Advertisement

- United States

- /

- Marine and Shipping

- /

- NYSE:KEX

Is Kirby’s Recent Fleet Expansion a Reason to Revisit Its Share Price in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

- If you have ever wondered whether Kirby stock is attractively priced or trading at a premium, you are not alone. Many investors are taking a fresh look after recent market moves.

- Kirby’s share price has climbed 5.0% in the last week and a robust 12.0% over the past month, rebounding from a 1-year decline of 10.6% and reminding us of its long-term potential with a 102.7% gain over five years.

- Investor attention has recently sharpened due to strategic announcements from Kirby, including notable expansions in their fleet and new partnerships within the marine transportation industry. These developments have helped fuel the latest momentum in the stock.

- Currently, Kirby scores 0 out of 6 for undervaluation checks. Next, let’s break down those approaches and see why relying on standard metrics might not tell the full story of Kirby’s value.

Kirby scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Kirby Discounted Cash Flow (DCF) Analysis

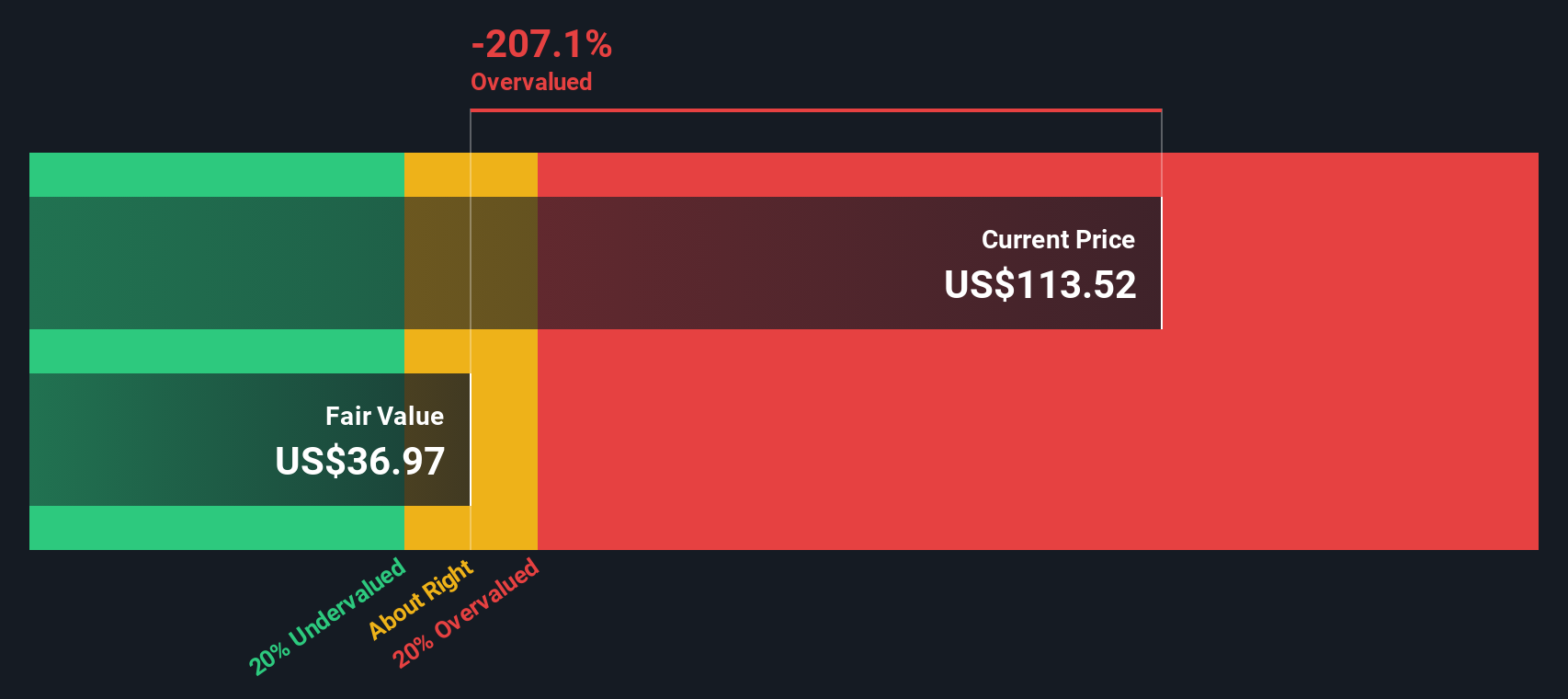

The Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by projecting its future cash flows and then discounting them back to today’s dollars. For Kirby, this approach starts with the company’s latest twelve-month free cash flow (FCF), which is $218.5 million. Analysts forecast FCF to grow, reaching $337.2 million by December 2024. Over the next decade, extrapolated projections suggest a gradual decline, with FCF expected to be around $102.1 million in 2035 after peaking in the near term.

These cash flow estimates are derived from a two-stage model. The model reflects higher growth in the short term, followed by a more moderate trajectory as the business matures. It is important to note that cash flow projections for later years rely on assumptions and are less certain than near-term estimates.

Based on this analysis, Kirby’s calculated intrinsic value is $36.84 per share. Compared to the current market price, this implies a 206.9% premium, which indicates the stock is substantially overvalued according to the DCF model.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Kirby may be overvalued by 206.9%. Discover 920 undervalued stocks or create your own screener to find better value opportunities.

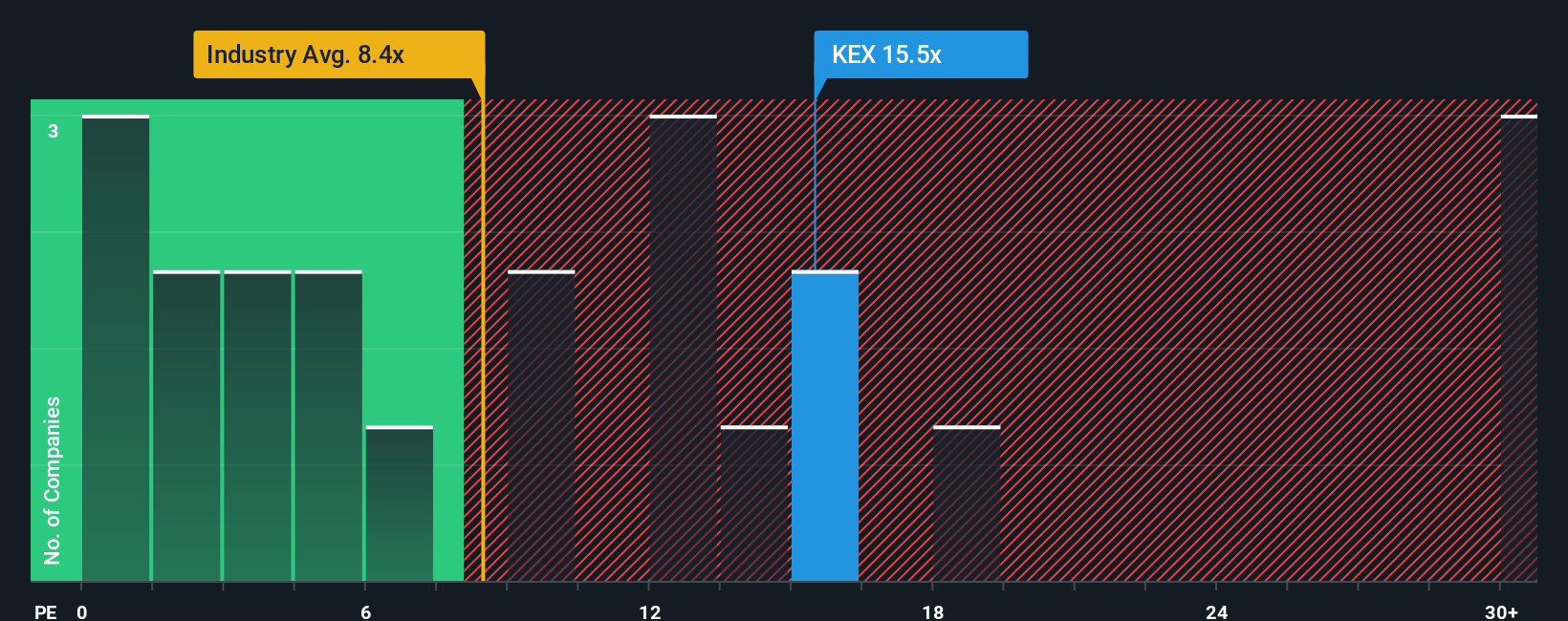

Approach 2: Kirby Price vs Earnings

The Price-to-Earnings (PE) ratio is commonly used for evaluating profitable companies, as it measures how much investors are willing to pay for each dollar of earnings. This makes it a good starting point for considering Kirby’s valuation because the company generates consistent profits.

Typically, a "normal" or "fair" PE ratio is shaped by expectations for future growth and the perceived risks facing the company. Rapidly growing or lower-risk businesses tend to command higher PE multiples, while slower-growing or riskier companies may trade at lower ones.

Kirby currently trades at a PE ratio of 20.1x. This stands noticeably above the shipping industry average of 9.7x and also higher than the average of its closest peers, which is 13.6x. On the surface, this suggests Kirby might be trading at a premium to its sector and peers.

Simply Wall St's “Fair Ratio” is particularly useful here. Unlike a basic industry or peer comparison, it is calculated by taking into account Kirby’s unique profile, factoring in its earnings growth outlook, profit margins, market capitalization, industry placement, and various company-specific risks. This provides a more holistic view of what the company’s multiple should be under current conditions.

Kirby’s Fair Ratio is estimated at 13.1x, which is notably lower than the current PE of 20.1x. Since this gap is more than 0.10, it points to Kirby’s shares being overvalued relative to its underlying fundamentals on an earnings basis.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Kirby Narrative

Earlier, we mentioned there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is a powerful, user-friendly tool that lets you tell the story behind a company’s numbers, combining your unique take on Kirby’s future with your assumptions about its revenue, earnings, and margins to arrive at your own fair value.

Instead of relying solely on static valuation ratios, Narratives connect a company’s bigger picture—everything from industry shifts to management decisions—directly to the financial forecasts that drive share price. This makes them an accessible way for investors of any skill level to bridge the gap between what’s happening in the real world and what those changes mean for Kirby’s value.

Available on Simply Wall St’s Community page, Narratives help millions of investors decide whether to buy or sell by comparing fair value (based on their stories and forecasts) to the current share price. What’s more, Narratives update automatically as new information, like earnings results or breaking news, is released, keeping your analysis relevant in real time.

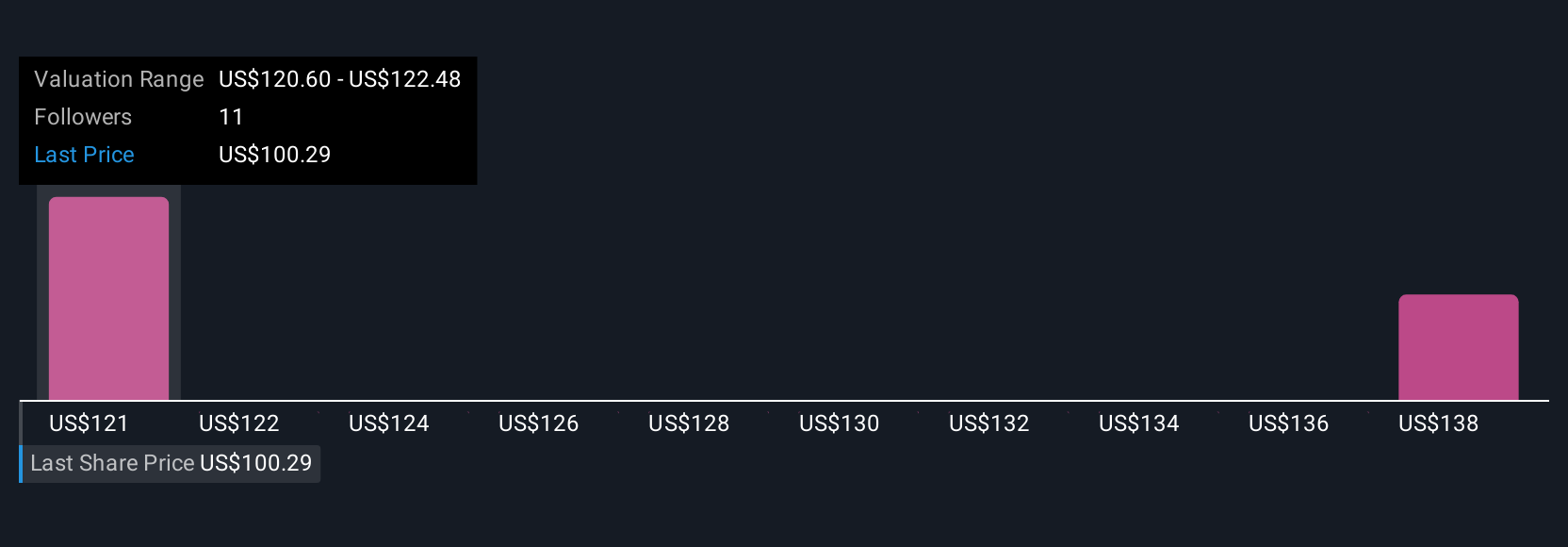

For example, some investors expect Kirby could be worth as much as $128 per share thanks to strong data center demand and shipping fleet upgrades. Others see a fair value of $102, reflecting concerns around petrochemical weakness and cost pressures. Both views are easily explored and tracked using Narratives.

Do you think there's more to the story for Kirby? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kirby might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:KEX

Excellent balance sheet with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

102 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative