Advertisement

- United States

- /

- Transportation

- /

- NYSE:UBER

Assessing Uber’s True Value After 35.6% Share Price Surge in 2025

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Uber Technologies is still a smart buy after its big run-up? You are not alone, and the question of real value is front of mind for many investors right now.

- Uber's stock has delivered an impressive 35.6% gain year to date, despite seeing a dip of 10.5% over the last month, signaling both growth momentum and changing risk appetites in the market.

- Recent headlines have cast a spotlight on Uber's pivotal role in the evolving transportation landscape and ongoing legal and regulatory debates, fueling both investor optimism and caution. News about partnerships with automakers and expansion into new delivery segments have added to the story, influencing price moves and perceptions of future value.

- According to our valuation checks, Uber scores a solid 6 out of 6, which is a strong indicator that the company is currently undervalued across all measures we track. Up next, we will break down the different ways to value Uber, but stick around for a perspective on valuation that could change how you view the stock altogether.

Approach 1: Uber Technologies Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its expected future cash flows and discounting them back to today, reflecting the time value of money. For Uber Technologies, this approach provides an in-depth look at how much future business activity is worth right now in dollars.

Currently, Uber generates an impressive Free Cash Flow of approximately $8.66 billion. Analyst forecasts project consistent cash flow growth in the coming years. Free Cash Flow is expected to reach about $16.51 billion by the end of 2029. While analysts supply projections up to five years out, recent estimates have been extrapolated to provide a longer-term outlook. This illustrates strong anticipated expansion in Uber’s operations and profitability.

Based on the 2 Stage Free Cash Flow to Equity model, Uber’s estimated intrinsic value stands at $168.03 per share. This suggests the current share price is trading at a 49.0% discount to the company’s fair value. According to this methodology, the stock appears significantly undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Uber Technologies is undervalued by 49.0%. Track this in your watchlist or portfolio, or discover 922 more undervalued stocks based on cash flows.

Approach 2: Uber Technologies Price vs Earnings

The Price-to-Earnings (PE) ratio is a widely used valuation metric for profitable companies, as it directly relates a company’s share price to its earnings. For businesses like Uber Technologies that have reached profitability, the PE ratio helps investors assess whether the stock is priced attractively relative to the company’s ability to generate profits.

A "normal" or "fair" PE ratio depends on several factors, including the company’s expected earnings growth, perceived business risks, profit margins, and prevailing market sentiment. Companies with strong growth prospects generally command higher PE multiples, while added risks or lower growth can lead to a lower fair value.

Currently, Uber trades on a PE ratio of 10.70x. This is markedly lower than the Transportation industry average of 26.68x, and it also compares favorably to the average for Uber’s peers, which stands at a much higher 68.26x. On the surface, this might suggest Uber is undervalued.

However, the "Fair Ratio" calculated by Simply Wall St is 13.42x. The Fair Ratio is a proprietary metric that factors in Uber’s specific growth potential, risk profile, profit margins, size, and its position within the industry. This offers a more nuanced benchmark than peer or industry averages alone.

Comparing Uber’s actual PE ratio of 10.70x to its Fair Ratio of 13.42x indicates that the stock is undervalued by this key measure, with more than a 0.10 difference.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1440 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Uber Technologies Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative puts a story behind a stock: your view about where Uber Technologies is headed, what its future could look like, and why the market may be wrong about its true worth. Narratives link these stories to explicit forecasts and a resulting fair value, making investing a more personal and strategic process.

With Narratives, you are not just crunching numbers; you are connecting Uber's real-world potential, such as new revenue streams, legal challenges, or game-changing technology, to dynamic models that recalculate fair value as news or data changes. Available to millions of investors through the Simply Wall St Community page, Narratives are straightforward to use. You set your assumptions and see how your scenario compares to others’. This helps you decide whether to buy or sell by showing if the price currently on offer is above or below your estimate of fair value.

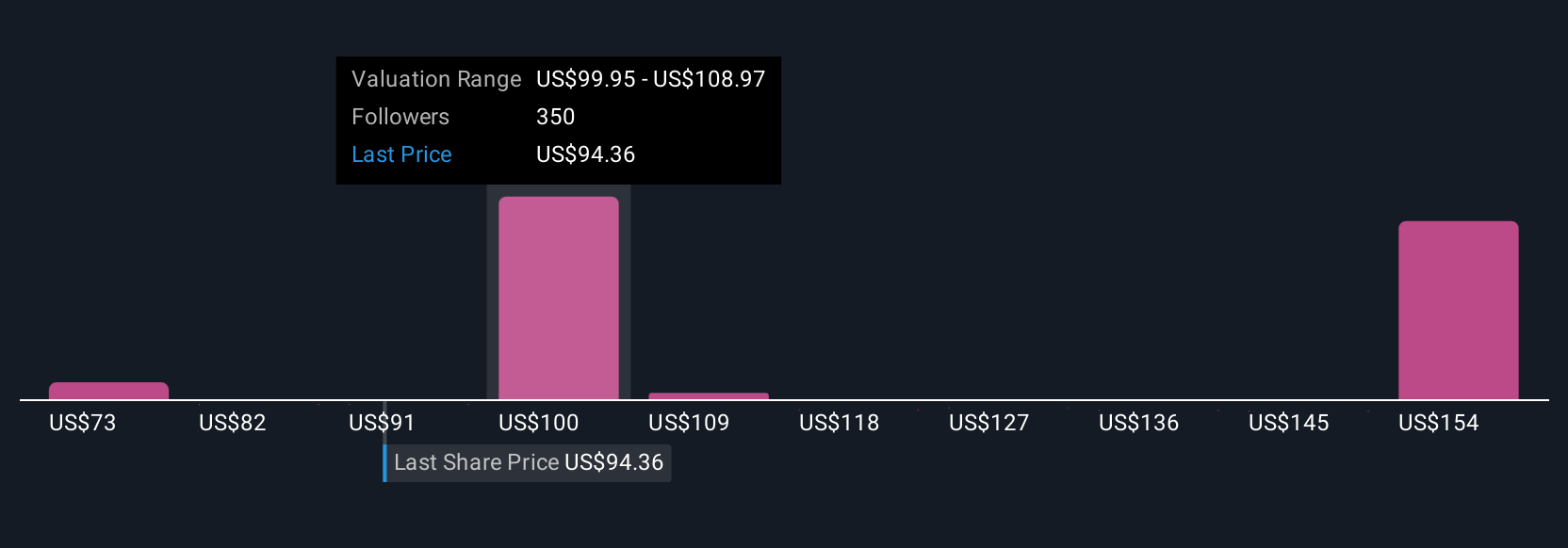

Narratives also update instantly when major events or earnings are reported, giving you a living forecast. For example, some investors see Uber’s fair value at $75 per share based on slower growth and margin risk, while others believe it could be worth over $110 if platform integration and autonomous vehicle bets pay off quickly.

For Uber Technologies, we'll make it really easy for you with previews of two leading Uber Technologies Narratives:

- 🐂 Uber Technologies Bull Case

Fair Value: $110.55

Current Price vs Fair Value: 22.5% undervalued

Revenue Growth Forecast: 14.5%

- Analysts expect expanding Uber platform engagement and product diversification to drive robust revenue growth and retention, supported by cross-platform integration and targeted promotions.

- Strategic investments in autonomous vehicles, electrification, and ancillary services are seen as enhancing long-term profitability and creating lasting competitive advantages.

- Risks include capital intensity from autonomous vehicle development, increasing regulatory pressures, and margin compression from growth in lower margin segments. Overall, analysts believe Uber’s fair value is above the current share price.

- 🐻 Uber Technologies Bear Case

Fair Value: $75.00

Current Price vs Fair Value: 14.2% overvalued

Revenue Growth Forecast: 4.2%

- Despite strong revenue growth and recent profitability, Uber’s current market capitalization is significantly above its estimated fair value based on conservative 2030 projections for earnings and EBITDA.

- Even factoring in expected improvements from autonomous vehicle technology, the narrative sees the stock as overvalued, with a more attractive entry point estimated at $65 to $75 per share.

- Key concerns include slower projected revenue growth going forward, a higher valuation relative to sustainable long-term earnings, and potential risks around scalability and margin pressure.

Do you think there's more to the story for Uber Technologies? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:UBER

Uber Technologies

Develops and operates proprietary technology applications in the United States, Canada, Latin America, Europe, the Middle East, Africa, and the Asia Pacific.

Very undervalued with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative