- South Korea

- /

- Packaging

- /

- KOSE:A014820

Undiscovered Gems in South Korea to Watch This September 2024

Reviewed by Simply Wall St

Over the last 7 days, the South Korean market has remained flat with a notable 3.1% decline in the Financials sector, and it has shown no significant change over the past 12 months. Despite this stagnation, earnings are forecast to grow by an impressive 29% annually, making it an opportune time to identify stocks with strong growth potential that may be flying under the radar.

Top 10 Undiscovered Gems With Strong Fundamentals In South Korea

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Korea Airport ServiceLtd | NA | 3.97% | 42.22% | ★★★★★★ |

| Miwon Chemicals | 0.08% | 11.70% | 14.38% | ★★★★★★ |

| NOROO PAINT & COATINGS | 13.99% | 5.04% | 7.98% | ★★★★★★ |

| Korea Ratings | NA | 1.13% | 0.54% | ★★★★★★ |

| Samyang | 49.49% | 6.68% | 23.96% | ★★★★★★ |

| Kyung Dong Navien | 22.40% | 11.19% | 18.84% | ★★★★★★ |

| Namuga | 14.47% | 0.88% | 38.25% | ★★★★★★ |

| BIO-FD&CLtd | 1.99% | 10.59% | 21.51% | ★★★★★★ |

| ONEJOON | 10.13% | 35.30% | -5.78% | ★★★★★☆ |

| Daewon Cable | 30.50% | 8.72% | 60.38% | ★★★★★☆ |

Here we highlight a subset of our preferred stocks from the screener.

Soulbrain Holdings (KOSDAQ:A036830)

Simply Wall St Value Rating: ★★★★★☆

Overview: Soulbrain Holdings Co., Ltd. develops, manufactures, and supplies core materials for the semiconductor, display, and secondary battery cell industries in South Korea and internationally, with a market cap of ₩1.12 trillion.

Operations: Soulbrain Holdings generates revenue primarily from the semiconductor, display, and secondary battery cell industries. The company has a market cap of ₩1.12 trillion.

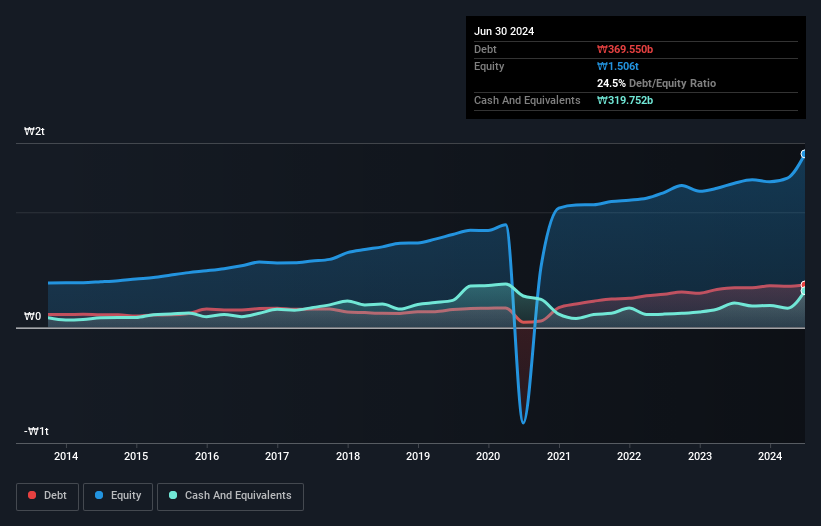

Soulbrain Holdings, a notable player in South Korea's chemicals sector, has seen its earnings grow by 2.4% over the past year, outpacing the industry average of -5.6%. The company's debt to equity ratio increased from 19.4% to 24.5% over five years, yet its net debt to equity ratio remains satisfactory at 3.3%. With EBIT covering interest payments 7.6 times over and trading at a significant discount of 70.7% below estimated fair value, Soulbrain presents an intriguing investment opportunity despite recent share price volatility.

- Navigate through the intricacies of Soulbrain Holdings with our comprehensive health report here.

Examine Soulbrain Holdings' past performance report to understand how it has performed in the past.

Dongwon Systems (KOSE:A014820)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Dongwon Systems Corporation, a packaging company, manufactures and markets packaging materials in South Korea with a market cap of ₩1.27 billion.

Operations: Dongwon Systems generates revenue primarily from its packaging business, amounting to ₩1.27 billion.

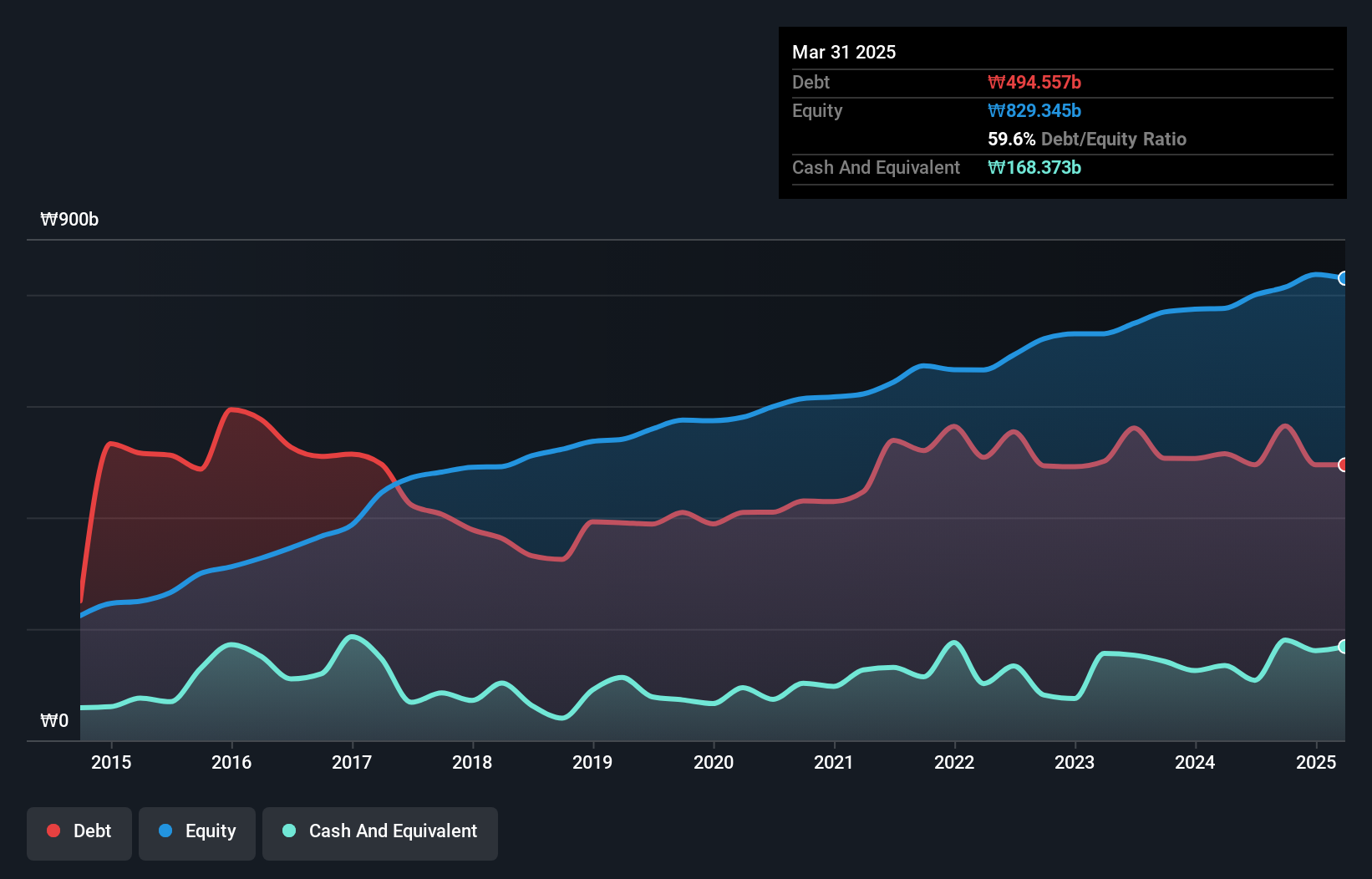

Dongwon Systems reported second-quarter sales of ₩8.50 billion, slightly up from ₩8.47 billion last year, with net income rising to ₩22.26 billion from ₩17.90 billion a year ago. Basic earnings per share increased to ₩761 compared to ₩612 previously, reflecting solid profitability despite high debt levels (net debt to equity ratio at 48%). Over the past five years, the company's debt-to-equity ratio has improved from 69% to 62%, and its EBIT covers interest payments 5.2 times over, indicating robust financial health.

- Get an in-depth perspective on Dongwon Systems' performance by reading our health report here.

Explore historical data to track Dongwon Systems' performance over time in our Past section.

Cuckoo Holdings (KOSE:A192400)

Simply Wall St Value Rating: ★★★★★☆

Overview: Cuckoo Holdings Co., Ltd., with a market cap of ₩767.64 billion, manufactures and sells electric heaters and daily necessities in South Korea and internationally through its subsidiaries.

Operations: Cuckoo Holdings generates revenue primarily from the sale of electric heaters and daily necessities. The company operates in South Korea and internationally through its subsidiaries, with a market cap of ₩767.64 billion.

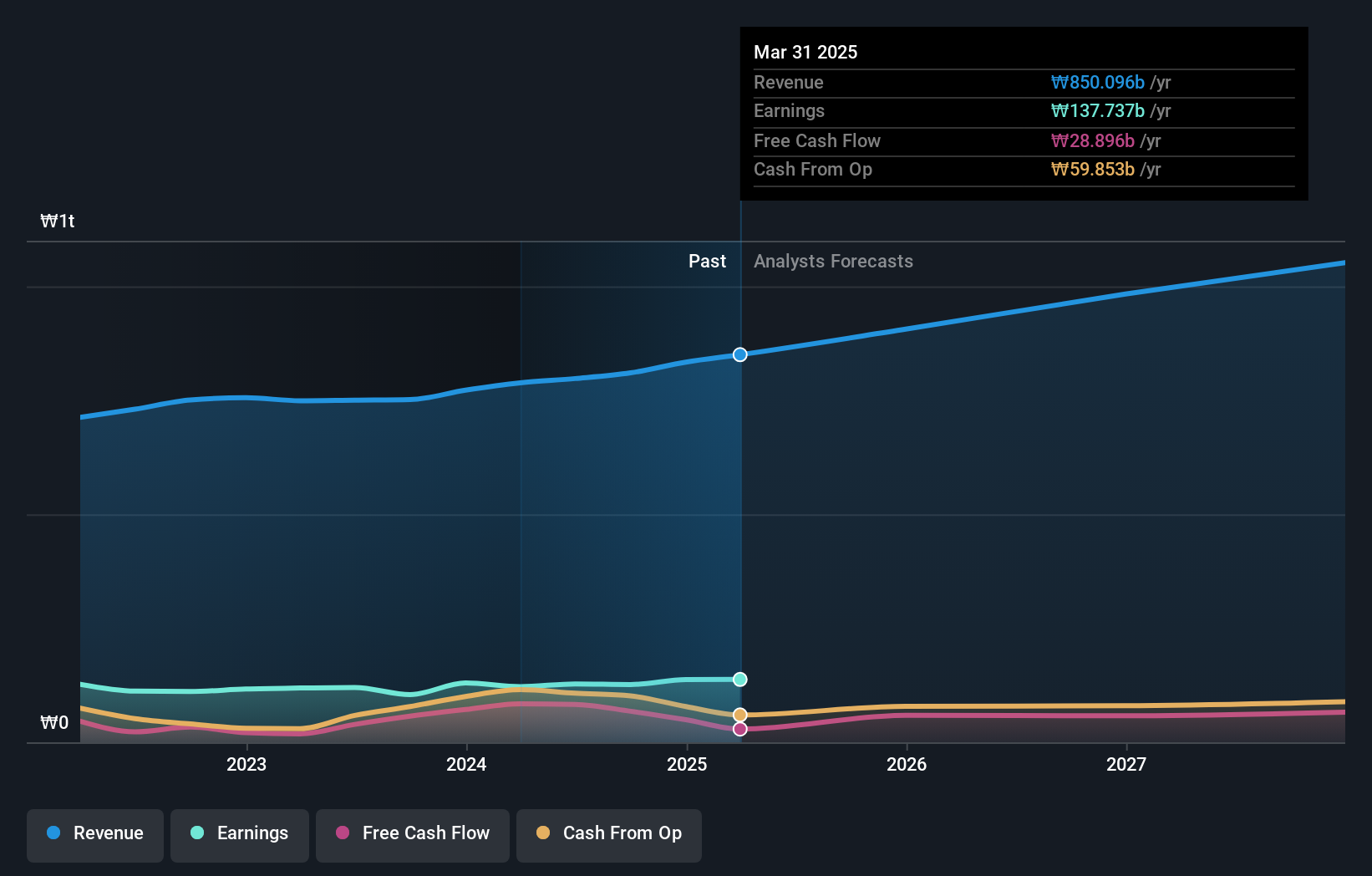

Cuckoo Holdings, a notable player in South Korea's consumer durables sector, has seen its earnings grow at 8.8% annually over the past five years. Recently trading at 79.1% below its estimated fair value, it offers an intriguing valuation proposition. Despite a modest debt-to-equity ratio increase from 0% to 0.04%, the company remains financially sound with more cash than total debt and generates positive free cash flow consistently ($83M as of June 2024).

- Delve into the full analysis health report here for a deeper understanding of Cuckoo Holdings.

Evaluate Cuckoo Holdings' historical performance by accessing our past performance report.

Taking Advantage

- Click through to start exploring the rest of the 189 KRX Undiscovered Gems With Strong Fundamentals now.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSE:A014820

Dongwon Systems

A packaging company, manufactures and markets packaging materials in South Korea.

Proven track record with adequate balance sheet.