Advertisement

- United States

- /

- Electric Utilities

- /

- NasdaqGS:CEG

What Rising Demand for Clean Power Means for Constellation Energy’s Valuation in 2025

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Constellation Energy is a bargain right now? You are not alone. Let us walk through why the stock has been attracting extra attention lately.

- Constellation’s share price is up 6.2% this week, but that follows a 10.5% dip over the last month. Still, the stock is up a substantial 48.0% year-to-date and a massive 299.9% over the past three years.

- Recent news about the company’s aggressive push into renewable energy, along with rising demand for clean power, has been a catalyst for investor interest. Many are watching closely as these factors could reshape both risk and growth prospects for the stock.

- Looking purely at our valuation checks, Constellation scores 2 out of 6 for being undervalued (see the score). Next, we will break down what goes into that number and compare different ways of valuing the company. Keep an eye out, because we will wrap up with an even more insightful way to put valuation into context.

Constellation Energy scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Constellation Energy Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates the value of a company by projecting its future cash flows and discounting them back to their value today. This approach aims to capture the present worth of all expected future earnings, offering insight into what the company could truly be worth beyond short-term market swings.

For Constellation Energy, the DCF analysis uses the 2 Stage Free Cash Flow to Equity model. According to the most recent data, the company's latest twelve months' free cash flow was -$657 million, reflecting a current negative cash flow position. Analysts forecast that free cash flow is expected to turn positive and grow significantly in the coming years, with projections reaching $5.67 billion by 2029. Simply Wall St extrapolates further cash flow growth beyond analysts' estimates for a full picture across ten years.

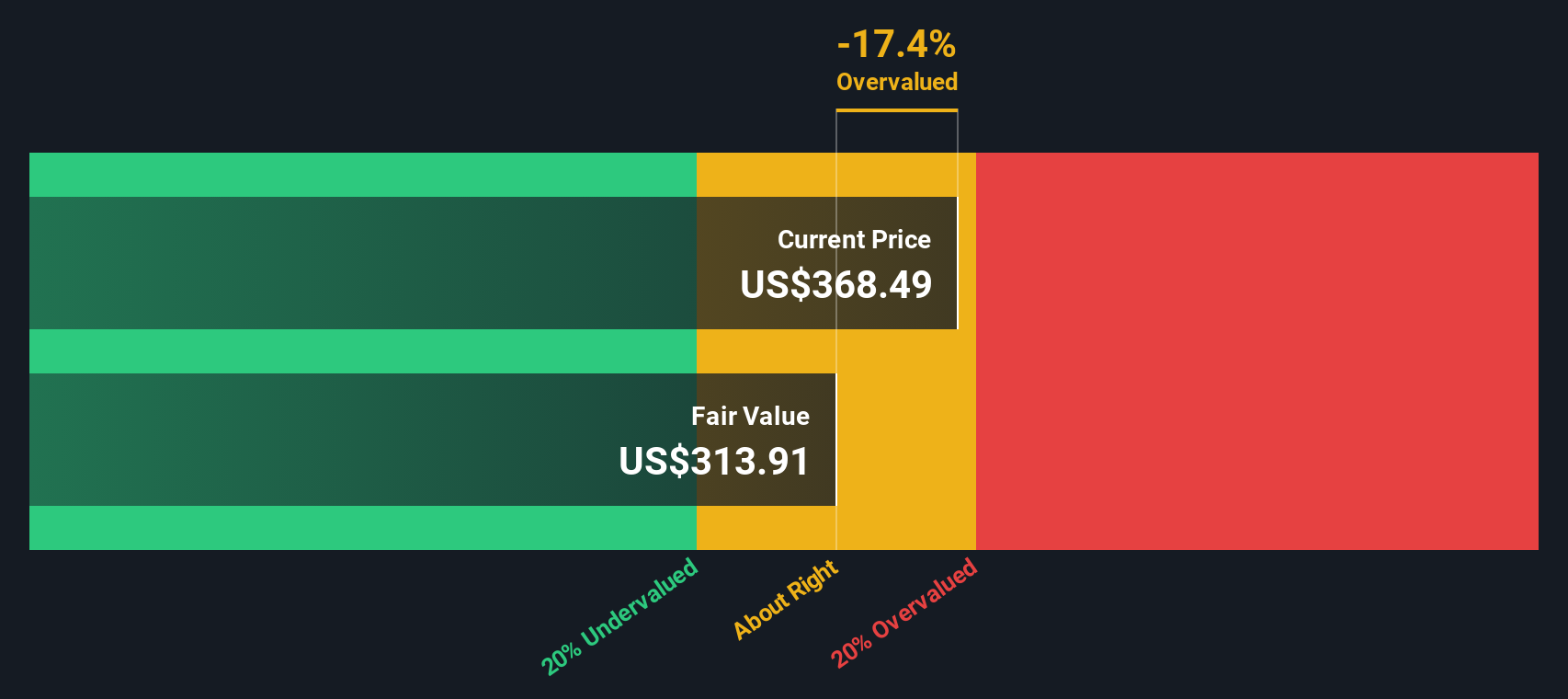

Based on these future cash flow projections and using a discount rate to factor in the time value of money and risk, the intrinsic value of Constellation Energy is determined to be $492.26 per share. This represents a 27.1% discount to the current market price, suggesting the stock is substantially undervalued using this valuation method.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Constellation Energy is undervalued by 27.1%. Track this in your watchlist or portfolio, or discover 926 more undervalued stocks based on cash flows.

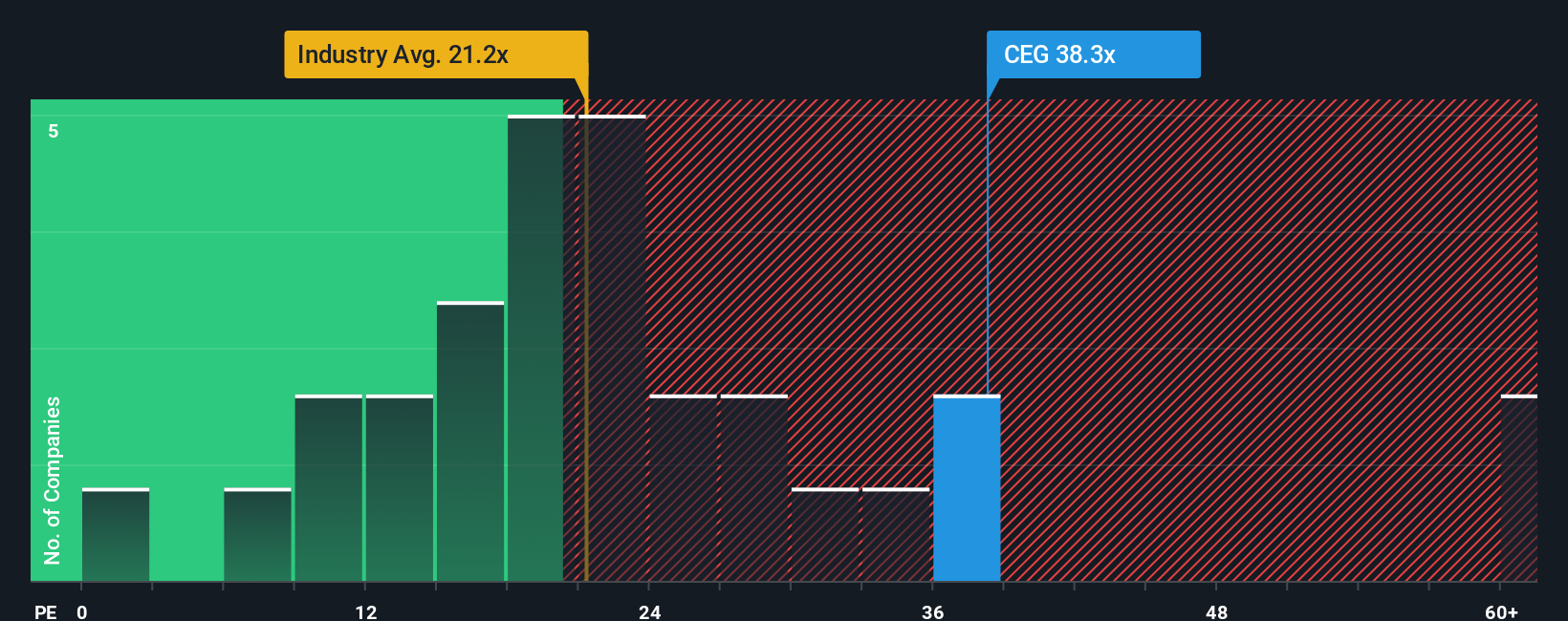

Approach 2: Constellation Energy Price vs Earnings

For profitable companies like Constellation Energy, the Price-to-Earnings (PE) ratio is one of the most widely used metrics to evaluate how the market is valuing future earnings power. Investors often prefer the PE ratio because it provides a quick snapshot of how much they are paying for each dollar of company profit, making it especially relevant for businesses generating consistent earnings.

It is important to note that what counts as a “fair” PE ratio can vary depending on factors like expected earnings growth and the level of risk facing the business. Companies with higher anticipated growth and lower risks typically justify a higher PE multiple, while those with more uncertainty or slower growth tend to trade at lower PEs.

Currently, Constellation Energy trades at a 40.94x PE ratio. This is much higher than the Electric Utilities industry average of 20.90x and above the peer group average of 21.77x. At first glance, this premium might seem excessive. However, Simply Wall St calculates a unique “Fair Ratio” for the company, factoring in elements like expected earnings growth, profit margins, market capitalization, and business risk. For Constellation Energy, the Fair PE Ratio stands at 39.76x.

The Fair Ratio goes deeper than basic peer or industry comparisons by tailoring the benchmark to Constellation’s specific profile. This means it accounts for why some companies deserve a higher or lower multiple than the crowd. In this case, with the actual PE ratio at 40.94x and the Fair Ratio at 39.76x, the difference is small, suggesting the market’s pricing of Constellation Energy is very close to expectations given its outlook and risk profile.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1439 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Constellation Energy Narrative

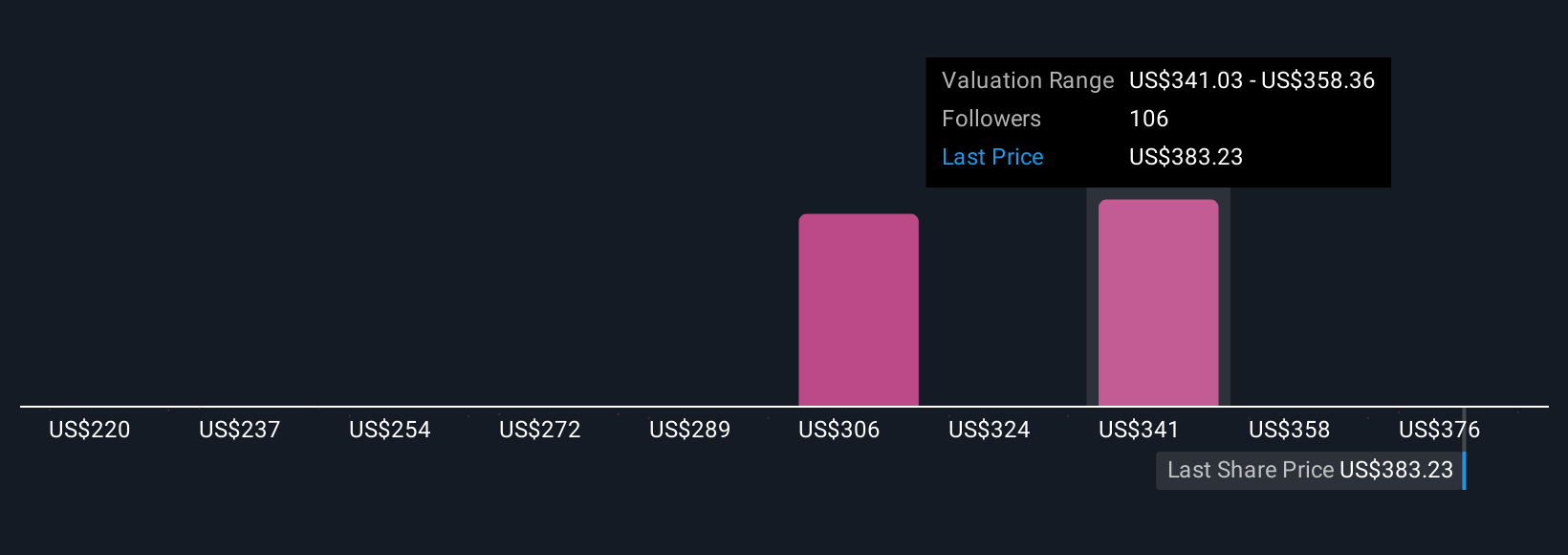

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives. A Narrative is your personal story about a company, combining your view of its business, future revenue, earnings, and margins into a single, shareable perspective that connects the numbers to real-world context. Narratives link what is happening in Constellation Energy’s business today, such as its power deals, nuclear investments, or the risks tied to data center clients, with your forecast and an estimate of fair value. This helps you see how your view compares to the current stock price.

On Simply Wall St, millions of investors can easily create and update Narratives within the Community page. This tool shows whether your fair value is above or below the current price and lets you adjust your assumptions as soon as news or earnings are released, keeping your decision-making agile and informed. For example, some investors expect Constellation’s earnings to reach as high as $5.1 billion with a fair value of $393, seeing potential if AI power demand keeps rising. Others forecast $1.5 billion in earnings with a fair value of $184, factoring in regulatory and execution risks.

Do you think there's more to the story for Constellation Energy? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CEG

Constellation Energy

Produces and sells energy products and services in the United States.

Adequate balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$120.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k1.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative