Stock Analysis

There's Been No Shortage Of Growth Recently For Yamato Industry's (TSE:7886) Returns On Capital

Finding a business that has the potential to grow substantially is not easy, but it is possible if we look at a few key financial metrics. One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. So on that note, Yamato Industry (TSE:7886) looks quite promising in regards to its trends of return on capital.

Understanding Return On Capital Employed (ROCE)

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on Yamato Industry is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.0018 = JP¥7.0m ÷ (JP¥8.2b - JP¥4.3b) (Based on the trailing twelve months to December 2023).

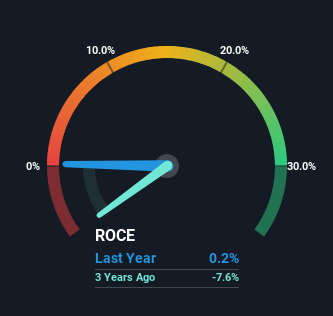

Therefore, Yamato Industry has an ROCE of 0.2%. Ultimately, that's a low return and it under-performs the Chemicals industry average of 6.8%.

Check out our latest analysis for Yamato Industry

Historical performance is a great place to start when researching a stock so above you can see the gauge for Yamato Industry's ROCE against it's prior returns. If you want to delve into the historical earnings , check out these free graphs detailing revenue and cash flow performance of Yamato Industry.

What The Trend Of ROCE Can Tell Us

Shareholders will be relieved that Yamato Industry has broken into profitability. While the business was unprofitable in the past, it's now turned things around and is earning 0.2% on its capital. On top of that, what's interesting is that the amount of capital being employed has remained steady, so the business hasn't needed to put any additional money to work to generate these higher returns. So while we're happy that the business is more efficient, just keep in mind that could mean that going forward the business is lacking areas to invest internally for growth. After all, a company can only become a long term multi-bagger if it continually reinvests in itself at high rates of return.

On a side note, Yamato Industry's current liabilities are still rather high at 52% of total assets. This effectively means that suppliers (or short-term creditors) are funding a large portion of the business, so just be aware that this can introduce some elements of risk. While it's not necessarily a bad thing, it can be beneficial if this ratio is lower.

In Conclusion...

In summary, we're delighted to see that Yamato Industry has been able to increase efficiencies and earn higher rates of return on the same amount of capital. Since the stock has returned a solid 52% to shareholders over the last five years, it's fair to say investors are beginning to recognize these changes. Therefore, we think it would be worth your time to check if these trends are going to continue.

If you want to continue researching Yamato Industry, you might be interested to know about the 1 warning sign that our analysis has discovered.

While Yamato Industry may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

Valuation is complex, but we're helping make it simple.

Find out whether Yamato Industry is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:7886

Yamato Industry

Yamato Industry Co., Ltd. manufactures, processes, and sells OA equipment parts, SP products, distribution equipment, housing and automotive equipment, household goods, information communication goods, and home appliance parts in Japan and internationally.

Adequate balance sheet and slightly overvalued.