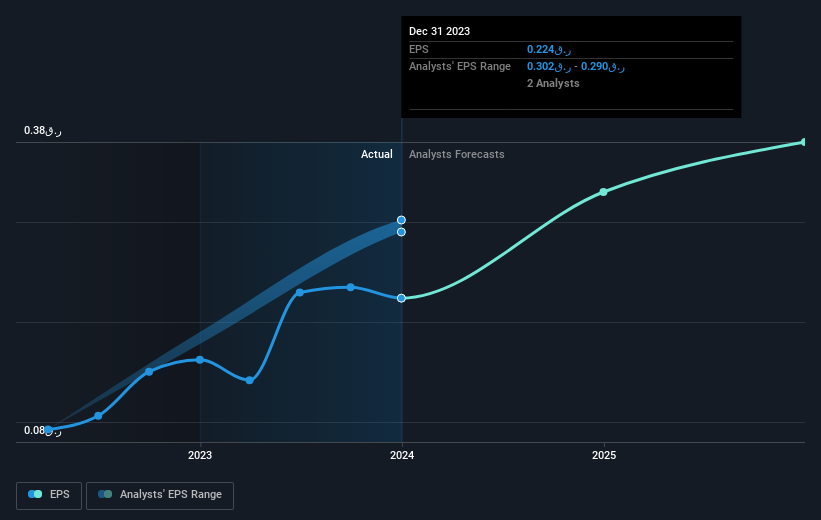

There is no denying that markets are sometimes efficient, but prices do not always reflect underlying business performance. One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

During the last half decade, Gulf International Services Q.P.S.C became profitable. That's generally thought to be a genuine positive, so investors may expect to see an increasing share price.

You can see below how EPS has changed over time (discover the exact values by clicking on the image).

It is of course excellent to see how Gulf International Services Q.P.S.C has grown profits over the years, but the future is more important for shareholders. If you are thinking of buying or selling Gulf International Services Q.P.S.C stock, you should check out this FREE detailed report on its balance sheet.

What About Dividends?

It is important to consider the total shareholder return, as well as the share price return, for any given stock. The TSR incorporates the value of any spin-offs or discounted capital raisings, along with any dividends, based on the assumption that the dividends are reinvested. Arguably, the TSR gives a more comprehensive picture of the return generated by a stock. We note that for Gulf International Services Q.P.S.C the TSR over the last 5 years was 96%, which is better than the share price return mentioned above. And there's no prize for guessing that the dividend payments largely explain the divergence!

A Different Perspective

It's nice to see that Gulf International Services Q.P.S.C shareholders have received a total shareholder return of 43% over the last year. That's including the dividend. Since the one-year TSR is better than the five-year TSR (the latter coming in at 14% per year), it would seem that the stock's performance has improved in recent times. Given the share price momentum remains strong, it might be worth taking a closer look at the stock, lest you miss an opportunity. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Consider risks, for instance. Every company has them, and we've spotted 2 warning signs for Gulf International Services Q.P.S.C you should know about.

If you are like me, then you will not want to miss this free list of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Qatari exchanges.

Valuation is complex, but we're helping make it simple.

Find out whether Gulf International Services Q.P.S.C is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About DSM:GISS

Gulf International Services Q.P.S.C

Gulf International Services Q.P.S.C., through its subsidiaries, engages in the provision of insurance and reinsurance, helicopter transportation, and drilling and related services in Qatar, Turkiye, and internationally.

Solid track record with mediocre balance sheet.