- China

- /

- Semiconductors

- /

- SHSE:688052

Chinese Growth Stocks With High Insider Ownership

Reviewed by Simply Wall St

In recent weeks, Chinese stocks have experienced declines amid a light economic calendar and caution surrounding global market events. Despite this, the search for promising growth companies with high insider ownership remains a key strategy for investors looking to capitalize on potential long-term gains. A good stock in this context is often characterized by strong growth prospects and significant insider ownership, which can indicate confidence from those closest to the company's operations.

Top 10 Growth Companies With High Insider Ownership In China

| Name | Insider Ownership | Earnings Growth |

| ShenZhen Woer Heat-Shrinkable MaterialLtd (SZSE:002130) | 18% | 28.7% |

| Ningbo Sunrise Elc TechnologyLtd (SZSE:002937) | 24.3% | 27.7% |

| Western Regions Tourism DevelopmentLtd (SZSE:300859) | 13.9% | 39.2% |

| Arctech Solar Holding (SHSE:688408) | 38.7% | 26.9% |

| Suzhou Shijing Environmental TechnologyLtd (SZSE:301030) | 22% | 54.9% |

| Cubic Sensor and InstrumentLtd (SHSE:688665) | 10.1% | 34.3% |

| Suzhou Sunmun Technology (SZSE:300522) | 36.5% | 63.4% |

| Sineng ElectricLtd (SZSE:300827) | 36.5% | 40.1% |

| UTour Group (SZSE:002707) | 23% | 36.1% |

| BIWIN Storage Technology (SHSE:688525) | 18.8% | 116.8% |

Here we highlight a subset of our preferred stocks from the screener.

Shanghai Baolong Automotive (SHSE:603197)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shanghai Baolong Automotive Corporation manufactures and sells automotive parts and components, with a market cap of CN¥6.08 billion.

Operations: Shanghai Baolong Automotive Corporation generates revenue from the manufacture and sale of automotive parts and components.

Insider Ownership: 32.5%

Revenue Growth Forecast: 24.2% p.a.

Shanghai Baolong Automotive is positioned as a growth company with substantial insider ownership in China. The stock is trading at 55.5% below its estimated fair value, indicating potential undervaluation. Analysts forecast a significant annual earnings growth of 30.14%, outpacing the broader Chinese market's expected growth of 22%. Despite recent earnings growth of 34.4%, concerns exist over debt coverage by operating cash flow and low future return on equity (18%).

- Unlock comprehensive insights into our analysis of Shanghai Baolong Automotive stock in this growth report.

- Upon reviewing our latest valuation report, Shanghai Baolong Automotive's share price might be too pessimistic.

DBAPPSecurity (SHSE:688023)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: DBAPPSecurity Co., Ltd. engages in the research, development, manufacture, and sale of cybersecurity products in China and has a market cap of CN¥2.89 billion.

Operations: DBAPPSecurity's revenue segments include the research, development, manufacture, and sale of cybersecurity products in China.

Insider Ownership: 16.9%

Revenue Growth Forecast: 16.3% p.a.

DBAPPSecurity's projected revenue growth of 16.3% per year outpaces the Chinese market's 13.4%, suggesting competitive positioning. The company is expected to turn profitable within three years, with an annual earnings growth forecast of 81.02%. Trading at 76.1% below its estimated fair value, it offers potential undervaluation benefits despite low future return on equity (3.8%). No substantial insider trading activity has been reported in the last three months.

- Get an in-depth perspective on DBAPPSecurity's performance by reading our analyst estimates report here.

- Our valuation report unveils the possibility DBAPPSecurity's shares may be trading at a discount.

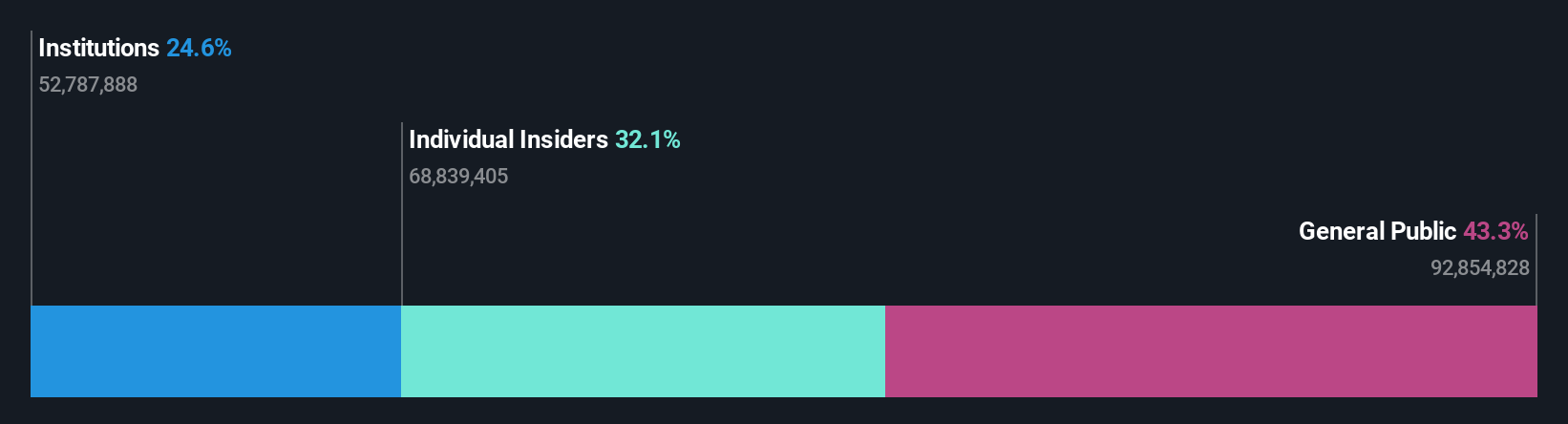

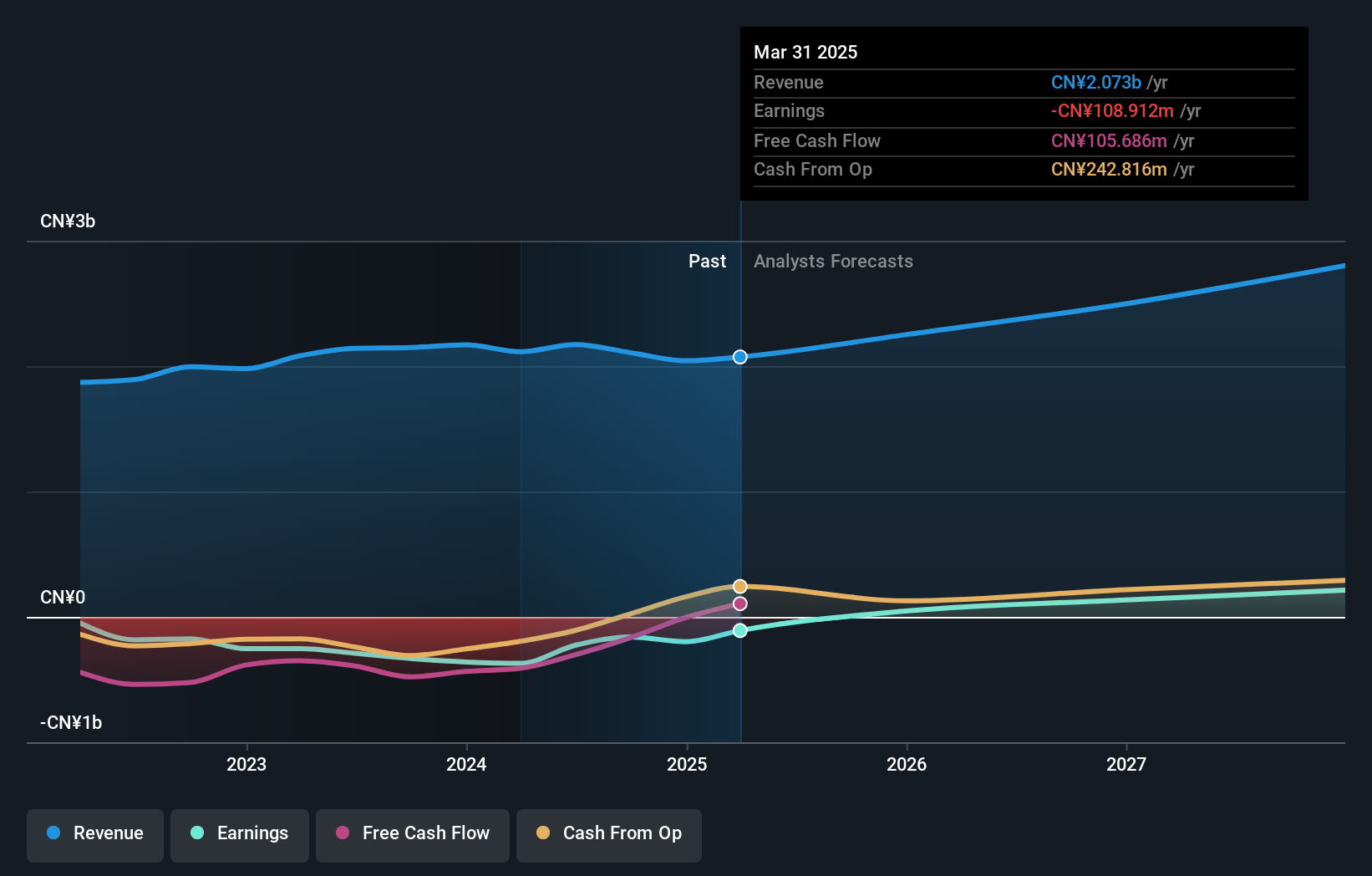

Suzhou Novosense Microelectronics (SHSE:688052)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Suzhou Novosense Microelectronics Co., Ltd. operates in the semiconductor industry, focusing on the design and manufacturing of sensor and analog chips, with a market cap of CN¥13.39 billion.

Operations: Suzhou Novosense Microelectronics generates revenue primarily from the design and manufacturing of sensor and analog chips, with a market cap of CN¥13.39 billion.

Insider Ownership: 25.1%

Revenue Growth Forecast: 31.9% p.a.

Suzhou Novosense Microelectronics is forecast to grow revenue at 31.9% annually, outpacing the Chinese market. Despite a current net loss of CNY 265.25 million for H1 2024, earnings are projected to rise by 116.75% per year, with profitability expected within three years. The stock trades at a slight discount to its estimated fair value but has experienced high volatility recently. No significant insider trading activity has been reported in the past three months.

- Take a closer look at Suzhou Novosense Microelectronics' potential here in our earnings growth report.

- The analysis detailed in our Suzhou Novosense Microelectronics valuation report hints at an inflated share price compared to its estimated value.

Make It Happen

- Delve into our full catalog of 373 Fast Growing Chinese Companies With High Insider Ownership here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688052

Suzhou Novosense Microelectronics

Suzhou Novosense Microelectronics Co., Ltd.

High growth potential with adequate balance sheet.