Advertisement

- United States

- /

- Marine and Shipping

- /

- NYSE:KEX

Could Softer Barge Demand Quietly Redefine Kirby’s Capacity Advantage And Risk Profile (KEX)?

Simply Wall St

Reviewed by Sasha Jovanovic

- Recently, investors highlighted that Kirby Corporation’s inland marine transportation business has come under pressure as softened barge utilization and weaker demand from energy, chemical, and industrial customers weigh on volumes and pricing.

- An interesting takeaway is that, despite these cyclical headwinds and lower earnings expectations, some institutional investors still view Kirby’s constrained industry capacity as a longer-term advantage.

- We’ll now examine how softer inland barge utilization and demand may reshape Kirby’s broader investment narrative and long-term risk-return profile.

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

Kirby Investment Narrative Recap

To own Kirby today, you really have to believe that constrained barge capacity and the shift toward waterborne petrochemical transport will matter more than near term softness in volumes and pricing. The latest pullback in inland barge utilization directly affects Kirby’s key near term catalyst of tight industry supply supporting rates, and it also amplifies the most immediate risk that weaker demand from large chemical and energy customers could drag on earnings.

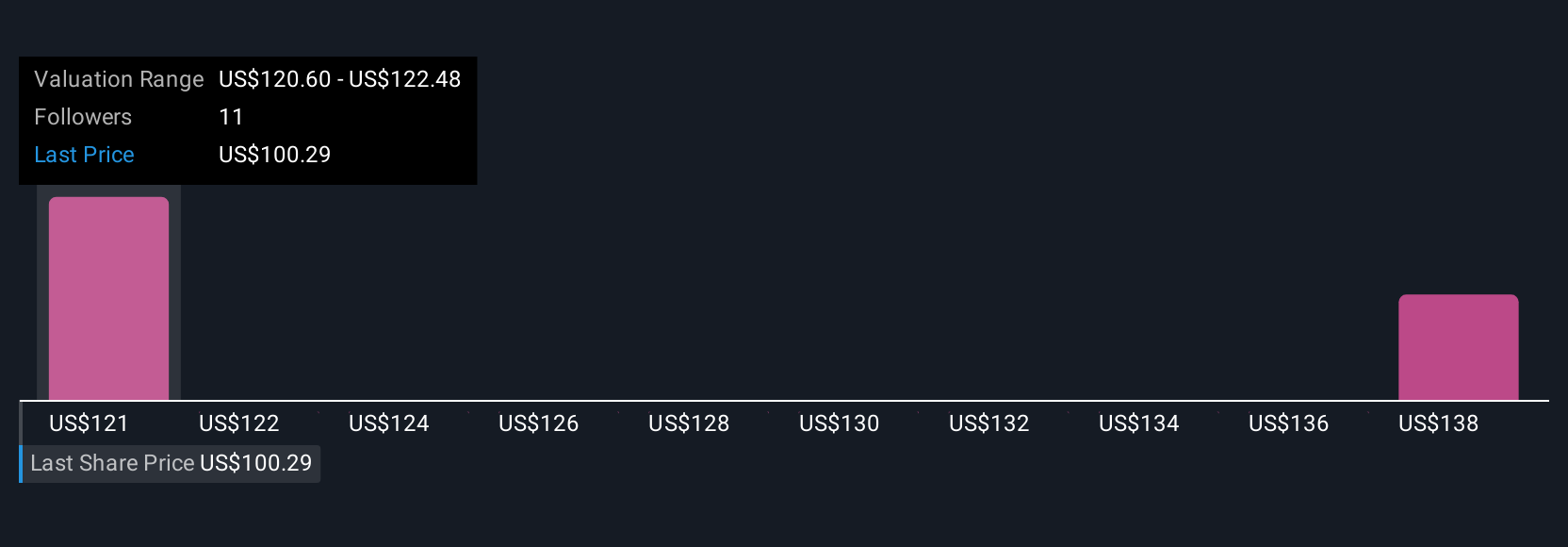

Against this backdrop, Kirby’s ongoing share repurchase program stands out, with US$753.05 million deployed since 2010 and roughly 15.9% of shares bought back by November 2025. While this capital return has not offset recent stock underperformance, it does interact with the same supply constraint story investors are focused on, as tighter vessel capacity and a smaller share count could both influence how much upside or downside the earnings cycle ultimately delivers.

However, investors also need to be aware that Kirby’s heavy reliance on the US inland petrochemical market leaves it particularly exposed if...

Read the full narrative on Kirby (it's free!)

Kirby's narrative projects $3.9 billion revenue and $445.6 million earnings by 2028. This requires 6.1% yearly revenue growth and about a $142.6 million earnings increase from $303.0 million today.

Uncover how Kirby's forecasts yield a $125.33 fair value, a 11% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community fair value estimates for Kirby span from US$36.91 to US$125.33 across 2 independent views, underscoring how far apart individual assessments can be. When you weigh this spread against the risk that softer chemical and energy demand could keep barge utilization and pricing under pressure, it becomes even more important to compare several perspectives before deciding how Kirby fits into your portfolio.

Explore 2 other fair value estimates on Kirby - why the stock might be worth less than half the current price!

Build Your Own Kirby Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Kirby research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

- Our free Kirby research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Kirby's overall financial health at a glance.

Curious About Other Options?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Rare earth metals are the new gold rush. Find out which 36 stocks are leading the charge.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kirby might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:KEX

Excellent balance sheet with questionable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

57 followersusers have followed this narrative

6 commentsusers have commented on this narrative

17 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15081.9% undervalued

50 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4727.3% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

117 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

958 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

57 followersusers have followed this narrative

6 commentsusers have commented on this narrative

17 likesusers have liked this narrative