Uranium Price Bolts Ahead Despite Nuclear Headwinds

Reviewed by Michael Paige, Bailey Pemberton

Quote of the Week: “Nuclear power is the only carbon-free energy source we have that can deliver power day and night throughout any season, almost anywhere on earth. And it’s been proven to work at a large scale” - Bill Gates

Recently, we covered the solar and wind industries, which are both currently facing several challenges.

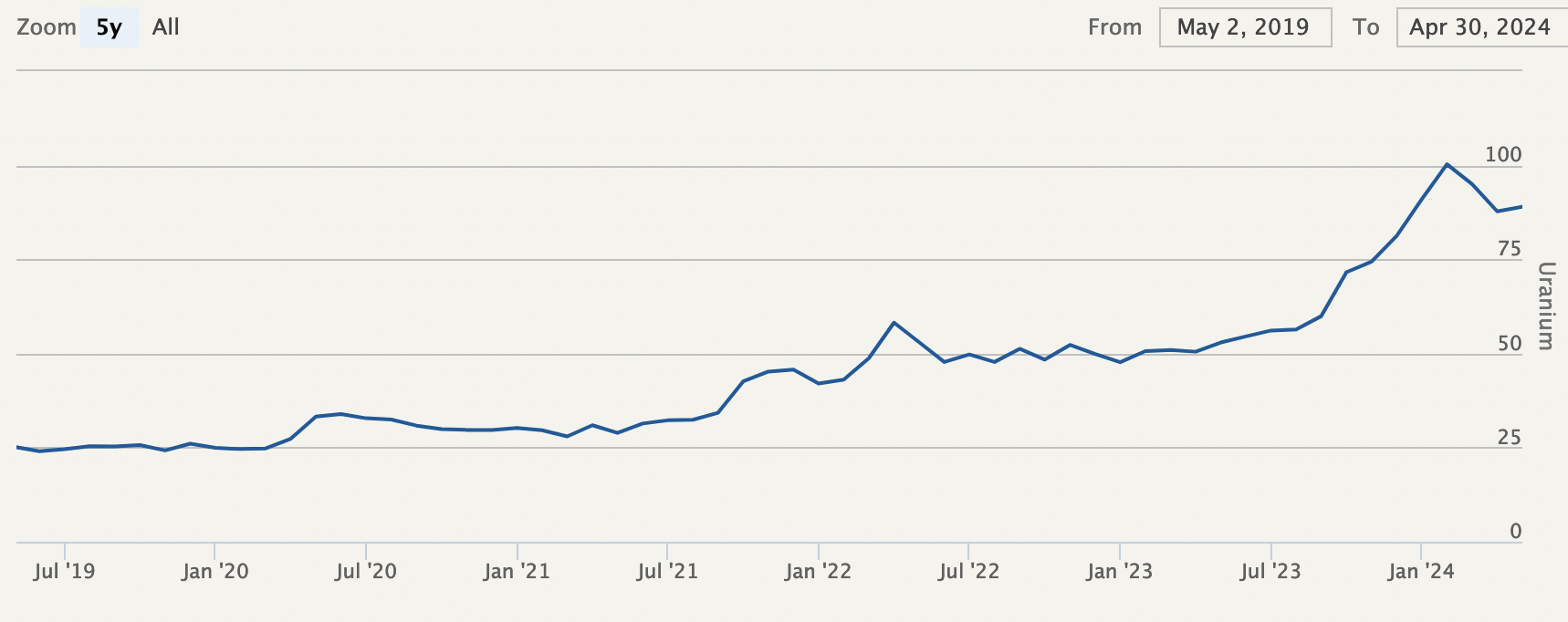

While investors have grown somewhat disillusioned with wind and solar, there seems to be growing optimism around another power source: nuclear energy. And the price of uranium over the last 5 years would indicate as much.

In September, we gave you an overview of the nuclear industry, as well as the more experimental SMRs and fusion projects. Since then, the price of uranium and the stocks linked to uranium mining and nuclear energy generation have continued to rise. So it’s worth delving back into the space to see what’s happening.

In this week’s newsletter, we are checking in on the key developments in the industry, and for those interested, how to get exposure.

What Happened In Markets This Week?

Here’s a quick summary of what’s been going on:

- 🧑⚖️ TikTok Sues To Block The US Ban ( Reuters )

- Our Take: Whether there would be a suitable buyer with adequate funds to buy TikTok is one thing, but getting a sale even allowed by the U.S. and Chinese governments is another. TikTok is trying hard to appease the U.S. government's demands, reportedly spending close to $2bn to implement measures to protect U.S. user's data, and even giving the U.S. government a “ shut-down option ” if it violates any of its obligations. This is a stark reminder of the importance of a political landscape and the local rule of law when you’re investing in international businesses.

- 💸 Apple Announces $110bn Buyback ( Yahoo )

- Our Take: Apple seems to have plenty of cash floating around and not enough appealing reinvestment opportunities, so it has opted for a huge buyback. While services revenue and EPS hit all-time highs, revenue declined due to weakness in iPhone sales, but this was largely expected. Some critics argue the company lacks innovation, and this huge capital return would support that thesis. Either that, or the company is just so profitable, that it can reinvest in everything it needs to, and still have billions left over.

- 🏦 Berkshire’s Annual Shareholder Meeting ( CNBC )

- Our Take: It was a sad meeting given it was the first where Warren didn’t have his long-time friend and business partner Charlie Munger sitting beside him. The key announcements from the day ranged from clarity on succession plans ( Greg Abel running the show when Buffet’s gone ), Berkshire’s 13% reduction in its Apple stake, the complete sale of the Paramount position and the fact that Berkshire’s cash pile could reach over $200bn by next quarter.

- 🇸🇪 Sweden cuts rates for the first time since 2016 ( Reuters )

- Our take: Sweden's Riksbank became the first major central bank to cut rates when it lowered rates from 4% to 3.75%. The ECB is expected to follow soon. Central bankers will be watching to see how this affects prices in Sweden, although the country’s inflation rate is already holding at 2%, so the cut is probably justified.

As for macroeconomic news, here’s some of the key data released recently:

- 🇬🇧 The Bank of England has kept interest rates on hold at 5.35%.

- Two committee members preferred to reduce the rate by 25 basis points, compared to only one member in the previous meeting. According to BoE projections, a decline in the interest rate is expected from 5.25% to 3.75% by the end of Q2 2027.

- Two committee members preferred to reduce the rate by 25 basis points, compared to only one member in the previous meeting. According to BoE projections, a decline in the interest rate is expected from 5.25% to 3.75% by the end of Q2 2027.

- 🇦🇺 The Reserve Bank of Australia has held interest rates at 4.35%.

- This was in line with consensus forecasts, but it could be an early indication that a rate cut is further away than first thought.

- This was in line with consensus forecasts, but it could be an early indication that a rate cut is further away than first thought.

- 🇩🇪 Germany’s balance of trade data was reported for March with an increase from €22.3bn, up from €21.4bn reported in February.

- This fell just short of the €22.4bn consensus forecasts.

- This fell just short of the €22.4bn consensus forecasts.

- 🇨🇳 China's trade surplus decreased to US$72.35bn in April 2024 from $US86.46bn billion twelve months ago.

- The balance of trade came in below consensus forecasts of $US76.7bn. The large decrease was caused by a relatively small increase in exports of 1.5%, compared to a large jump in imports by 8.4%.

🚂 Is the Nuclear Renaissance Gathering Steam?

Judging by the uranium price, one might think the world is once again embracing nuclear energy - particularly with the solar and wind industries being dealt a reality check.

In fact, there have been very few tangible changes in policy around nuclear energy - besides a lot of talk. As it stands, there are still around 70 reactors under construction around the world, mostly in developing economies, and mostly in China. There are another 450 or so reactors in various stages of planning and approval.

✨ That may seem like quite a lot, but not all projects get approved, and it could be decades before the ones that do get approved begin generation. These additions to global nuclear capacity will only just offset the reactors being decommissioned or retired.

One bullish development came last week in the UK, where Europe’s first facility to produce high-assay, low-enriched uranium was announced.

This fuel will be required to power the next-generation reactors the country plans to eventually build. The UK is planning to increase its nuclear production to 24 gigawatts by 2050. To give that some context, China is currently producing 57 gigawatts of nuclear power, with another 30 gigawatts of capacity under construction. China also has another 220 GW at various stages of planning.

⚠️ Nuclear’s Reality Check

China’s goals for nuclear energy may seem ambitious, but they are actually way behind schedule and are likely to be scaled back even more.

In 2011 China announced plans to make nuclear the foundation of its grid, by adding 300 GW over the following 10–20 years.

Since then, the country has instead added more solar and wind capacity than planned and less nuclear power. The initial reason for this was the Fukushima disaster, but economic realities seem to have dominated the industry since then.

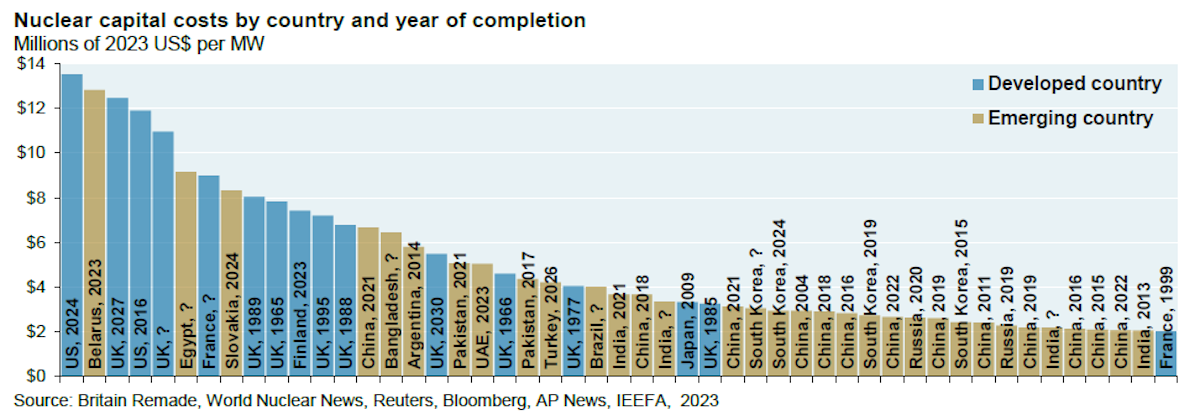

✨ Nuclear power is very affordable when costs are amortized over the life of a reactor, which can be as much as 80 years. But nuclear power is also very expensive when it comes to upfront investments.

The following chart shows that rectors are also becoming increasingly expensive, particularly in developed countries, shown in blue.

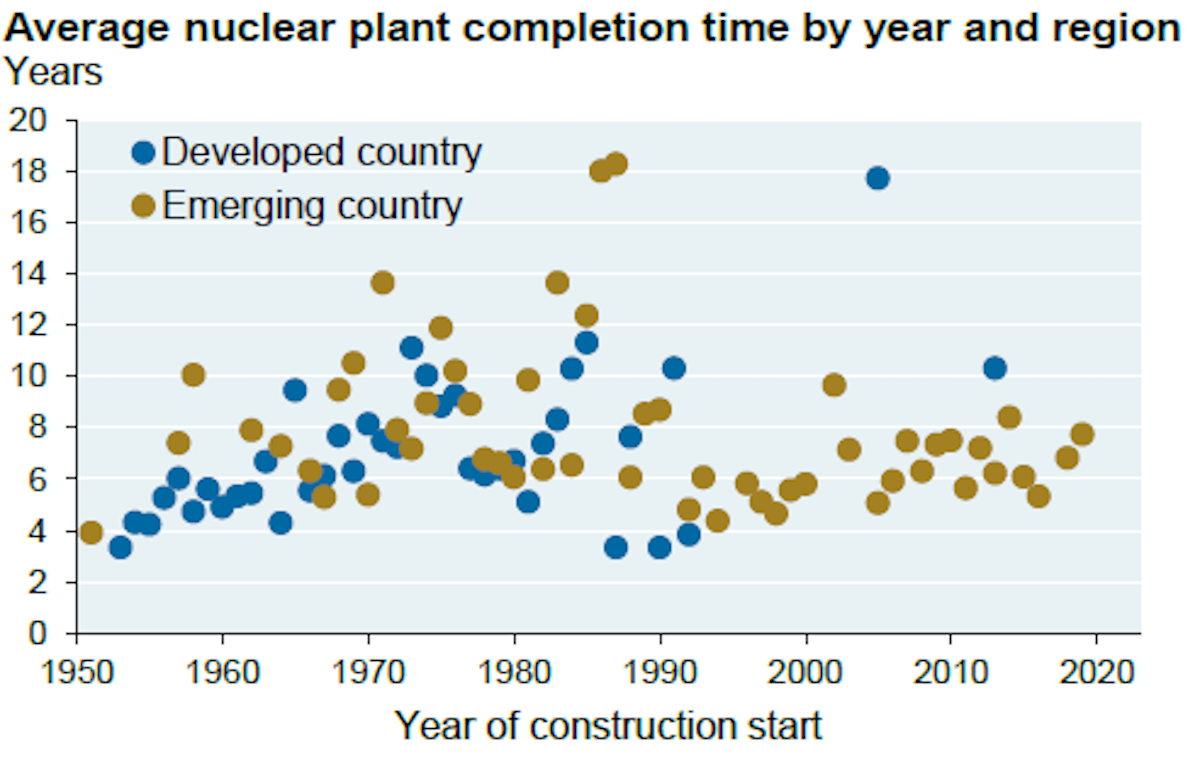

In addition to the high cost, the time it takes to build a reactor is becoming an unknown variable. Projects are typically taking longer than expected to complete, and coming in over budget.

The large investments required for nuclear power are typically made by institutional investors or government agencies.

From their point of view, nuclear projects are very difficult to assess. At best, they will have to wait for eight years before they see positive cash flow. With interest rates at current levels, the hurdle will already be very high when they begin to recoup their investment.

If the project runs over budget or takes longer than anticipated, the hurdle will be even higher. Longer construction periods mean the opportunity costs compound for longer, and over budget means returns have to be shared amongst more investors.

😬 More Bad News For SMRs

Building nuclear reactors is very capital-intensive. SMRs (small modular reactors) could give governments or utilities a way to build up nuclear capacity gradually.

There are now nearly 70 SMR projects in various stages of design and planning around the world. Only four SMRs are currently being constructed (2 in China, 1 in Russia, and 1 in Argentina) and two are operational (in China and Russia).

In October 2023 a new paper estimated the production costs of 19 SMRs. The paper concluded that cost estimates were too optimistic and that none of the 19 concepts were likely to be profitable.

There was more bad news in November when the Utah Associated Municipal Power Systems cancelled the first SMR plant due to go live in the US.

This project by NuScale Power began in 2015 and was supposed to cost $3 billion and produce 600 MW by 2023. By 2021 the cost had risen to $9 billion and the expected output had fallen to 460 MW.

In the UK, Rolls Royce has scaled back its plan to build two factories to build SMRs. Executives said they expect it will take regulators another four and half years to approve its design for an SMR.

SMRs aim to achieve economies of scale by mass-producing small reactors in factories rather than on-site. But if they can’t get to scale, that’s not going to happen. Until something changes, companies in this space should probably be regarded as speculative.

Fusion power, which we covered in detail in September, is also very experimental, and therefore, should probably also be considered speculative.

❓📈 Well, Why Is The Uranium Price Increasing?

So we’ve just covered the difficulties that are encountered with getting profitable and timely nuclear projects off the ground. We’ve also seen that regulatory scrutiny can inhibit the ability of new nuclear projects to come online. You would not be remiss in asking the obvious question: “So, why then is the price for uranium increasing?”

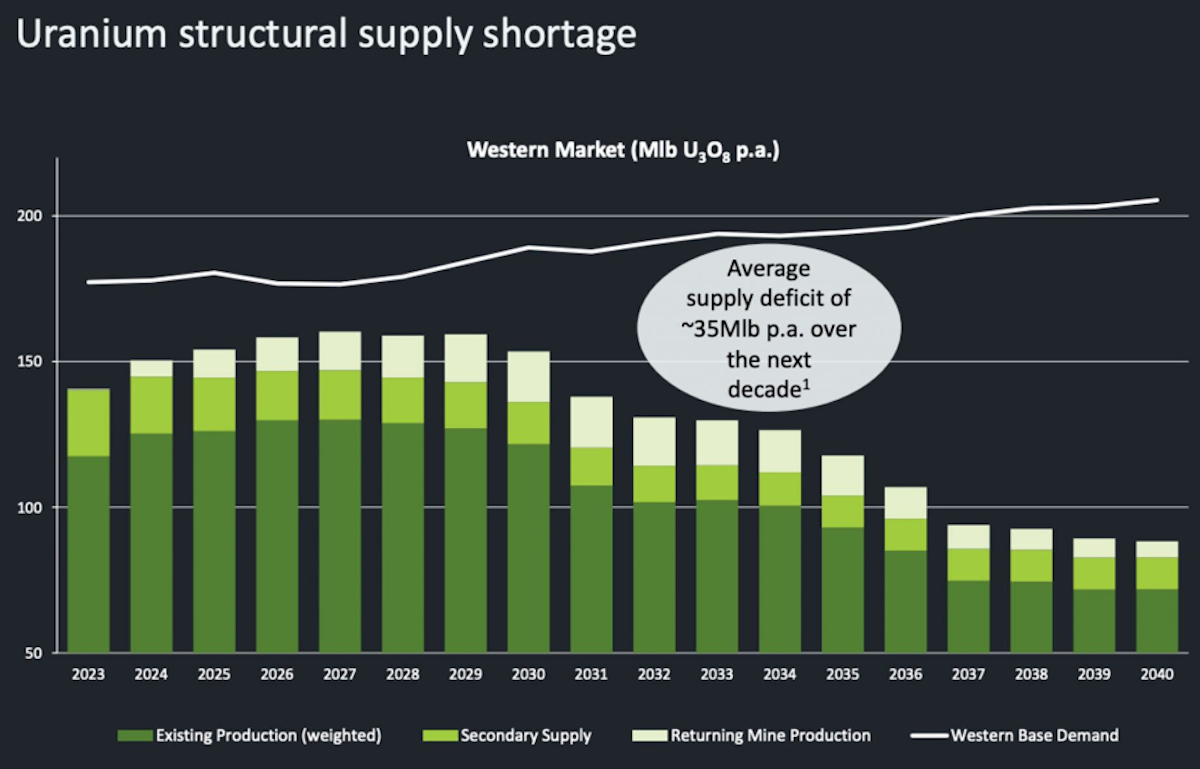

There are two factors at play here. Not to state the obvious, but there are supply-side issues and heightening demand that seem to be applying upward pressure on the Uranium price.

If you look at a list of countries listed by uranium reserves, you’d see a few familiar faces.

Australia stands head and shoulders above the rest with 28% or 1.7m tonnes of the world’s recoverable uranium reserves, followed by Kazakhstan, Canada, Russia and Namibia.

Some of these countries, as you’d expect, are in quite geopolitically sensitive predicaments, which can hurt global supply chains.

Last Tuesday, the US Senate passed legislation to ban the import of Russian uranium. However, it’s not just sanctions impacting the global supply. Niger is set to have produced around 4.1% of global uranium supplies in 2023. Despite that being a marginal increase in production over the previous year, there are expectations this could fall dramatically for 2024 as uncertainty arises due to the recent coup, upsetting supplies bound for Western Europe.

While countries like Australia are in much less of a geopolitically arduous position, there are still political concerns with mining uranium, as evidenced by the Western Australian government’s 2017 ban on new uranium projects.

These issues are exacerbated by a larger issue, according to Greg Cochran, the managing director of Aurora Energy Metals. Cochran details that over the last 15 years, little work had been done in exploration or building new mines and so the industry is now “playing catch up”.

Tightening supply isn’t the only thing keeping the uranium price buoyant.

While we have spoken at length about the difficulties in getting a nuclear project up and running, there is one truth that remains. Nuclear energy is the cleanest, most efficient and least dangerous source of energy at scale, and it’s still essential in helping to achieve global Net-Zero targets.

The reinvigorated interest in scaling up nuclear energy production recently has also contributed significantly to the price increases.

Even though there’s no guarantee that much of the planned uranium projects will come to fruition, the US Department of Energy’s $500m commitment to building a domestic uranium supply only supports the bullish sentiment around the mineral.

💡 The Insight: Just Like The AI Value Chain, Consider The Nuclear Value Chain

Just like we discussed the AI value chain back in February, there are several different ways to invest in nuclear energy or uranium, including uranium itself, uranium producers, utilities, and equipment manufacturers.

The dynamics that drive returns for each of these investments are very different, and it’s important to understand what you are actually buying.

If you believe in the long-term potential of nuclear energy and those involved in producing it, then some of these parts of the value chain may take your interest.

⛏️ Uranium and Uranium Miners

Some of the strongest price performance of the last year has been from the companies that explore, mine and process uranium.

The supply deficit is expected to increase at the end of the decade as current mines become depleted. But, uranium is a commodity, and like all commodities, higher prices lead to new investment and output. Forecasts like the one above often underestimate new production.

If you’re keen to invest in producers, make sure they are earning healthy margins (like the world’s largest producer, JSC National Atomic Company Kazatomprom ) and that their costs aren’t rising faster than revenues.

Some other uranium miners include:

- Uranium Royalty Corp. ( NASDAQ:UROY )

- Energy Fuels Inc. ( NYSE:UUUU )

- Ur-Energy Inc. ( NYSE:URG )

- Denison Mines Corp. ( NYSE:DNN )

- Cameco Corporation ( NYSE:CCJ )

- Uranium Energy Corp. ( NYSE:UEC )

- NexGen Energy Ltd. ( NYSE:NXE )

- BHP Group ( NYSE:BHP )

⚡ Utilities

Electric utilities have varying exposure to nuclear energy, and it’s often just one of the ways they generate power. Ultimately, they are selling electricity - and they have to sell it at a profit regardless of the source.

Some names with exposure include:

- NuScale Power Corporation ( NYSE:SMR )

- Duke Energy Corporation ( NYSE:DUK )

- Dominion Energy, Inc. ( NYSE:D )

- DTE Energy Company ( NYSE:DTE )

- Entergy Corporation ( NYSE:ETR )

- Constellation Energy ( NYSE:CEG )

⚒️ Picks and Shovels

Several companies sell equipment or provide services to nuclear plants. These companies earn revenue by providing equipment and services to existing plants, as well as to new plants. They would benefit from an increase in investment and are far less dependent on the price of electricity or uranium.

- Centrus Energy Corp. ( NYSE:LEU )

- BWX Technologies, Inc. ( NYSE:BWXT )

- Brookfield Renewable Partners ( NYSE:BEP )

Considering AI data centres are incredibly power intensive, and nuclear seems like an appealing power source for them, some believe that some nuclear stocks are well positioned to benefit from the expansion in data centres.

Key Events During the Next Week

Investors will be focussed on some key inflation data this week:

Tuesday

-

🇬🇧 UK unemployment is forecast to remain at 4.2%

-

🇺🇸 US producer price inflation is expected to rise from 2.1% to 2.2%, while core PPI is expected to remain at 2.4%

Wednesday

-

🇺🇸 US retail sales are forecast to have risen 0.3% in the year to April, down from 0.7% the prior month

-

🇺🇸 US consumer inflation is expected to remain at 3.5%, while analysts expect the core inflation rate to fall 0.1% to 3.7%.

Thursday

- 🇺🇸 US Building permits are expected to remain at 1.47 million, while housing starts are forecast to partially reverse March’s sharp decline with an increase of 3.7% in April

- 🇯🇵 Preliminary estimates are expected to show Japan’s GDP growing by just 0.1% in the first quarter.

We are now about halfway through earnings season for large-cap companies, with the first of the retailers and Chinese tech companies due to report:

- Home Depot

- Walmart

- Cisco

- Applied Materials

- Alibaba

- Baidu

- Tencent Music Entertainment

- JD.com

- Sony

- Sea Ltd

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. Any comments below from SWS employees are their opinions only, should not be taken as financial advice and may not represent the views of Simply Wall St. Unless otherwise advised, SWS employees providing commentary do not own a position in any company mentioned in the article or in their comments.We provide analysis based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Richard Bowman

Richard is an analyst, writer and investor based in Cape Town, South Africa. He has written for several online investment publications and continues to do so. Richard is fascinated by economics, financial markets and behavioral finance. He is also passionate about tools and content that make investing accessible to everyone.