Advertisement

- United States

- /

- Airlines

- /

- NYSE:DAL

Delta Air Lines (DAL): Exploring Valuation After Leadership Signals Strong Recovery and Holiday Travel Optimism

Simply Wall St

Reviewed by Simply Wall St

Delta Air Lines (DAL) is in the spotlight after recent updates from company leadership, which highlighted a sharp recovery following the government shutdown. The updates also pointed to upbeat holiday travel expectations and ongoing gains in operational fundamentals and customer service technology.

See our latest analysis for Delta Air Lines.

Momentum around Delta’s share price has picked up recently, with a 9.7% gain over the last week and a 3.4% increase just in the past day as investors respond to forecasts of strong holiday travel and positive leadership commentary. While the 1-year total shareholder return sits at a modest 1.9%, the company’s robust three-year total shareholder return of 85% indicates investors continue to price in meaningful upside given Delta’s operational recovery and long-term growth initiatives.

If Delta’s recent move has you wondering what else could be poised for growth, now is the perfect time to explore See the full list for free.

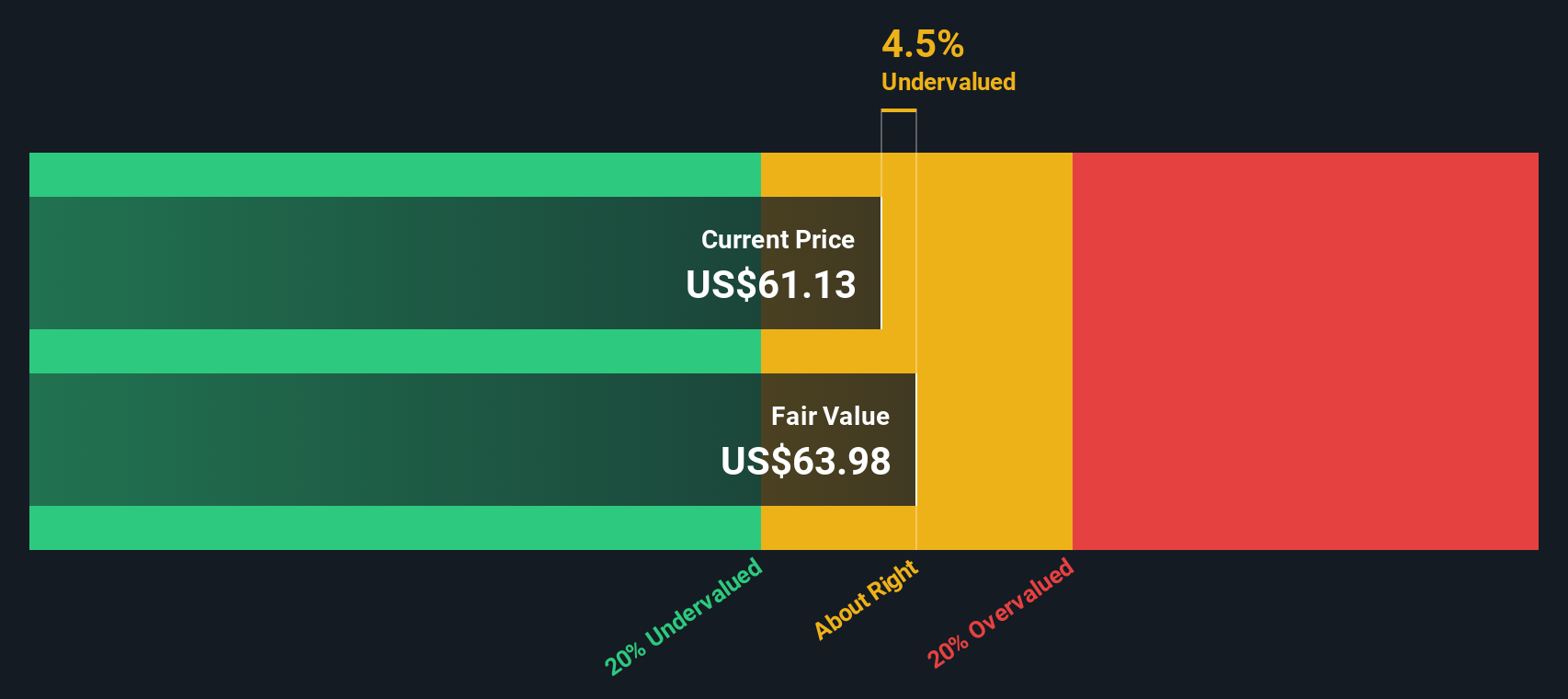

With shares now pricing in a rapid recovery and ambitious growth goals, the real question is whether Delta is still trading at a discount, or if the market has already factored in all of its future potential for investors.

Most Popular Narrative: 7.4% Overvalued

According to PittTheYounger, the narrative's fair value estimate comes in lower than Delta’s last close price, raising questions about whether shares have gotten ahead of themselves. The author's detailed breakdown contrasts robust recent performance with revised forward expectations that underpin a more muted long-term outlook.

Yet with its early warning about waning travel demand in March, my original assumptions in February regarding revenue growth and future PE had to be revised downwards from 4 to 2 per cent per year and 12, respectively. This resulted in a fair value of about $53.50 a share. After DAL's quarterly numbers as of 9 April and the related poor visibility for the remainder of the year, I have to lower my anticipated PE further to 11, leading to a new fair value of about 49 dollars a share. This still leaves some upside.

Which data points force this outlook shift? PittTheYounger's narrative hints at the crosscurrents behind a sharply lower profit multiple and reduced growth runway. Hungry for the exact moves that recalibrate Delta’s perceived future value? The full narrative holds the numbers and logic that drive this eye-opening fair value.

Result: Fair Value of $49 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, sudden economic shocks or renewed trade tensions could swiftly undermine Delta's recovery. This reminds investors that the airline industry’s outlook can change quickly.

Find out about the key risks to this Delta Air Lines narrative.

Another View: DCF Says Shares Are Undervalued

Challenging the earlier fair value, our DCF model estimates Delta’s shares are currently trading at a sharp 40.9% discount to fair value. This suggests significant upside is possible if the company’s cash flows remain robust. But do these assumptions hold up under changing industry winds?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Delta Air Lines Narrative

If you see the numbers differently or want to develop your own perspective, you can analyze the fundamentals and craft your narrative in just a few minutes. Do it your way

A great starting point for your Delta Air Lines research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Missing these opportunities could mean overlooking your next big winner. Make your next smart move with fresh stock ideas built for today’s market momentum.

- Catch tomorrow’s leaders early and zero in on potential breakout companies with these 3575 penny stocks with strong financials to stay ahead of Wall Street trends.

- Collect steady income and add financial resilience to your portfolio by reviewing these 15 dividend stocks with yields > 3% that offer robust yields and solid stability.

- Harness the future of artificial intelligence by browsing these 25 AI penny stocks. These fast movers are shaping how technology transforms the business world.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:DAL

Delta Air Lines

Provides scheduled air transportation for passengers and cargo in the United States and internationally.

Undervalued with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$120.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k1.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative