Advertisement

- United States

- /

- Other Utilities

- /

- NYSE:CNP

CenterPoint Energy (CNP): Assessing Valuation After Strong Share Price Gains

Simply Wall St

Reviewed by Simply Wall St

CenterPoint Energy (CNP) has been gradually regaining ground, with its stock delivering a solid 27% return year to date and climbing 25% over the past year. The steady gains reflect sustained investor interest over the past three years as well.

See our latest analysis for CenterPoint Energy.

CenterPoint Energy’s 1-year total shareholder return of 25% signals momentum that is hard to ignore, especially as the share price has reached $39.95 following continued strength. With recent weeks quiet on major announcements, the steady climb in both price and returns suggests that investors are recognizing potential for the long term.

If you’re looking to broaden your opportunity set beyond utilities, now might be a smart time to discover fast growing stocks with high insider ownership.

With the share price hovering near all-time highs, investors may be wondering if CenterPoint Energy is trading at a bargain or if the recent rally means the market has already priced in the company’s future growth prospects.

Most Popular Narrative: 6.4% Undervalued

Market optimism is running just ahead of price targets, with CenterPoint Energy’s narrative fair value of $42.67 standing slightly above the last close at $39.95. This setup hints at rising expectations and leaves the question of how much runway is left.

Bullish analysts are encouraged by CenterPoint’s consistent operational execution and the extension of its long-term financial plan, which supports EPS growth targets of 7% to 9% through 2030. Upward revisions to price targets cite strong demand trends, a growing capital plan now totaling $65 billion through 2035, and opportunities from industrial expansion, transmission, population growth, and increased data center load.

Want to know the growth blueprint driving this target? The secret is ambitious earnings expansion tied to significant capital deployment and a large-scale long-term plan. Which assumptions are fueling this premium? Dive deeper for the full story behind these bold projections, without spoilers.

Result: Fair Value of $42.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, regulatory lag and rising debt costs remain potential catalysts that could challenge the optimistic growth outlook currently priced into CenterPoint’s shares.

Find out about the key risks to this CenterPoint Energy narrative.

Another View: Risk from Market Comparisons

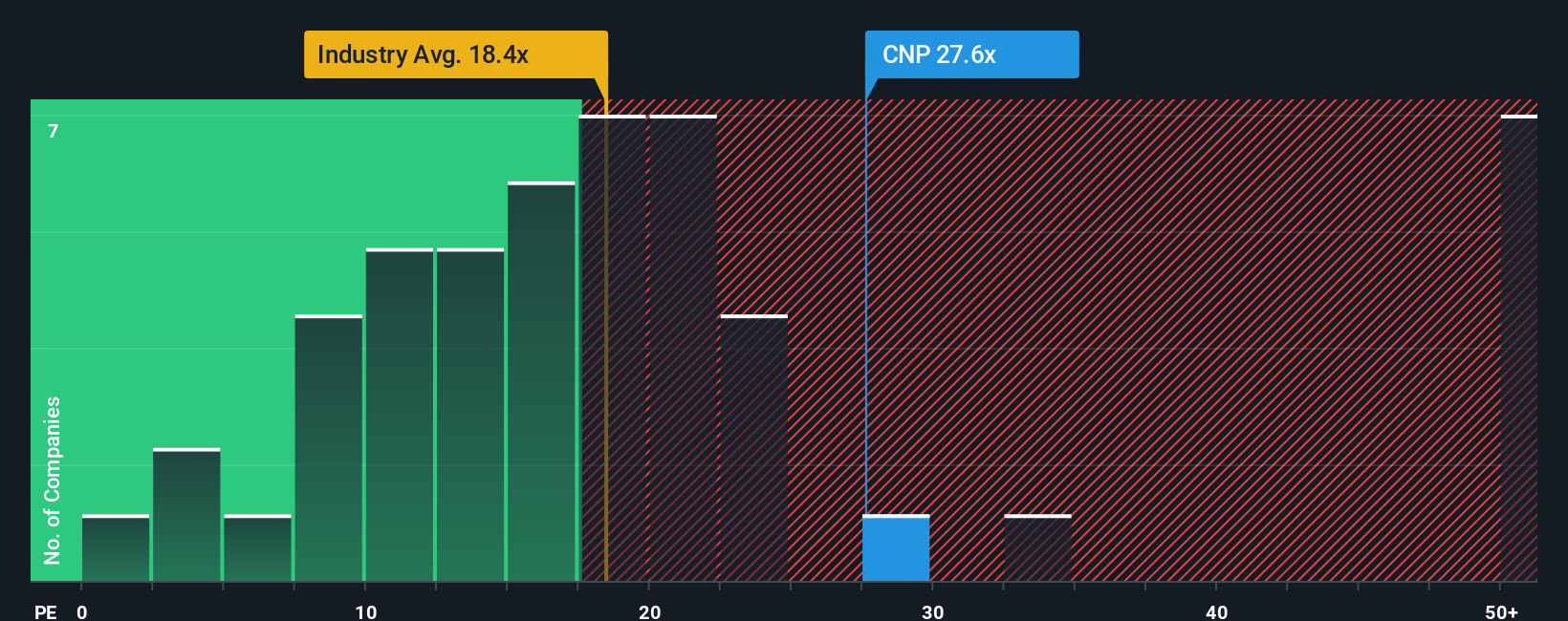

Looking beyond fair value, CenterPoint Energy trades at a price-to-earnings ratio of 25.2x, which is above both its peer average of 21.8x and the global integrated utilities sector at 17.7x. This premium raises questions about valuation risk if market sentiment changes or if industry multiples move toward the fair ratio of 22.5x. Will investors continue to support this higher price, or could momentum slow?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own CenterPoint Energy Narrative

If you want a different angle or believe your own analysis could tell a new story, you can build your own perspective in just a few minutes. Do it your way.

A great starting point for your CenterPoint Energy research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Unlock your next opportunity by using the Simply Wall Street Screener. Make every investment decision count with ideas that give you an edge over the crowd.

- Capture consistent income by reviewing these 15 dividend stocks with yields > 3% offering attractive yields above 3% for income-focused portfolios.

- Tap into rapid tech sector growth by scanning these 25 AI penny stocks. These stocks are redefining entire industries through artificial intelligence breakthroughs.

- Spot tomorrow’s breakout performers among these 925 undervalued stocks based on cash flows based on strong cash flow metrics that indicate untapped upside potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CNP

CenterPoint Energy

Operates as a public utility holding company in the United States.

Solid track record unattractive dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

76 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

45 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative