Advertisement

- United States

- /

- Electric Utilities

- /

- NYSE:IDA

How Investors May Respond To IDACORP (IDA) Raising Earnings Outlook After Strong Q3 Profitability

Simply Wall St

Reviewed by Sasha Jovanovic

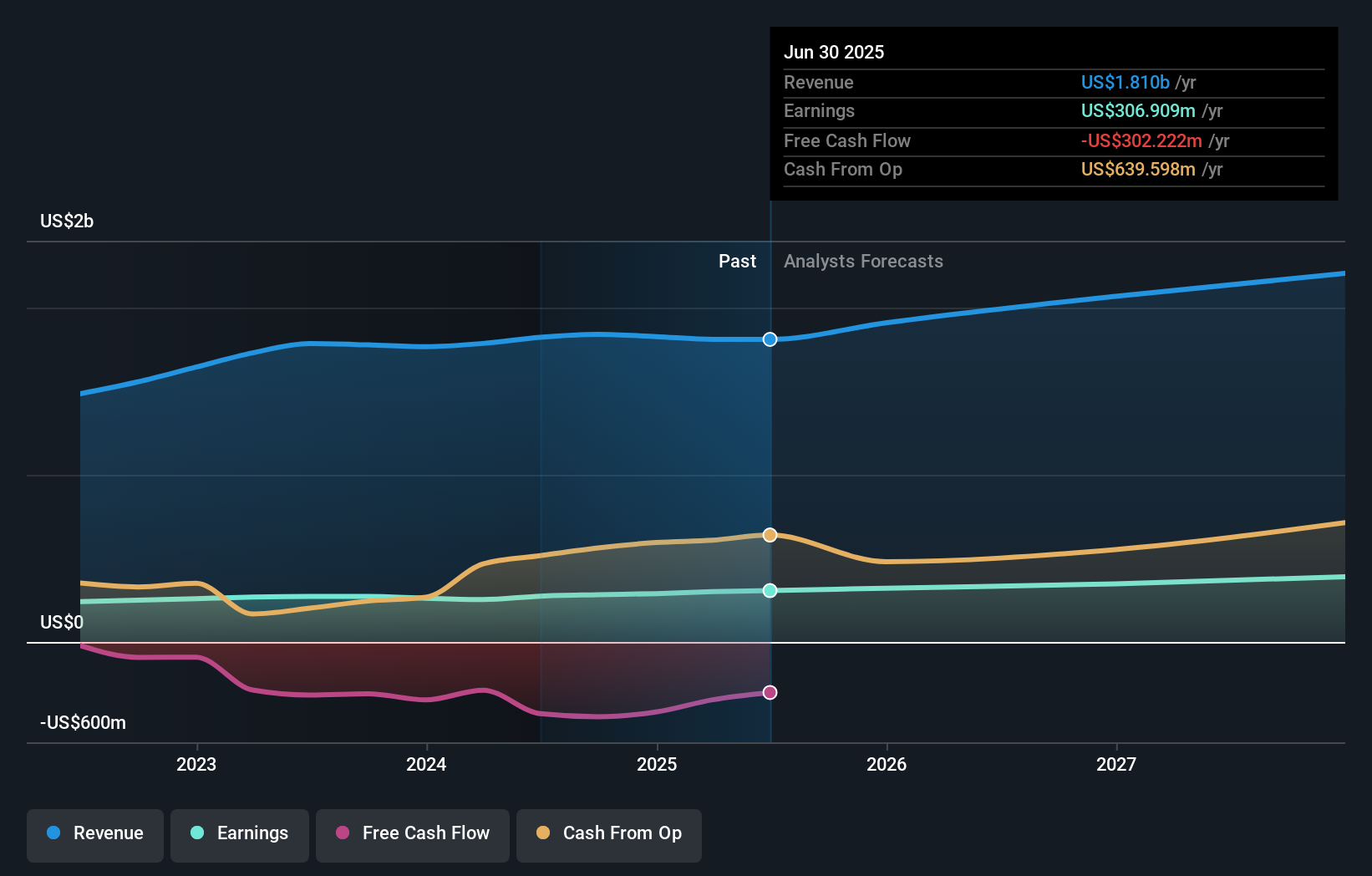

- IDACORP, Inc. recently reported its third quarter 2025 results, showing increased net income and raised its full-year earnings guidance to US$5.80–US$5.90 per diluted share, up from its previous range of US$5.70–US$5.85.

- This upward revision in guidance followed stronger profitability despite slightly lower sales and revenue, underscoring improved operational performance and management's confidence in the company's outlook.

- We'll examine how IDACORP's boosted earnings outlook and recent results affect its investment narrative, especially regarding earnings stability.

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

IDACORP Investment Narrative Recap

To be a shareholder in IDACORP, you need to believe in the company's ability to maintain steady earnings in a sector shaped by long-term customer growth, significant infrastructure investment, and evolving regulatory frameworks. The recent upward revision to earnings guidance is a short-term catalyst, but it does not materially reduce the biggest risk facing the business: the need for regulatory cost recovery as capital spending and debt rise with increased demand.

Among several recent announcements, the highlight is IDACORP's move to raise its full-year 2025 earnings guidance following strong net income for the third quarter, despite soft revenue. This guidance increase directly reinforces the company's narrative of earnings stability amid changing conditions and suggests the core business remains resilient through near-term weather and market variability.

However, even with improved guidance, regulatory approval around cost recovery remains a crucial issue investors should keep in mind, especially if rising capital needs...

Read the full narrative on IDACORP (it's free!)

IDACORP's narrative projects $2.3 billion revenue and $441.8 million earnings by 2028. This requires 8.3% yearly revenue growth and a $134.9 million earnings increase from $306.9 million.

Uncover how IDACORP's forecasts yield a $139.00 fair value, a 7% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members offered three estimates for IDACORP's fair value, ranging from US$103.21 to US$139. Customer growth and accelerating capital investment were flagged by analysts as meaningful drivers that could influence these opinions. Explore several viewpoints to see how consensus can diverge.

Explore 3 other fair value estimates on IDACORP - why the stock might be worth as much as 7% more than the current price!

Build Your Own IDACORP Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your IDACORP research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free IDACORP research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate IDACORP's overall financial health at a glance.

Looking For Alternative Opportunities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've found 16 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Rare earth metals are the new gold rush. Find out which 35 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:IDA

IDACORP

Engages in the generation, transmission, distribution, purchase, and sale of electric energy in the United States.

Solid track record average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|7.6% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor