Stock Analysis

- Japan

- /

- Medical Equipment

- /

- TSE:7747

Despite delivering investors losses of 19% over the past 3 years, Asahi Intecc (TSE:7747) has been growing its earnings

In order to justify the effort of selecting individual stocks, it's worth striving to beat the returns from a market index fund. But if you try your hand at stock picking, your risk returning less than the market. We regret to report that long term Asahi Intecc Co., Ltd. (TSE:7747) shareholders have had that experience, with the share price dropping 21% in three years, versus a market return of about 45%. Furthermore, it's down 19% in about a quarter. That's not much fun for holders.

While the stock has risen 5.0% in the past week but long term shareholders are still in the red, let's see what the fundamentals can tell us.

View our latest analysis for Asahi Intecc

There is no denying that markets are sometimes efficient, but prices do not always reflect underlying business performance. One way to examine how market sentiment has changed over time is to look at the interaction between a company's share price and its earnings per share (EPS).

Although the share price is down over three years, Asahi Intecc actually managed to grow EPS by 26% per year in that time. Given the share price reaction, one might suspect that EPS is not a good guide to the business performance during the period (perhaps due to a one-off loss or gain). Alternatively, growth expectations may have been unreasonable in the past.

It's worth taking a look at other metrics, because the EPS growth doesn't seem to match with the falling share price.

With a rather small yield of just 0.7% we doubt that the stock's share price is based on its dividend. We note that, in three years, revenue has actually grown at a 20% annual rate, so that doesn't seem to be a reason to sell shares. It's probably worth investigating Asahi Intecc further; while we may be missing something on this analysis, there might also be an opportunity.

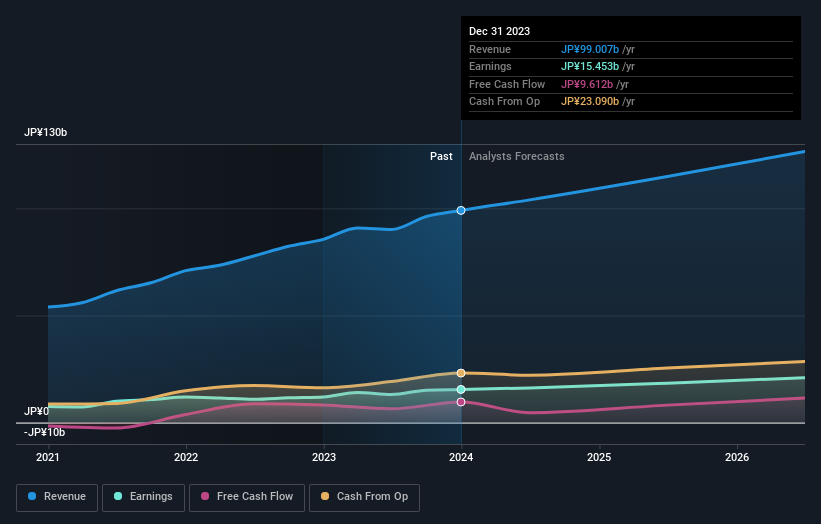

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

Asahi Intecc is well known by investors, and plenty of clever analysts have tried to predict the future profit levels. So it makes a lot of sense to check out what analysts think Asahi Intecc will earn in the future (free analyst consensus estimates)

A Different Perspective

While the broader market gained around 31% in the last year, Asahi Intecc shareholders lost 5.8% (even including dividends). Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Unfortunately, last year's performance may indicate unresolved challenges, given that it was worse than the annualised loss of 2% over the last half decade. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. Before deciding if you like the current share price, check how Asahi Intecc scores on these 3 valuation metrics.

We will like Asahi Intecc better if we see some big insider buys. While we wait, check out this free list of growing companies with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Japanese exchanges.

Valuation is complex, but we're helping make it simple.

Find out whether Asahi Intecc is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:7747

Asahi Intecc

Engages in the development, manufacture, and sale of medical devices in Japan, the United States, Europe, China, and internationally.

Flawless balance sheet with moderate growth potential.