Stock Analysis

- China

- /

- Electronic Equipment and Components

- /

- SZSE:300684

Jones Tech PLC's (SZSE:300684) Stock Going Strong But Fundamentals Look Weak: What Implications Could This Have On The Stock?

Jones Tech's (SZSE:300684) stock is up by a considerable 12% over the past week. However, in this article, we decided to focus on its weak fundamentals, as long-term financial performance of a business is what ultimately dictates market outcomes. Particularly, we will be paying attention to Jones Tech's ROE today.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Put another way, it reveals the company's success at turning shareholder investments into profits.

See our latest analysis for Jones Tech

How Is ROE Calculated?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Jones Tech is:

4.2% = CN¥81m ÷ CN¥1.9b (Based on the trailing twelve months to March 2024).

The 'return' refers to a company's earnings over the last year. Another way to think of that is that for every CN¥1 worth of equity, the company was able to earn CN¥0.04 in profit.

What Is The Relationship Between ROE And Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

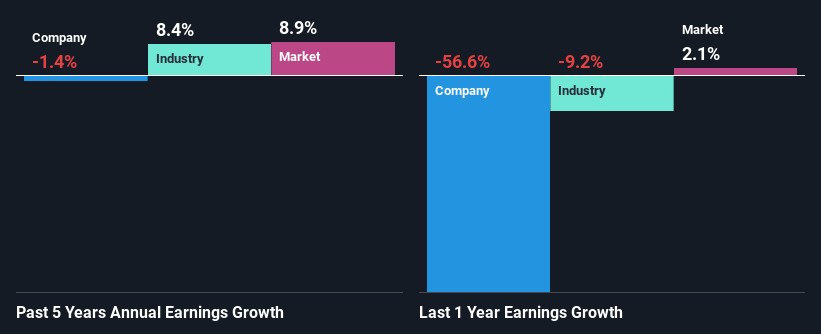

A Side By Side comparison of Jones Tech's Earnings Growth And 4.2% ROE

As you can see, Jones Tech's ROE looks pretty weak. Even compared to the average industry ROE of 6.3%, the company's ROE is quite dismal. As a result, Jones Tech's flat earnings over the past five years doesn't come as a surprise given its lower ROE.

Next, on comparing with the industry net income growth, we found that the industry grew its earnings by 8.4% over the last few years.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. Is Jones Tech fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Jones Tech Using Its Retained Earnings Effectively?

Jones Tech has a high three-year median payout ratio of 95% (or a retention ratio of 4.9%), meaning that the company is paying most of its profits as dividends to its shareholders. This does go some way in explaining why there's been no growth in its earnings.

Moreover, Jones Tech has been paying dividends for six years, which is a considerable amount of time, suggesting that management must have perceived that the shareholders prefer dividends over earnings growth.

Conclusion

Overall, we would be extremely cautious before making any decision on Jones Tech. Particularly, its ROE is a huge disappointment, not to mention its lack of proper reinvestment into the business. As a result its earnings growth has also been quite disappointing. With that said, we studied the latest analyst forecasts and found that while the company has shrunk its earnings in the past, analysts expect its earnings to grow in the future. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

Valuation is complex, but we're helping make it simple.

Find out whether Jones Tech is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300684

Jones Tech

Jones Tech PLC provides materials solutions for intelligent electronic equipment in Asia, Europe, and America.

Flawless balance sheet with high growth potential.