Stock Analysis

- India

- /

- Infrastructure

- /

- NSEI:DREDGECORP

Returns On Capital Are Showing Encouraging Signs At Dredging Corporation of India (NSE:DREDGECORP)

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. With that in mind, we've noticed some promising trends at Dredging Corporation of India (NSE:DREDGECORP) so let's look a bit deeper.

Return On Capital Employed (ROCE): What Is It?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on Dredging Corporation of India is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.037 = ₹634m ÷ (₹24b - ₹6.7b) (Based on the trailing twelve months to September 2023).

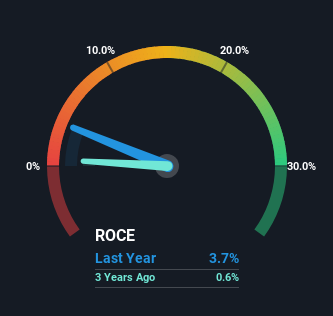

Thus, Dredging Corporation of India has an ROCE of 3.7%. Ultimately, that's a low return and it under-performs the Infrastructure industry average of 8.2%.

Check out our latest analysis for Dredging Corporation of India

Historical performance is a great place to start when researching a stock so above you can see the gauge for Dredging Corporation of India's ROCE against it's prior returns. If you're interested in investigating Dredging Corporation of India's past further, check out this free graph of past earnings, revenue and cash flow.

So How Is Dredging Corporation of India's ROCE Trending?

Shareholders will be relieved that Dredging Corporation of India has broken into profitability. The company now earns 3.7% on its capital, because five years ago it was incurring losses. While returns have increased, the amount of capital employed by Dredging Corporation of India has remained flat over the period. So while we're happy that the business is more efficient, just keep in mind that could mean that going forward the business is lacking areas to invest internally for growth. So if you're looking for high growth, you'll want to see a business's capital employed also increasing.

On a side note, we noticed that the improvement in ROCE appears to be partly fueled by an increase in current liabilities. Effectively this means that suppliers or short-term creditors are now funding 28% of the business, which is more than it was five years ago. Keep an eye out for future increases because when the ratio of current liabilities to total assets gets particularly high, this can introduce some new risks for the business.

In Conclusion...

To sum it up, Dredging Corporation of India is collecting higher returns from the same amount of capital, and that's impressive. And with a respectable 62% awarded to those who held the stock over the last five years, you could argue that these developments are starting to get the attention they deserve. Therefore, we think it would be worth your time to check if these trends are going to continue.

On a final note, we've found 1 warning sign for Dredging Corporation of India that we think you should be aware of.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

Valuation is complex, but we're helping make it simple.

Find out whether Dredging Corporation of India is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:DREDGECORP

Dredging Corporation of India

Dredging Corporation of India Limited provides dredging services to various ports, the Indian navy, fishing harbors, and other maritime organizations in India.

Solid track record with excellent balance sheet.