Advertisement

- United States

- /

- Electric Utilities

- /

- NYSE:DUK

Duke Energy (DUK): Assessing Valuation as Shares Tick Higher Following Strong YTD Performance

Simply Wall St

Reviewed by Simply Wall St

Duke Energy (DUK) shares edged slightly higher today, drawing attention from investors who are weighing whether recent moves in the stock present a good value opportunity. The company's diversified utility operations continue to underpin its steady performance.

See our latest analysis for Duke Energy.

Duke Energy’s share price recently ticked higher to $123.43, putting its momentum back on investors’ radar after a solid start to the year. While the 1-day share price return was 1.23%, what also stands out is the 14.48% gain year-to-date and a five-year total shareholder return of 59.96%, highlighting how steady utility demand and measured growth strategies have rewarded patient shareholders over time.

If you’re looking to broaden your search after observing Duke Energy’s steady move, now is an opportune time to explore other fast-growing companies with high insider ownership using our fast growing stocks with high insider ownership.

With a strong track record and the stock trading around 11% below analyst price targets, the question remains: Is Duke Energy undervalued right now, or is the market already accounting for its growth prospects?

Most Popular Narrative: 10.2% Undervalued

Duke Energy’s most followed narrative sets a fair value substantially above its last close of $123.43, suggesting market participants are missing constructive catalysts on the horizon.

Major economic development wins (such as AWS's $10B data center in North Carolina), paired with accelerated migration and manufacturing demand in Duke's service territory, are expected to drive robust, multi-year load and volume growth. This supports higher revenues and long-term EPS growth. Supportive state and federal legislation, including the Power Bill Reduction Act in NC and the Energy Security Act in SC, streamlines cost recovery for new generation and grid investments. These measures reduce regulatory lag and improve cash flow and earnings stability over the next decade.

Want to know what’s powering this premium? The narrative centers on a combination of rising earnings, ongoing revenue expansion, and a notable profit margin trajectory. The real surprise is that it projects a valuation multiple comparable to some of the country’s highest-growth companies. Interested in the financial factors behind this outlook? Check out the details that are moving the needle on Duke Energy’s fair value calculation.

Result: Fair Value of $137.47 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, accelerated adoption of distributed energy and rising capital needs could challenge Duke Energy’s revenue growth and put future margins under pressure.

Find out about the key risks to this Duke Energy narrative.

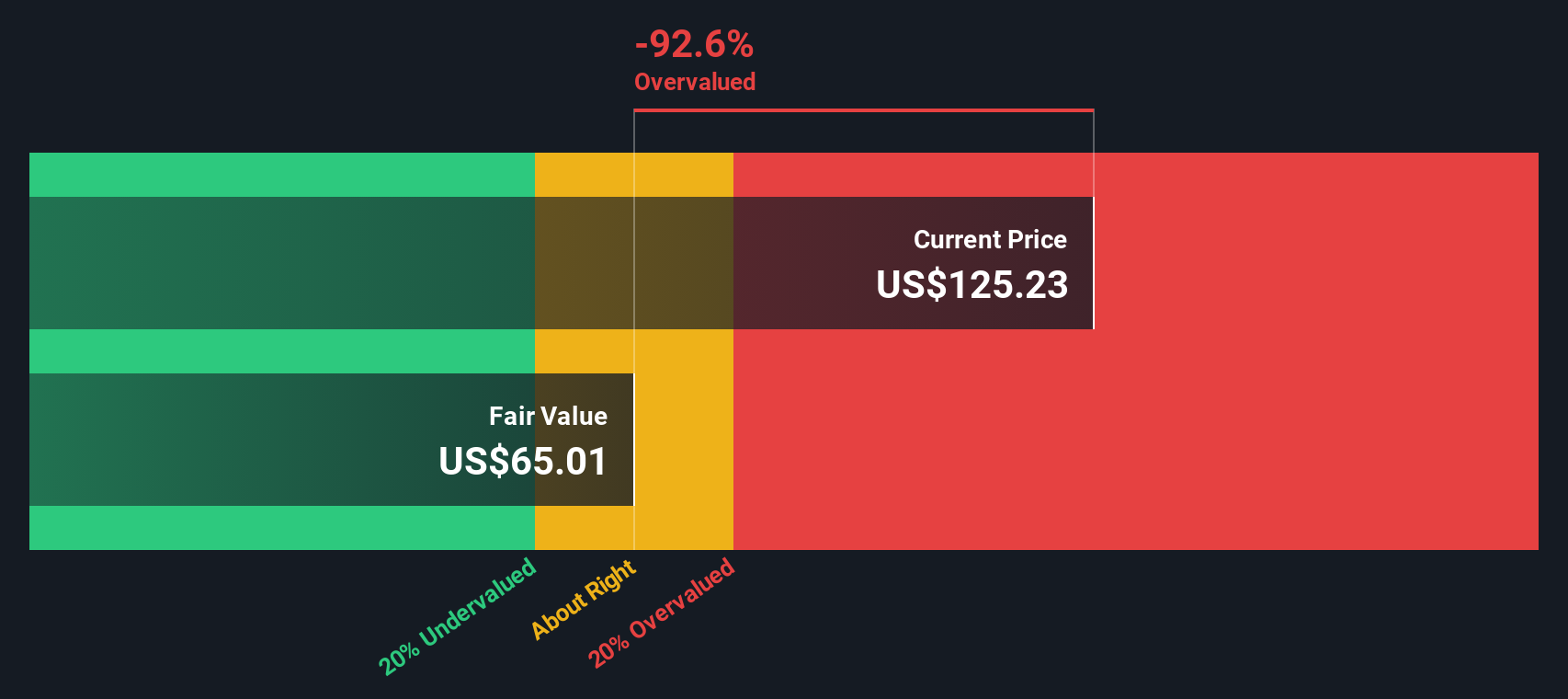

Another View: How Does DCF Stack Up?

While the popular narrative suggests Duke Energy is undervalued based on analyst price targets, our SWS DCF model arrives at a different conclusion. The DCF estimate puts fair value at just $63.17 per share, meaning the stock looks overvalued compared to its current market price. This divergence in outcomes may be due to growth assumptions that could be overly optimistic or to the possibility that the market is expecting catalysts that the cash flow model does not capture.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Duke Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 927 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Duke Energy Narrative

If the conclusions above aren't quite what you had in mind, you can dive into the data and build your own take in just a few minutes. Do it your way.

A great starting point for your Duke Energy research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t limit your strategy to just one stock when the market is full of potential. Secure your next opportunity by targeting fast-moving trends others might miss.

- Capture high yields and stable income by reviewing these 15 dividend stocks with yields > 3%, which is packed with stocks offering robust dividend payouts above 3%.

- Spot tomorrow’s tech winners among these 25 AI penny stocks, where artificial intelligence and rapid innovation are creating powerful investment tailwinds.

- Uncover overlooked gems and seize value before the crowd by browsing these 927 undervalued stocks based on cash flows, filled with companies trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:DUK

Duke Energy

Through its subsidiaries, operates as an energy company in the United States.

Proven track record average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

76 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

90 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

928 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative