Advertisement

- United States

- /

- Electric Utilities

- /

- NYSE:PCG

Has PG&E’s Settlement Progress Changed the Stock’s Value Narrative in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

- Curious if PG&E’s share price offers real value right now? You are not alone, as many investors are looking under the hood to see what is driving this utility stock.

- PG&E shares moved up by 2.9% in the past week and 2.3% over the last month, but they are still down 19.4% year-to-date and 25% over the last twelve months. This hints at lingering uncertainty and changing risk perceptions.

- Recent headlines have centered around settlement progress related to wildfire liabilities, which has reassured some markets and attracted a fresh wave of investor interest. These news items provide important context for the recent price moves as the company seeks to strengthen its position while managing legacy risks.

- On our six-point value framework, PG&E scores a 4 out of 6 for being undervalued. This is a solid showing, but not the whole story. Next, we will dive into the different valuation methods used, and at the end of the article, explore a more holistic way to really understand value.

Find out why PG&E's -25.0% return over the last year is lagging behind its peers.

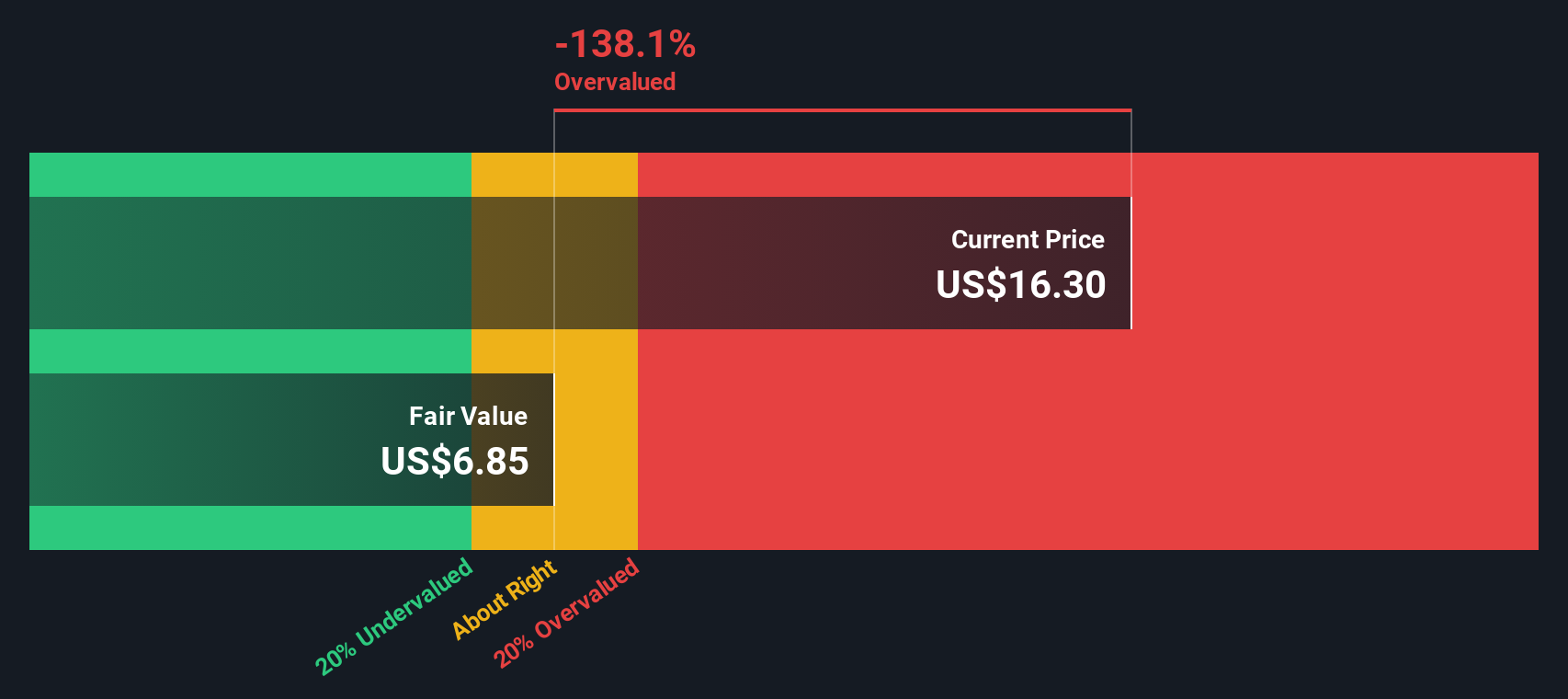

Approach 1: PG&E Dividend Discount Model (DDM) Analysis

The Dividend Discount Model (DDM) estimates a company's fair value by projecting future dividend payments and discounting them back to the present. This approach relies heavily on the sustainability and anticipated growth of those dividends rather than relying on cash flows or earnings alone.

For PG&E, the DDM incorporates a projected dividend per share (DPS) of $0.25, with the company targeting an average return on equity (ROE) of 8.45% and a dividend payout ratio around 3.47. Growth estimates for dividends are capped at 3.26%, although a longer-term expected growth rate is closer to 8.15%.

Using this model, PG&E's estimated intrinsic value is calculated to be $6.85 per share. However, this is significantly below the current share price, with the DDM suggesting the stock is about 135.5% overvalued relative to its underlying dividend prospects. This indicates that, at present levels, the market price may be running well ahead of the company's dividend growth fundamentals.

Result: OVERVALUED

Our Dividend Discount Model (DDM) analysis suggests PG&E may be overvalued by 135.5%. Discover 920 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: PG&E Price vs Earnings

The Price-to-Earnings (PE) ratio is a commonly used valuation multiple for profitable companies, as it quickly tells investors how much they are paying for a company’s current earnings. Because PG&E is now generating positive earnings, the PE ratio offers an immediate sense of the market’s expectations for its future growth or risk profile.

Not all companies warrant the same PE multiple. Higher growth prospects, stable profit margins, and low risk profiles typically result in a higher PE ratio being considered fair. In contrast, companies with volatile earnings, slower growth, or increased risk exposure will generally trade at lower PE multiples.

Currently, PG&E trades at a PE ratio of 13.6x. This is well below the average for its electric utility peers, which sits at 21.6x, and below the broader industry average of 20.9x. At first glance, this suggests a notable valuation discount compared to the competition.

To move beyond these basic comparisons, Simply Wall St calculates a “Fair Ratio” for PG&E of 26.1x. This proprietary estimate considers a blend of factors including the company’s market capitalization, earnings growth outlook, risk profile, profit margin, and the characteristics of the industry. Unlike simple peer or industry averages, the Fair Ratio offers a more nuanced benchmark that is tailored to the actual situation facing PG&E.

With PG&E’s PE ratio at 13.6x and a Fair Ratio that is nearly double at 26.1x, the shares appear to be priced well below what would reasonably be expected, all else being equal.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your PG&E Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives, an approach that lets you attach your own story and perspective to the numbers behind a company’s future.

A Narrative lets you connect what you believe about PG&E’s future, such as its earnings growth, margins, and risks, with your own financial forecast. You can then see what fair value would result from those assumptions.

This is more than just crunching numbers. Narratives allow you to express why you think PG&E is undervalued, overvalued, or fairly priced by capturing how all those industry updates, news, and forecasts shape your outlook.

Available through Simply Wall St’s Community page (where millions of investors share their views), Narratives make it simple to map your thesis to a fair value and instantly compare it to the current share price, helping you decide when to act.

Because Narratives update dynamically in response to new developments, like earnings releases or regulatory changes, you always have a living, personal investment view at your fingertips.

For example, one PG&E Narrative might focus on robust data center-driven demand growth and resilient margins, yielding a fair value of $23 per share. A more cautious Narrative might highlight regulatory and wildfire risks and land at just $17 per share.

Do you think there's more to the story for PG&E? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PCG

PG&E

Through its subsidiary, Pacific Gas and Electric Company, engages in the sale and delivery of electricity and natural gas to customers in northern and central California, the United States.

Good value with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative