Advertisement

- United States

- /

- Airlines

- /

- NasdaqGS:UAL

Is There Still an Opportunity in United Airlines After Recent Route Expansion News?

Simply Wall St

Reviewed by Bailey Pemberton

- Ever wondered if United Airlines Holdings is trading at a bargain or simply soaring too high? Whether you are an optimist or a skeptic, understanding what the stock is truly worth could help you land a smarter investment decision.

- The stock has climbed 10.6% over the last week and 6.3% over the past month, adding up to a healthy 6.8% year-to-date return, and an impressive 132.3% over the last three years.

- Fueling these recent gains, the company has been catching headlines for expanding international routes and announcing new sustainability initiatives. These factors have kept both investors and industry watchers tuned in. Shifts in travel demand and United's strategic moves are front and center in these news stories, shaping how the market reacts.

- Our initial valuation check gives United Airlines Holdings a score of 5 out of 6 for being undervalued based on key metrics. We will break down how we arrive at this score using a range of valuation methods, but stick around because there is an even more insightful perspective coming at the end of the article.

Approach 1: United Airlines Holdings Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and then discounting them back to today, reflecting the time value of money. This approach is one of the most commonly used methods for valuing companies with substantial, predictable cash flows.

For United Airlines Holdings, the DCF valuation uses recent and projected free cash flows denominated in $. Currently, United generated $2.61 Billion in free cash flow over the last twelve months. Analyst estimates and forecasts suggest this is set to climb steadily, reaching around $3.39 Billion by 2028. Projections further out to 2035 indicate continued growth. While detailed analyst estimates only cover the next five years, later years have been extrapolated to provide a full ten-year view.

Based on these projections, the DCF model arrives at an intrinsic value of $206.57 per share. With the current share price trading approximately 50.6% below this estimate, the model signals that United Airlines Holdings is significantly undervalued by the market at this time.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests United Airlines Holdings is undervalued by 50.6%. Track this in your watchlist or portfolio, or discover 920 more undervalued stocks based on cash flows.

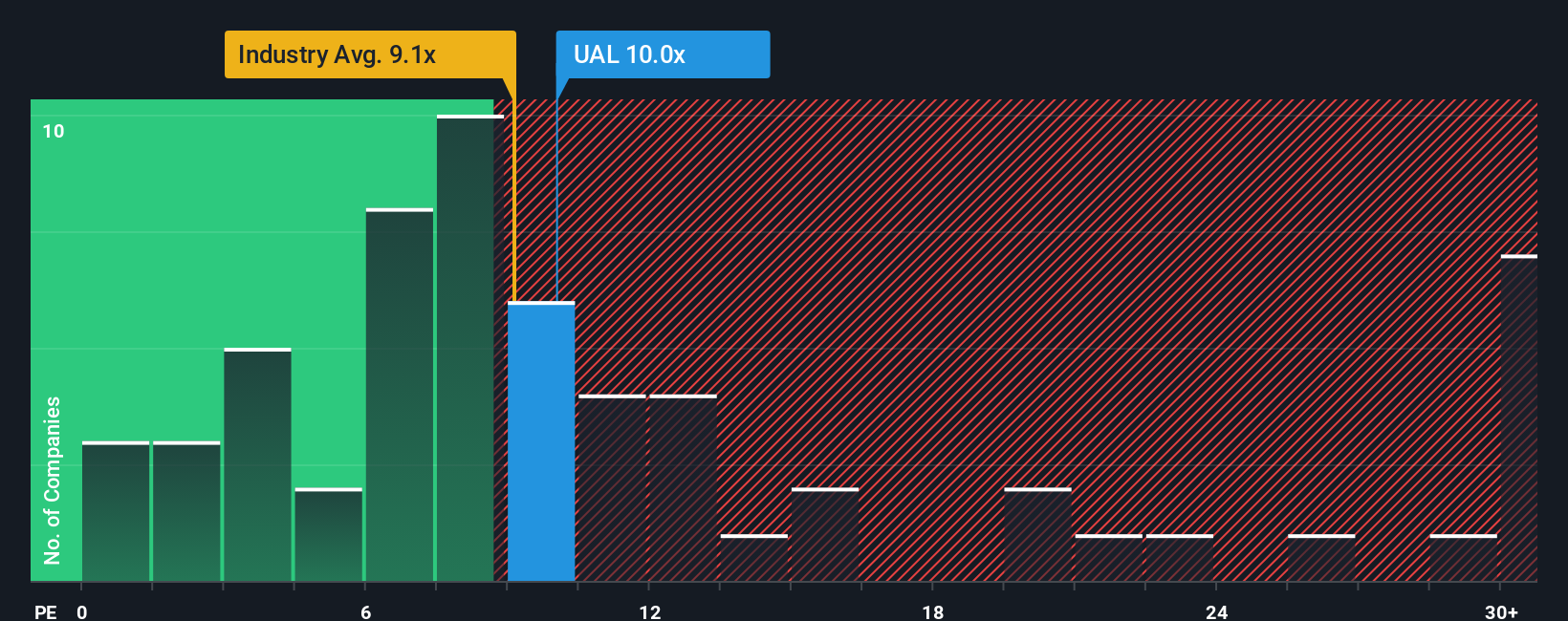

Approach 2: United Airlines Holdings Price vs Earnings (PE)

The Price-to-Earnings (PE) ratio is a widely used valuation metric, particularly for profitable companies like United Airlines Holdings. It shows how much investors are willing to pay today for each dollar of earnings, making it a straightforward way to weigh value, market confidence, and growth prospects.

Assessing a company’s "normal" or "fair" PE ratio depends on several factors. Companies with higher growth expectations or lower risk profiles often justify higher PE ratios, while lower growth or higher risk typically drags the ratio down. Market sentiment, profitability, and industry trends all influence where a reasonable PE should sit.

United Airlines Holdings currently trades at a PE ratio of 10.02x, which is just above the airline industry average of 9.10x and significantly below the peer group average of 19.95x. To provide a more tailored benchmark, Simply Wall St’s proprietary "Fair Ratio" is 14.53x. This Fair Ratio considers not only growth and profitability but also factors like profit margin, industry trends, company size, and specific risk exposures. It offers a more tailored reference point than a blanket industry average.

Comparing the Fair Ratio of 14.53x to United's actual PE of 10.02x suggests that the stock is undervalued, as it is trading well below what would be expected after accounting for its growth profile, profits, and risks.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your United Airlines Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let's introduce you to Narratives. A Narrative is a simple story that captures your unique perspective on a company by connecting business trends and events with your assumptions about its future revenue, earnings, and profit margins. This approach links those beliefs to a specific fair value estimate.

Narratives help you move beyond just the numbers, letting you easily back up your view on United Airlines Holdings with your own forecasts and reasoning. On Simply Wall St’s Community page, used by millions of investors, you can explore dynamic Narratives from others and create your own with just a few clicks, making this tool both user-friendly and insightful.

Narratives are especially powerful because they update automatically as key news stories or earnings reports come out, helping you quickly see how new events may affect your investment thesis. They make it crystal clear when a stock looks attractive to you if your Narrative’s fair value is above the current price, or when it might be time to reconsider.

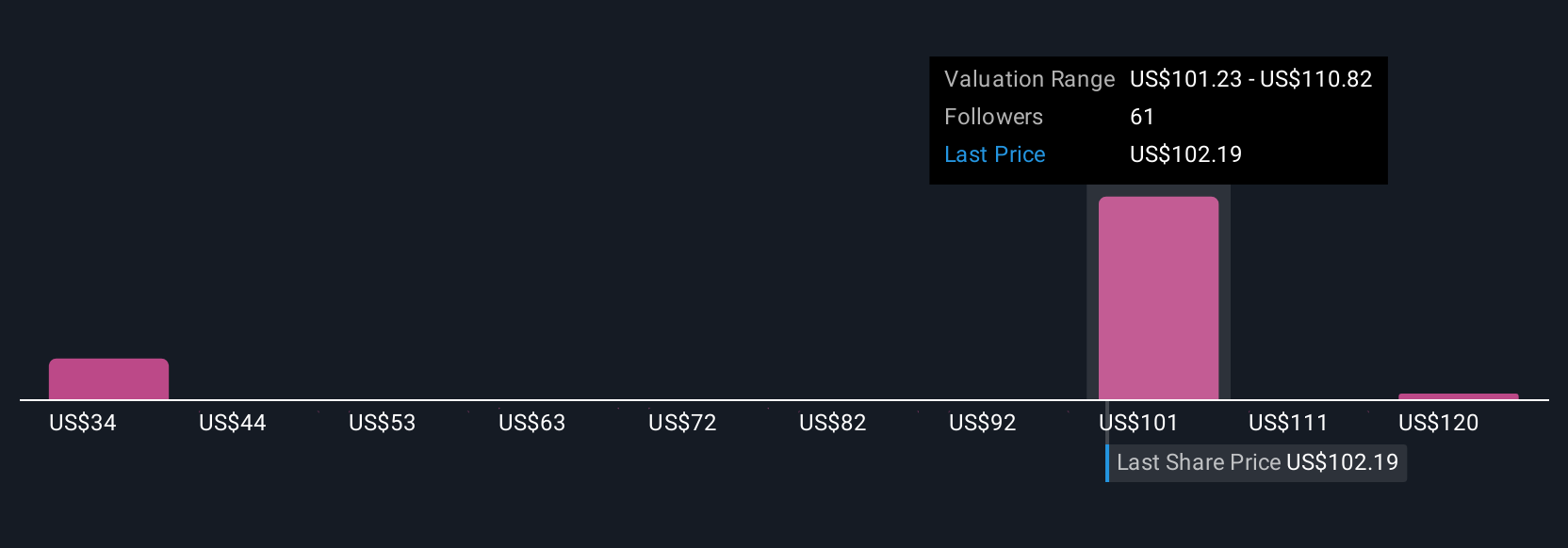

For example, one investor’s Narrative for United Airlines could be extremely optimistic, targeting a fair value of $156 per share based on strong earnings growth and margin expansion. Another may be cautious, seeing risks and valuing the company as low as $43 per share, which demonstrates just how personal and actionable these stories can be.

Do you think there's more to the story for United Airlines Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:UAL

United Airlines Holdings

Through its subsidiaries, provides air transportation services in the United States, Canada, Atlantic, the Pacific, and Latin America.

Undervalued with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative