SEHK's August 2024 Value Picks: 3 Stocks Trading Below Estimated Worth

Reviewed by Simply Wall St

As global markets react to potential interest rate cuts and economic updates, the Hong Kong market has seen a mix of cautious sentiment and selective optimism. In this environment, identifying undervalued stocks becomes crucial for investors looking to capitalize on discrepancies between market prices and intrinsic values.

Top 10 Undervalued Stocks Based On Cash Flows In Hong Kong

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Best Pacific International Holdings (SEHK:2111) | HK$2.30 | HK$4.34 | 47.1% |

| Bosideng International Holdings (SEHK:3998) | HK$3.87 | HK$6.75 | 42.6% |

| ANTA Sports Products (SEHK:2020) | HK$69.05 | HK$135.46 | 49% |

| BYD Electronic (International) (SEHK:285) | HK$30.15 | HK$53.17 | 43.3% |

| Inspur Digital Enterprise Technology (SEHK:596) | HK$3.26 | HK$5.69 | 42.7% |

| Pacific Textiles Holdings (SEHK:1382) | HK$1.52 | HK$2.85 | 46.6% |

| Shanghai INT Medical Instruments (SEHK:1501) | HK$28.20 | HK$56.36 | 50% |

| Q Technology (Group) (SEHK:1478) | HK$4.96 | HK$9.73 | 49% |

| iDreamSky Technology Holdings (SEHK:1119) | HK$2.16 | HK$4.12 | 47.6% |

| Vobile Group (SEHK:3738) | HK$1.57 | HK$2.70 | 41.8% |

Underneath we present a selection of stocks filtered out by our screen.

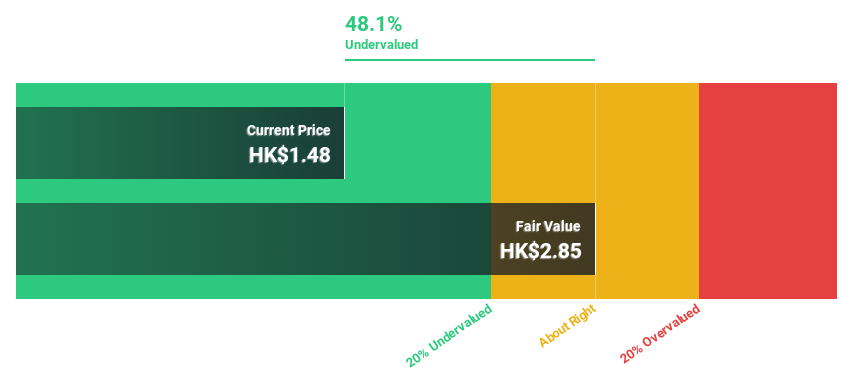

Pacific Textiles Holdings (SEHK:1382)

Overview: Pacific Textiles Holdings Limited manufactures and trades textile products across various regions including China, Vietnam, Bangladesh, and the United States with a market cap of HK$2.12 billion.

Operations: The company generates HK$4.67 billion in revenue from the manufacturing and trading of textile products across its various operational regions.

Estimated Discount To Fair Value: 46.6%

Pacific Textiles Holdings is trading at HK$1.52, significantly below its estimated fair value of HK$2.85, indicating it may be undervalued based on cash flows. Despite a decrease in net income to HK$167.12 million for the year ended March 31, 2024, earnings are forecast to grow significantly at 37.67% per year over the next three years, outpacing the Hong Kong market's growth rate of 10.9%. However, profit margins have declined from last year's figures and the dividend coverage remains weak due to insufficient earnings and free cash flows.

- Our earnings growth report unveils the potential for significant increases in Pacific Textiles Holdings' future results.

- Dive into the specifics of Pacific Textiles Holdings here with our thorough financial health report.

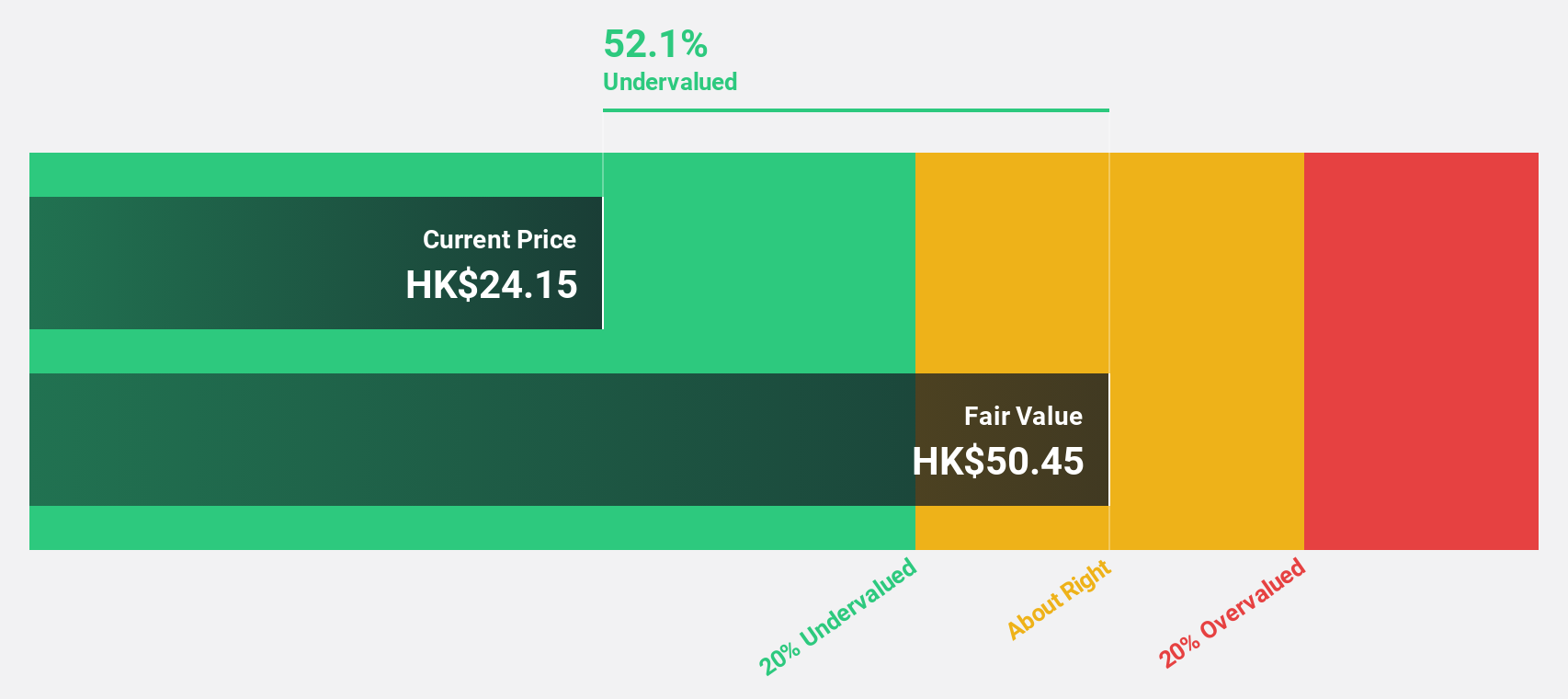

Shanghai INT Medical Instruments (SEHK:1501)

Overview: Shanghai INT Medical Instruments Co., Ltd. (SEHK:1501) operates in the medical instruments sector and has a market cap of HK$4.94 billion.

Operations: Shanghai INT Medical Instruments generates revenue primarily from its Cardiovascular Interventional Business, amounting to CN¥718.71 million.

Estimated Discount To Fair Value: 50%

Shanghai INT Medical Instruments is trading at HK$28.2, well below its estimated fair value of HK$56.36, indicating significant undervaluation based on cash flows. Recent earnings for the half year ended June 30, 2024, showed sales of CNY 392.32 million and net income of CNY 100.54 million, both up from the previous year. Earnings are forecast to grow at a robust 27.2% annually over the next three years, outpacing market growth rates despite past shareholder dilution and low future return on equity (14.7%).

- In light of our recent growth report, it seems possible that Shanghai INT Medical Instruments' financial performance will exceed current levels.

- Click here to discover the nuances of Shanghai INT Medical Instruments with our detailed financial health report.

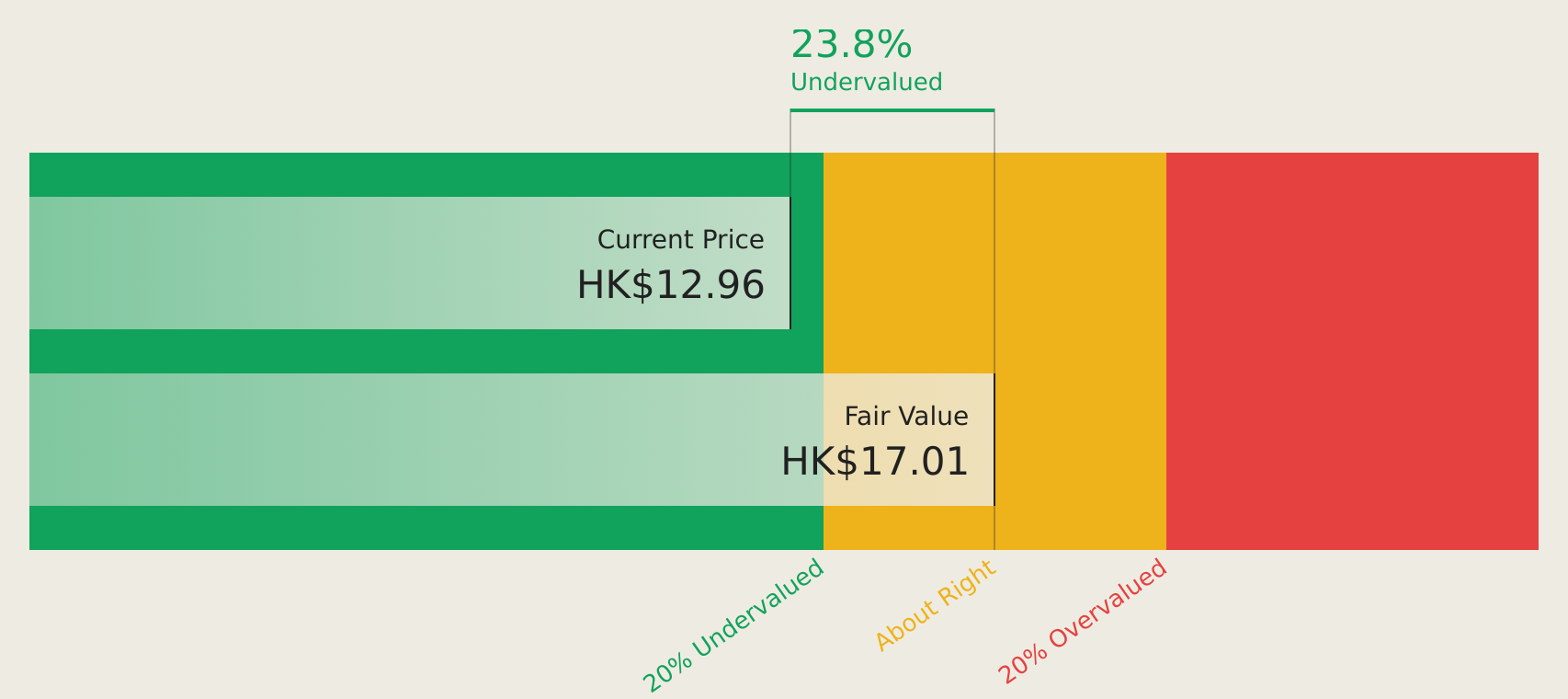

Bank of East Asia (SEHK:23)

Overview: The Bank of East Asia, Limited, along with its subsidiaries, offers a range of banking and financial services and has a market cap of HK$25.64 billion.

Operations: The company generates revenue from several segments, including Corporate Management (HK$104 million), Mainland China Operations (HK$3.44 billion), Overseas, Macau and Taiwan operations (HK$2.91 billion), Hong Kong Operations - Personal Banking (HK$6.81 billion), Hong Kong Operations - Treasury Markets (HK$1.50 billion), and Hong Kong Operations - Wealth Management (HK$459 million).

Estimated Discount To Fair Value: 36.5%

Bank of East Asia is trading 36.5% below its estimated fair value of HK$15.35, with a current price of HK$9.74, reflecting substantial undervaluation based on cash flows. Despite reporting lower net income (HK$2.11 billion) for the half year ended June 30, 2024, compared to the previous year (HK$2.64 billion), earnings are forecast to grow significantly at 24.63% annually over the next three years, surpassing market growth rates and highlighting its potential as an undervalued stock in Hong Kong.

- The growth report we've compiled suggests that Bank of East Asia's future prospects could be on the up.

- Get an in-depth perspective on Bank of East Asia's balance sheet by reading our health report here.

Summing It All Up

- Explore the 37 names from our Undervalued SEHK Stocks Based On Cash Flows screener here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bank of East Asia might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:23

Bank of East Asia

Provides various banking and related financial services.

Reasonable growth potential with adequate balance sheet.