Advertisement

- United States

- /

- Airlines

- /

- NYSE:LUV

Is Southwest Airlines Stock Still Worth a Look After 13% Jump on Travel Demand News?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Southwest Airlines is a hidden bargain or if the stock price is flying a bit too high? Here is what you should know before making your next move.

- The stock has been on the move lately, up 6.1% in the past week and gaining 13.5% over the last month. These changes have caught the attention of investors looking for growth or shifts in market sentiment.

- These recent jumps follow news of changes in the airline industry landscape, including renewed travel demand and updates on operational improvements at Southwest. Investors are also watching closely as airlines adapt to evolving regulations and fluctuations in fuel prices, all of which add important context to the recent price swings.

- Despite the strong recent momentum, Southwest Airlines currently scores a 0 out of 6 on our undervalued checklist. Next, we will explore the classic valuation methods. For those who want an even sharper edge, a smarter way to understand the numbers will be covered by the end of this article.

Southwest Airlines scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Southwest Airlines Dividend Discount Model (DDM) Analysis

The Dividend Discount Model (DDM) estimates a stock's intrinsic value by projecting future dividend payments and discounting them back to today's dollars. This approach is especially suited for companies that pay regular dividends, focusing on both the sustainability and expected growth of those dividends.

According to the latest data, Southwest Airlines currently pays an annual dividend per share of $0.78. The payout ratio, which measures how much of the company’s earnings are paid out as dividends, is extremely high at 92.04%. This leaves very little room for future growth. This view is reinforced by their projected annual dividend growth rate of just 0.35%, calculated by multiplying the retained earnings portion of profits (just 7.96% is retained) by the return on equity (4.46%).

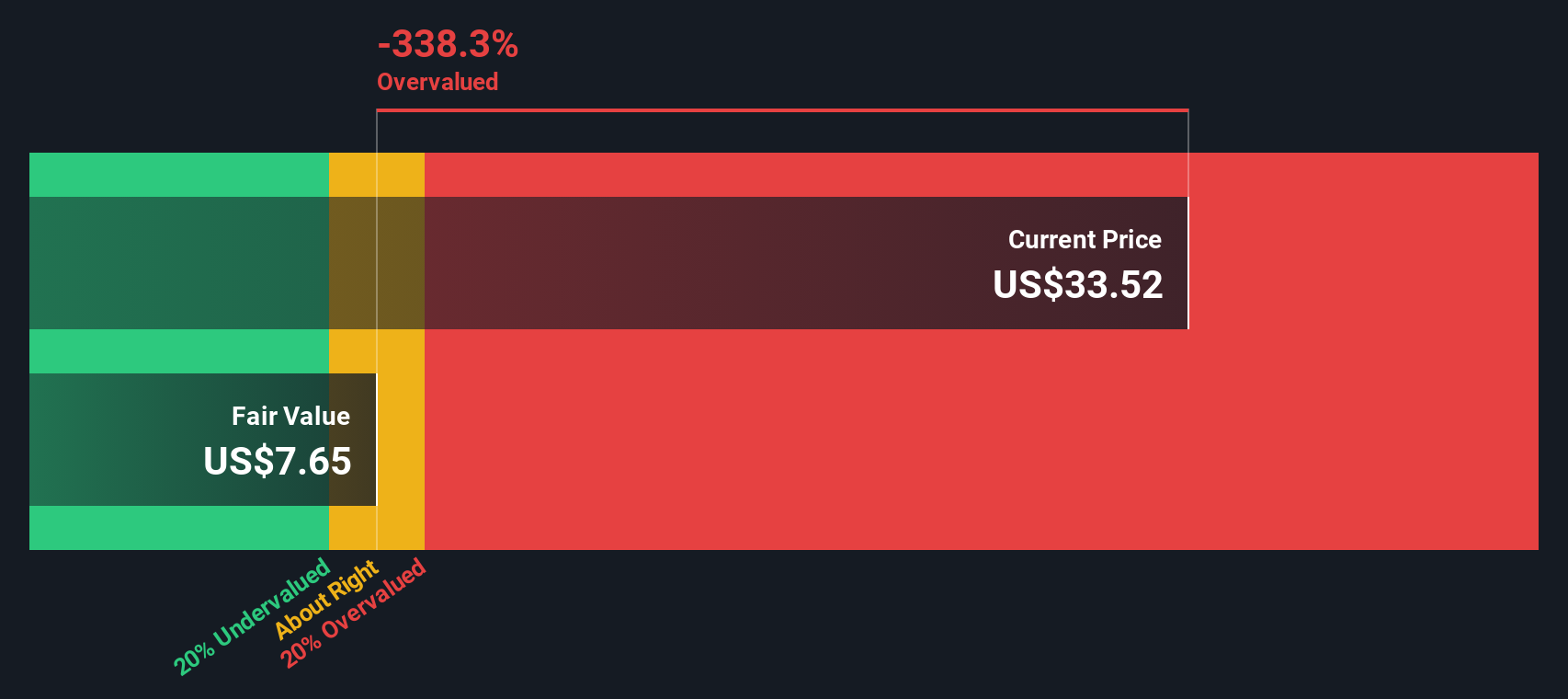

Based on these projections, the DDM model places the estimated fair value of Southwest Airlines stock at $8.11 per share, which is significantly below the current market price. This suggests the stock is roughly 329.3% overvalued using this method. Dividend growth is modest, and high payout ratios signal limited upside for valuation from dividends alone.

Result: OVERVALUED

Our Dividend Discount Model (DDM) analysis suggests Southwest Airlines may be overvalued by 329.3%. Discover 920 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Southwest Airlines Price vs Earnings

The Price-to-Earnings (PE) ratio is a popular valuation measure for profitable companies like Southwest Airlines. It helps investors assess how much the market is willing to pay for each dollar of earnings. PE ratios are especially useful in this context because they capture both current profitability and market expectations for future growth. Typically, firms with stronger earnings growth or lower perceived risk command higher PE ratios. Riskier or slower-growing companies tend to trade at lower multiples.

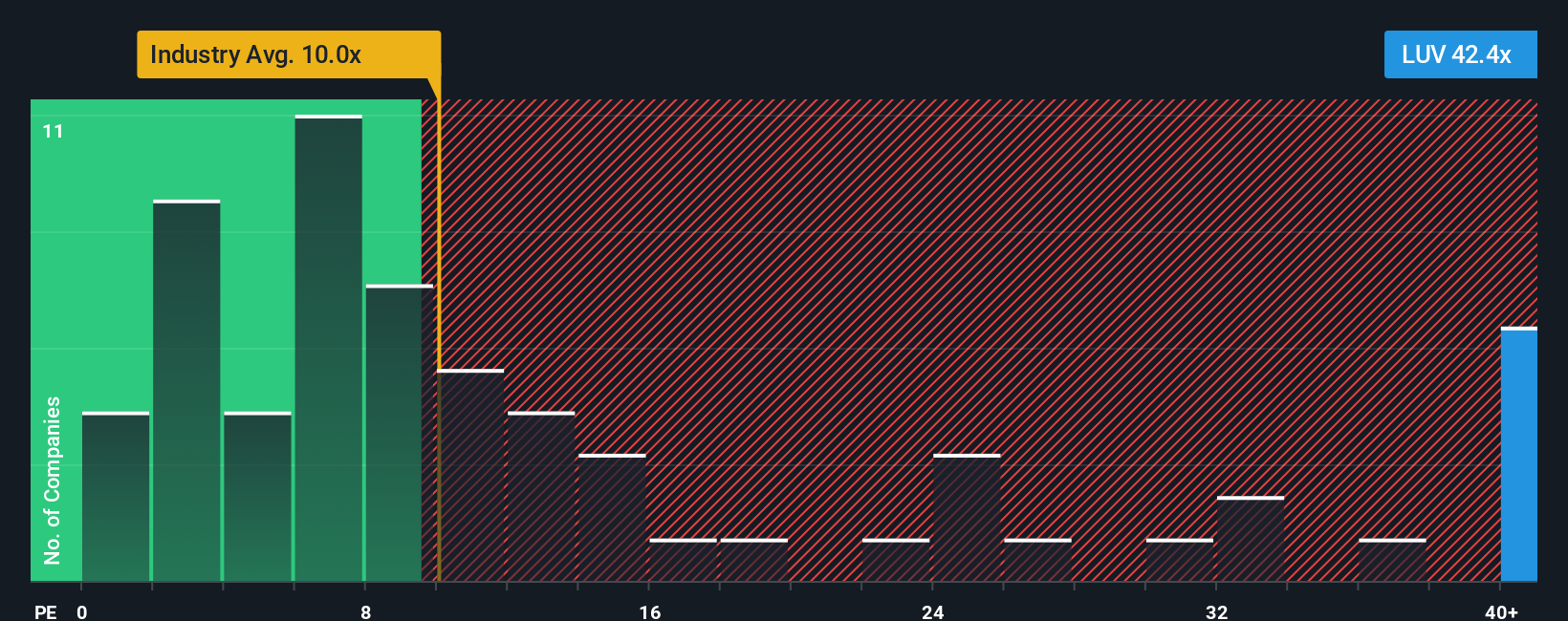

Currently, Southwest Airlines trades at a PE ratio of 47.5x. This stands out when compared with the airline industry average of 9.1x and its peer group average of 10.5x. This may suggest the market is assigning a premium to Southwest’s shares, possibly reflecting specific expectations or optimism about its performance relative to its competitors.

The analysis goes a step further with Simply Wall St's proprietary “Fair Ratio.” This fair PE ratio for Southwest Airlines is calculated at 28.2x and integrates not just peer and industry comparisons, but also factors in company-specific drivers. These include its earnings growth prospects, profit margins, risk profile, and market capitalization. By accounting for these elements, the Fair Ratio provides a more nuanced and potentially accurate benchmark than a simple industry average.

Comparing the Fair Ratio of 28.2x with Southwest’s current 47.5x PE, the stock appears significantly overvalued on this basis because the gap suggests a price well above its expected fair value.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Southwest Airlines Narrative

Earlier, we mentioned there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is a simple, powerful framework that lets you connect the story you believe about Southwest Airlines, such as expected revenue growth, margin expansion, or competitive challenges, to your own estimates and fair value calculation.

With Narratives, you go beyond traditional metrics. You create your investment thesis by forecasting future revenues, earnings, and margins based on the real-world trends and company actions you think matter most. Narratives are available right now to everyone on Simply Wall St’s Community page, and are used by millions of investors to put the numbers in context.

This approach helps you decide when to buy or sell by transparently comparing your Fair Value to the current share price. The best part is, Narratives update dynamically. As news breaks, earnings are announced, or industry conditions change, your story and fair value can evolve in real time.

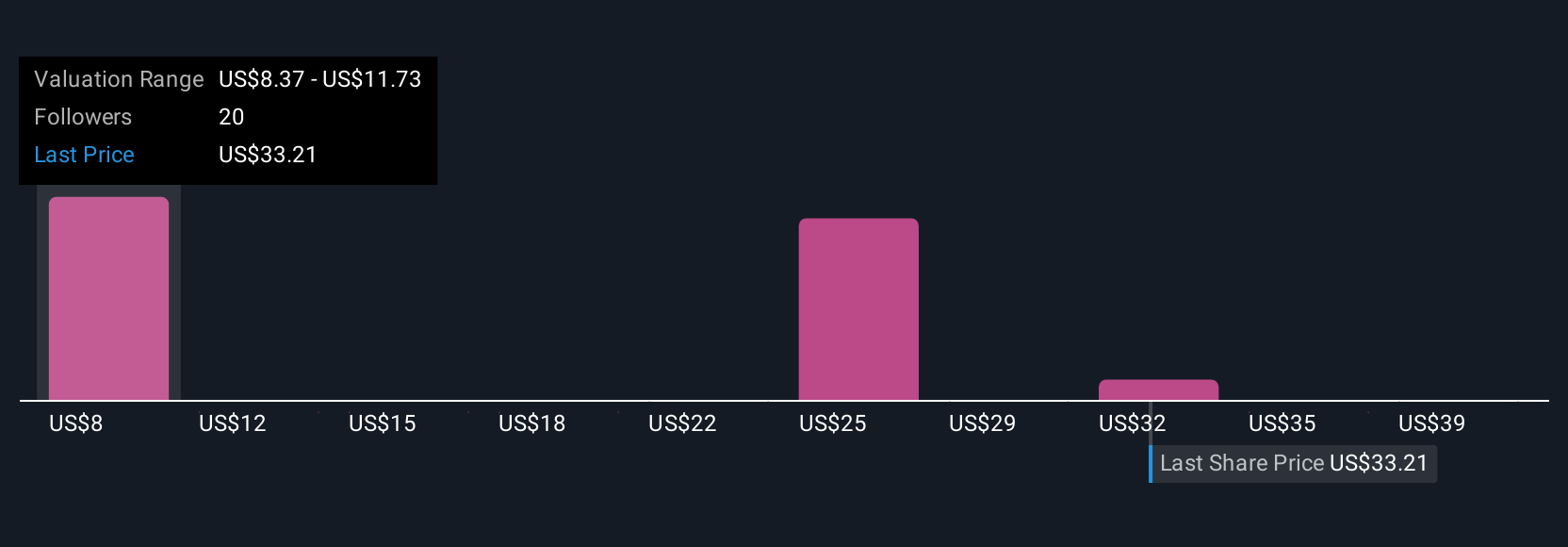

For example, some investors believe Southwest could be fairly valued as high as $46, assuming rapid revenue growth and recovery, while others see just $19 as more appropriate given lingering risks. The best perspective is the one informed by your own Narrative.

Do you think there's more to the story for Southwest Airlines? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:LUV

Southwest Airlines

Operates as a passenger airline company that provides scheduled air transportation services in the United States and near-international markets.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative