Stock Analysis

The five-year shareholder returns and company earnings persist lower as Clover (ASX:CLV) stock falls a further 23% in past week

We think intelligent long term investing is the way to go. But no-one is immune from buying too high. For example, after five long years the Clover Corporation Limited (ASX:CLV) share price is a whole 69% lower. We certainly feel for shareholders who bought near the top. And it's not just long term holders hurting, because the stock is down 49% in the last year.

After losing 23% this past week, it's worth investigating the company's fundamentals to see what we can infer from past performance.

View our latest analysis for Clover

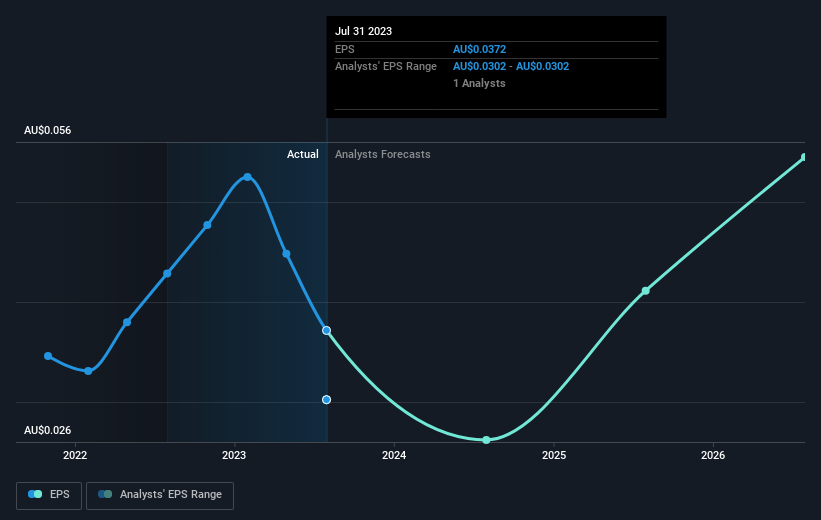

To paraphrase Benjamin Graham: Over the short term the market is a voting machine, but over the long term it's a weighing machine. One imperfect but simple way to consider how the market perception of a company has shifted is to compare the change in the earnings per share (EPS) with the share price movement.

During the five years over which the share price declined, Clover's earnings per share (EPS) dropped by 4.2% each year. This reduction in EPS is less than the 21% annual reduction in the share price. This implies that the market is more cautious about the business these days.

You can see how EPS has changed over time in the image below (click on the chart to see the exact values).

It might be well worthwhile taking a look at our free report on Clover's earnings, revenue and cash flow.

A Different Perspective

While the broader market gained around 16% in the last year, Clover shareholders lost 48% (even including dividends). Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Unfortunately, last year's performance may indicate unresolved challenges, given that it was worse than the annualised loss of 11% over the last half decade. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. It's always interesting to track share price performance over the longer term. But to understand Clover better, we need to consider many other factors. Consider for instance, the ever-present spectre of investment risk. We've identified 1 warning sign with Clover , and understanding them should be part of your investment process.

Of course Clover may not be the best stock to buy. So you may wish to see this free collection of growth stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Australian exchanges.

Valuation is complex, but we're helping make it simple.

Find out whether Clover is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:CLV

Clover

Clover Corporation Limited engages in the business of manufacturing, refining, and sale of tuna oil and encapsulated products in Australia, New Zealand, Asia, Europe, and the Americas.

Excellent balance sheet with reasonable growth potential.