Stock Analysis

- Australia

- /

- Diversified Financial

- /

- ASX:EML

Investors might be losing patience for EML Payments' (ASX:EML) increasing losses, as stock sheds 12% over the past week

The EML Payments Limited (ASX:EML) share price has had a bad week, falling 12%. But that doesn't change the reality that over twelve months the stock has done really well. After all, the share price is up a market-beating 99% in that time.

Since the long term performance has been good but there's been a recent pullback of 12%, let's check if the fundamentals match the share price.

See our latest analysis for EML Payments

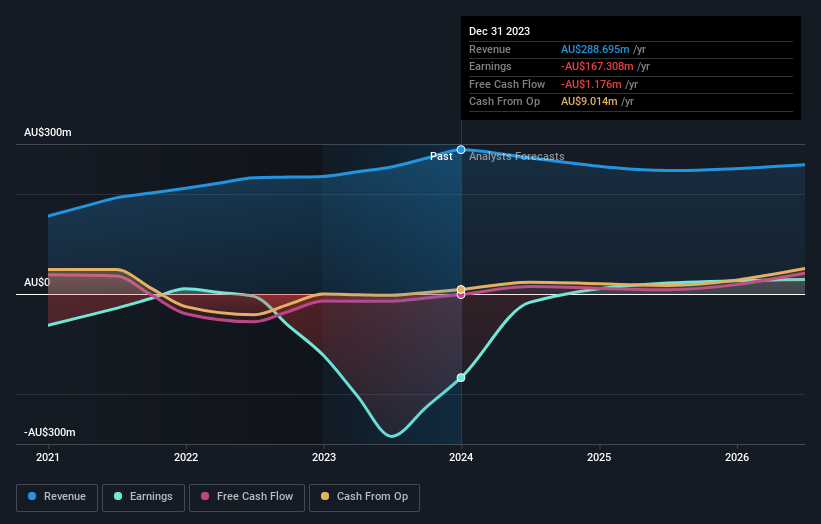

Because EML Payments made a loss in the last twelve months, we think the market is probably more focussed on revenue and revenue growth, at least for now. Shareholders of unprofitable companies usually desire strong revenue growth. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

In the last year EML Payments saw its revenue grow by 23%. We respect that sort of growth, no doubt. Buyers pushed the share price 99% in response, which isn't unreasonable. If revenue stays on trend, there may be plenty more share price gains to come. But it's crucial to check profitability and cash flow before forming a view on the future.

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

We're pleased to report that the CEO is remunerated more modestly than most CEOs at similarly capitalized companies. But while CEO remuneration is always worth checking, the really important question is whether the company can grow earnings going forward. If you are thinking of buying or selling EML Payments stock, you should check out this free report showing analyst profit forecasts.

A Different Perspective

We're pleased to report that EML Payments shareholders have received a total shareholder return of 99% over one year. Notably the five-year annualised TSR loss of 6% per year compares very unfavourably with the recent share price performance. The long term loss makes us cautious, but the short term TSR gain certainly hints at a brighter future. You could get a better understanding of EML Payments' growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies we expect will grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Australian exchanges.

Valuation is complex, but we're helping make it simple.

Find out whether EML Payments is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:EML

EML Payments

Provides payment solutions platform in Australia, Europe, and North America.

Fair value with moderate growth potential.