Advertisement

- United States

- /

- Tech Hardware

- /

- NasdaqGS:SNDK

Sandisk (SNDK): Evaluating Valuation Following Quarterly Earnings and New Revenue Guidance

Simply Wall St

Reviewed by Simply Wall St

Sandisk (SNDK) kicked off this week in the spotlight after releasing its first quarter earnings, showing a jump in sales but a drop in net income compared to last year. Investors are also weighing the company’s fresh revenue guidance for the upcoming quarter.

See our latest analysis for Sandisk.

After this strong earnings release and updated revenue outlook, Sandisk's stock has clearly grabbed the market’s attention, notching a remarkable 30-day share price return of 110%, and an even more eye-catching 686% year-to-date. The recent momentum suggests investors are rapidly reassessing Sandisk’s long-term potential as growth expectations shift.

If surging momentum in Sandisk has sparked your interest, now’s the perfect time to explore See the full list for free.

But with Sandisk shares surging so rapidly, the critical question now is whether the current price undervalues the company’s growth story, or if the market has already factored in all the future upside. Could there still be a buying opportunity?

Price-to-Sales of 5.3x: Is it justified?

Sandisk is currently trading at a price-to-sales ratio of 5.3x, with the share price sitting at $283.10. This makes the stock look expensive compared to its industry peers and historical benchmarks.

The price-to-sales (P/S) ratio is widely used for valuing tech companies, especially those with fluctuating or negative earnings. It compares a company’s market value to its revenue. For Sandisk, the current P/S ratio far exceeds both the US Tech sector average and its closest peer group, reflecting high investor expectations for future growth.

Compared to the US Tech industry average of 2.2x, Sandisk’s P/S ratio is notably higher. Even relative to the peer average of 2.8x and its own estimated fair ratio of 3.9x, the current valuation stands out as expensive. This suggests the market is pricing in significant growth, possibly more than what fundamentals may support if expectations shift.

Explore the SWS fair ratio for Sandisk

Result: Price-to-Sales of 5.3x (OVERVALUED)

However, the stock’s high valuation could be challenged if growth slows or if analyst price targets, which are currently below the share price, prove accurate.

Find out about the key risks to this Sandisk narrative.

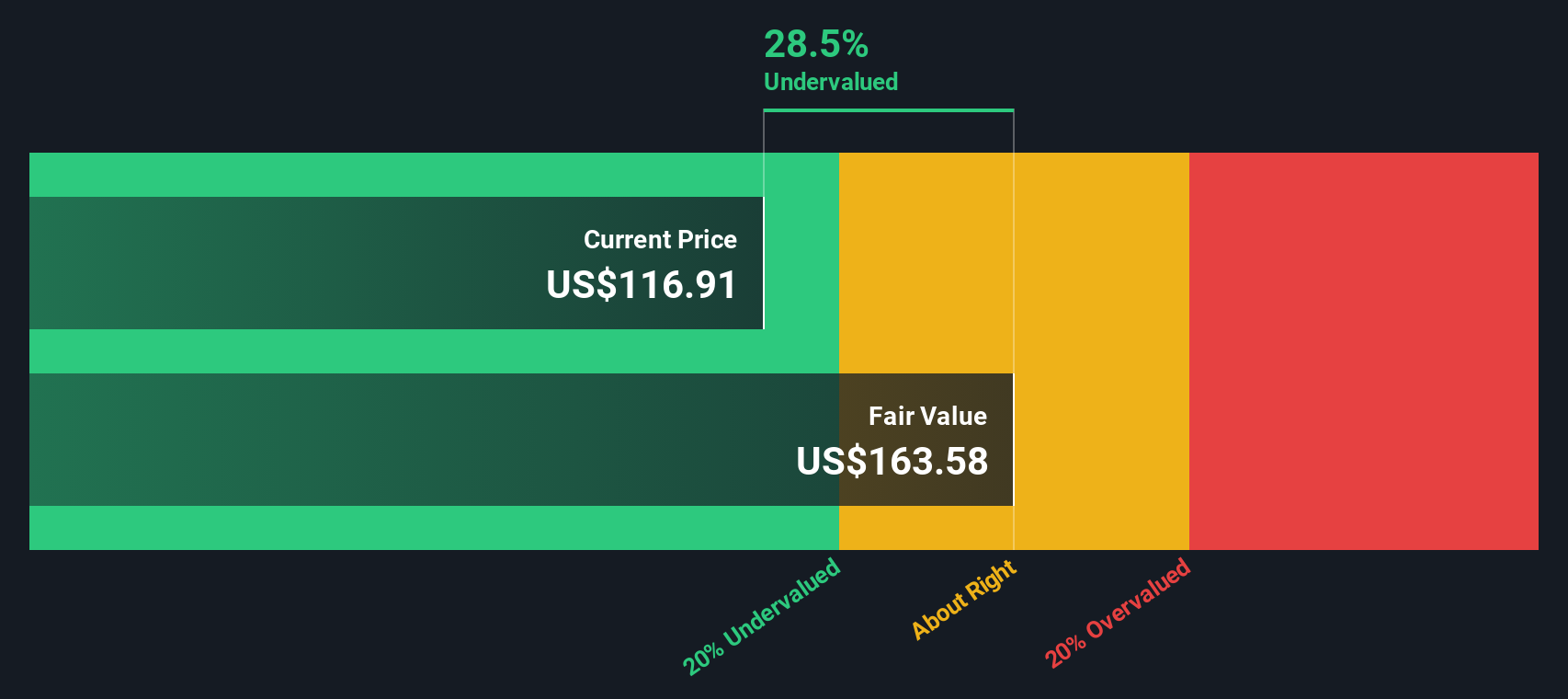

Another View: Discounted Cash Flow Model

While the price-to-sales ratio points to a richly valued stock, the SWS DCF model paints an even starker picture. According to this model, Sandisk shares are trading well above their estimated fair value of $83.41, which suggests that much of the optimism may already be reflected in the current price. Does this signal a reality check ahead for investors, or is the market seeing something models are missing?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Sandisk for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 865 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Sandisk Narrative

If you have a different perspective or enjoy digging into the numbers yourself, it takes just a few minutes to build your own view of Sandisk’s story. Do it your way.

A great starting point for your Sandisk research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Smart investors never stop at one opportunity. Take your portfolio to the next level by checking out these hand-picked stock ideas, all ready for you to action today.

- Boost your income by targeting high-potential opportunities using these 14 dividend stocks with yields > 3% for stocks with strong dividend yields and underlying stability.

- Unlock tomorrow’s potential and see which companies are shaping breakthroughs in artificial intelligence with these 25 AI penny stocks right now.

- Ride the next innovation wave by searching these 27 quantum computing stocks, which features stocks tapping into quantum computing’s future growth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:SNDK

Sandisk

Develops, manufactures, and sells data storage devices and solutions using NAND flash technology in the United States, Europe, the Middle East, Africa, Asia, and internationally.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor