Advertisement

Will Leadership Changes and a New Credit Facility Redefine CTS' (CTS) Capital Allocation Approach?

Simply Wall St

Reviewed by Sasha Jovanovic

- CTS Corporation recently announced the resignation of Senior Vice President Martin Baumeister, effective December 5, 2025, and the appointment of Pratik Trivedi as Chief Operating Officer, along with the establishment of a new five-year unsecured revolving credit facility of US$300 million to replace its previous US$400 million facility.

- This combination of leadership transition and financial restructuring signals active operational and balance sheet management aimed at supporting CTS's long-term growth and financial flexibility.

- We’ll explore how CTS’s new unsecured credit facility may influence its investment narrative and future capital allocation priorities.

Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

CTS Investment Narrative Recap

Shareholders in CTS need to believe in the company’s ability to diversify beyond a historically challenged transportation segment, coping with sector headwinds and capturing opportunities in medical and industrial markets. The recent leadership transition and new credit facility are unlikely to materially disrupt the main near-term catalyst, which continues to be revenue growth from newer markets, even as risks around transportation sales and global supply chain uncertainty remain at the forefront for many investors.

Of the recent corporate updates, CTS’s authorization of a new US$100 million share repurchase program stands out. This announcement is particularly relevant because it underscores the company’s ongoing focus on returning capital to shareholders, which could be appealing as management works to offset macroeconomic risks and cyclical weakness in key segments.

Yet, in contrast, investors should be aware of persistent softness in transportation sales and the impact this could have on overall revenue and...

Read the full narrative on CTS (it's free!)

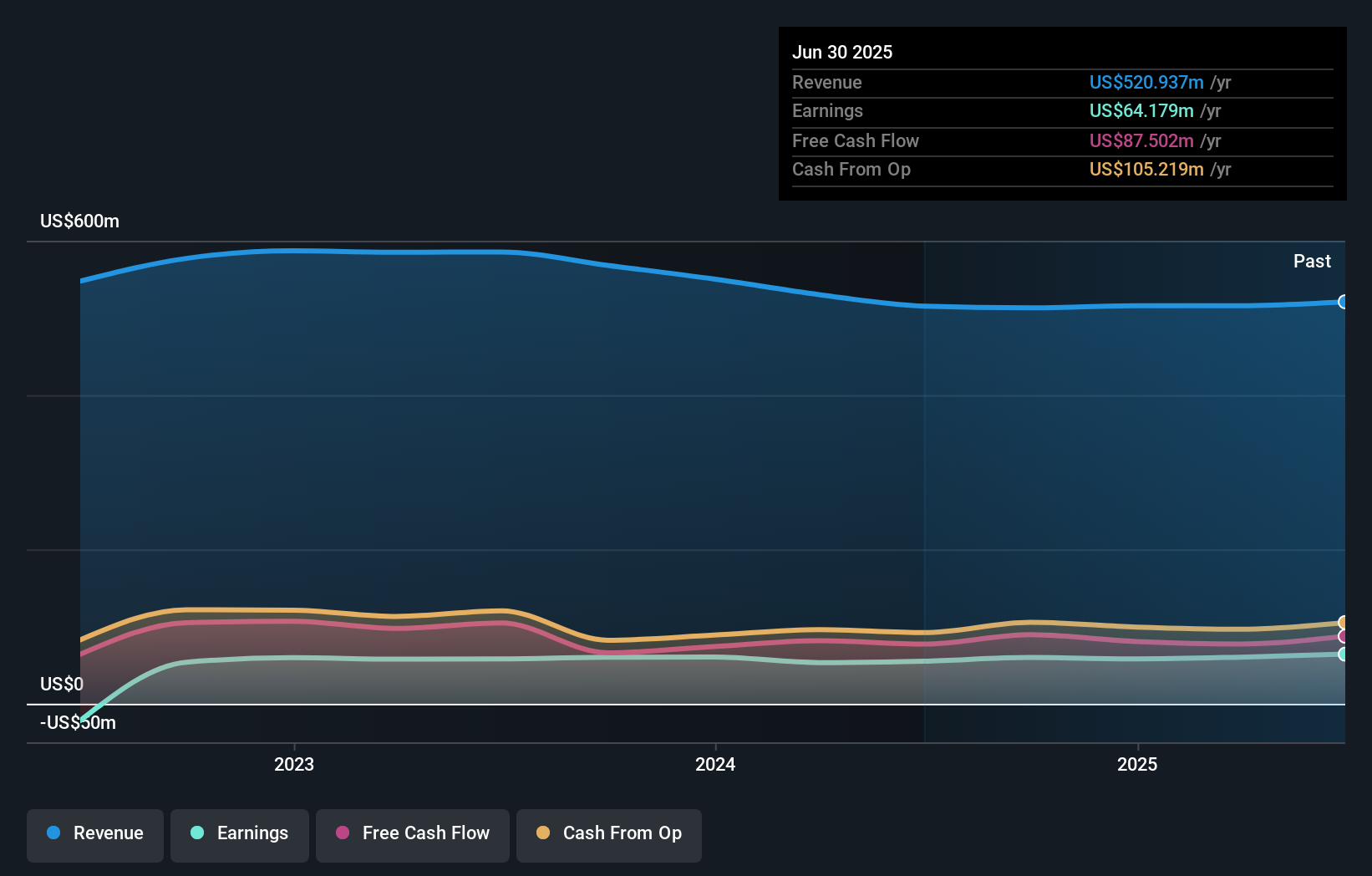

CTS' outlook anticipates $610.6 million in revenue and $78.8 million in earnings by 2028. Achieving these targets requires 5.4% annual revenue growth and a $14.6 million increase in earnings from the current level of $64.2 million.

Uncover how CTS' forecasts yield a $47.00 fair value, a 10% upside to its current price.

Exploring Other Perspectives

Two estimates from the Simply Wall St Community put fair value for CTS between US$43.30 and US$47.00 per share. With transportation market softness posing risks to both growth and profitability, consider the range of opinions before making any investment decisions.

Explore 2 other fair value estimates on CTS - why the stock might be worth just $43.30!

Build Your Own CTS Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your CTS research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free CTS research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CTS' overall financial health at a glance.

Ready For A Different Approach?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CTS

CTS

Designs, manufactures, and sells sensors, connectivity components, and actuators in North America, Europe, and Asia.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative