Stock Analysis

Morepen Laboratories (NSE:MOREPENLAB) Seems To Use Debt Quite Sensibly

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Morepen Laboratories Limited (NSE:MOREPENLAB) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Morepen Laboratories

What Is Morepen Laboratories's Debt?

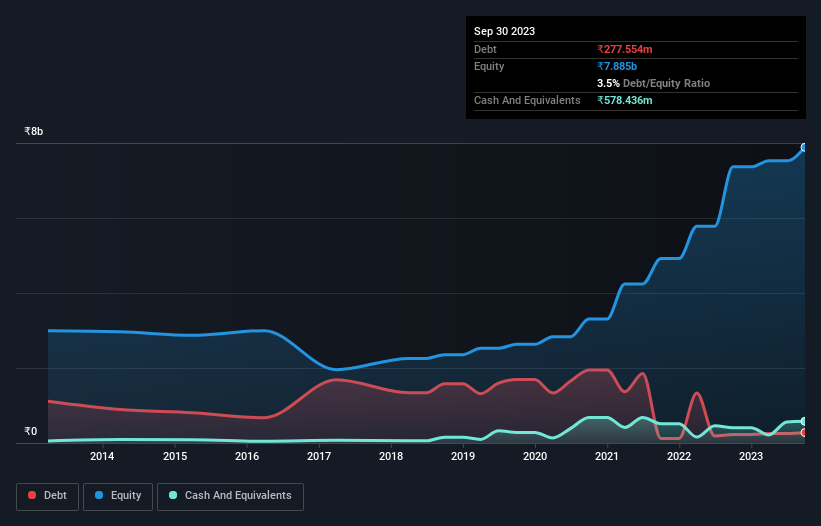

The image below, which you can click on for greater detail, shows that at September 2023 Morepen Laboratories had debt of ₹277.6m, up from ₹228.1m in one year. However, its balance sheet shows it holds ₹578.4m in cash, so it actually has ₹300.9m net cash.

How Strong Is Morepen Laboratories' Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Morepen Laboratories had liabilities of ₹3.66b due within 12 months and liabilities of ₹390.4m due beyond that. On the other hand, it had cash of ₹578.4m and ₹2.85b worth of receivables due within a year. So it has liabilities totalling ₹626.8m more than its cash and near-term receivables, combined.

Of course, Morepen Laboratories has a market capitalization of ₹22.2b, so these liabilities are probably manageable. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. Despite its noteworthy liabilities, Morepen Laboratories boasts net cash, so it's fair to say it does not have a heavy debt load!

The good news is that Morepen Laboratories has increased its EBIT by 2.1% over twelve months, which should ease any concerns about debt repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Morepen Laboratories will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Morepen Laboratories has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last three years, Morepen Laboratories burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Summing Up

While it is always sensible to look at a company's total liabilities, it is very reassuring that Morepen Laboratories has ₹300.9m in net cash. On top of that, it increased its EBIT by 2.1% in the last twelve months. So we are not troubled with Morepen Laboratories's debt use. Over time, share prices tend to follow earnings per share, so if you're interested in Morepen Laboratories, you may well want to click here to check an interactive graph of its earnings per share history.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're helping make it simple.

Find out whether Morepen Laboratories is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:MOREPENLAB

Morepen Laboratories

Morepen Laboratories Limited develops, manufactures, markets, and sells active pharmaceutical ingredients (APIs), formulations, and home health products in India, the United States, and internationally.

Flawless balance sheet with solid track record.