Stock Analysis

- South Korea

- /

- Chemicals

- /

- KOSDAQ:A187420

GenoFocus (KOSDAQ:187420) adds ₩9.4b to market cap in the past 7 days, though investors from three years ago are still down 59%

This week we saw the GenoFocus, Inc. (KOSDAQ:187420) share price climb by 11%. But that doesn't change the fact that the returns over the last three years have been disappointing. Tragically, the share price declined 59% in that time. So the improvement may be a real relief to some. The rise has some hopeful, but turnarounds are often precarious.

The recent uptick of 11% could be a positive sign of things to come, so let's take a look at historical fundamentals.

Check out our latest analysis for GenoFocus

Because GenoFocus made a loss in the last twelve months, we think the market is probably more focussed on revenue and revenue growth, at least for now. When a company doesn't make profits, we'd generally hope to see good revenue growth. That's because fast revenue growth can be easily extrapolated to forecast profits, often of considerable size.

In the last three years, GenoFocus saw its revenue grow by 11% per year, compound. That's a pretty good rate of top-line growth. So some shareholders would be frustrated with the compound loss of 17% per year. The market must have had really high expectations to be disappointed with this progress. So this is one stock that might be worth investigating further, or even adding to your watchlist.

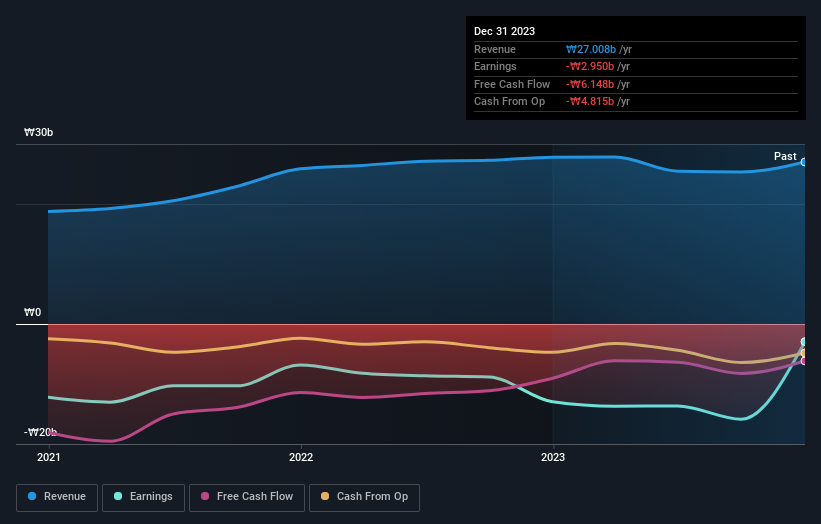

The graphic below depicts how earnings and revenue have changed over time (unveil the exact values by clicking on the image).

Take a more thorough look at GenoFocus' financial health with this free report on its balance sheet.

A Different Perspective

GenoFocus shareholders are down 6.3% for the year, but the market itself is up 6.9%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Unfortunately, longer term shareholders are suffering worse, given the loss of 7% doled out over the last five years. We'd need to see some sustained improvements in the key metrics before we could muster much enthusiasm. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Consider for instance, the ever-present spectre of investment risk. We've identified 2 warning signs with GenoFocus (at least 1 which makes us a bit uncomfortable) , and understanding them should be part of your investment process.

If you would prefer to check out another company -- one with potentially superior financials -- then do not miss this free list of companies that have proven they can grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on South Korean exchanges.

Valuation is complex, but we're helping make it simple.

Find out whether GenoFocus is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KOSDAQ:A187420

GenoFocus

GenoFocus, Inc. engages in the research and development, production, sales, and import/export of enzymes and fermentation products in South Korea and internationally.

Mediocre balance sheet with weak fundamentals.