Advertisement

- United States

- /

- Software

- /

- NYSE:HUBS

AI Integration Strategy and Strong Q3 Revenue Growth Could Be a Game Changer for HubSpot (HUBS)

Simply Wall St

Reviewed by Sasha Jovanovic

- Following its Q3 2025 earnings report, HubSpot posted 20.87% year-over-year revenue growth, fueled by rising subscription and professional services demand, and highlighted its AI integration strategy for small and medium-sized businesses at Wells Fargo’s 9th Annual TMT Summit.

- Management’s focus on embedding AI across HubSpot’s platform signals a technology shift aimed at improving accessibility and workflow efficiency for customers.

- We’ll explore how HubSpot’s expanded AI strategy could influence its long-term investment outlook and competitive positioning.

Find companies with promising cash flow potential yet trading below their fair value.

HubSpot Investment Narrative Recap

To be a HubSpot shareholder today, you need confidence in its ability to capture ongoing digital migration by SMBs and leverage integrated AI to drive workflow efficiency and customer adoption. While the company’s solid Q3 results, highlighted by strong revenue growth and further AI integration, reinforce existing growth catalysts, a sharp post-earnings share price drop suggests market sentiment is cautious. The news does not materially alter the biggest near-term catalyst or the primary risk, namely SMB customer volatility in uncertain economic climates.

One of the most relevant recent announcements for this context is HubSpot’s expansion of AI features across its CRM platform, showcased at the Wells Fargo TMT Summit and reinforced by integrations like the AI assistant for lead qualification. These developments align with key catalysts: more robust AI innovation and cross-platform adoption can support customer stickiness and revenue, yet their early-stage monetization means investors are still watching for proof of durable impact.

By contrast, investors should be aware of the uncertain pace of adoption and monetization for HubSpot’s new AI-driven features, as...

Read the full narrative on HubSpot (it's free!)

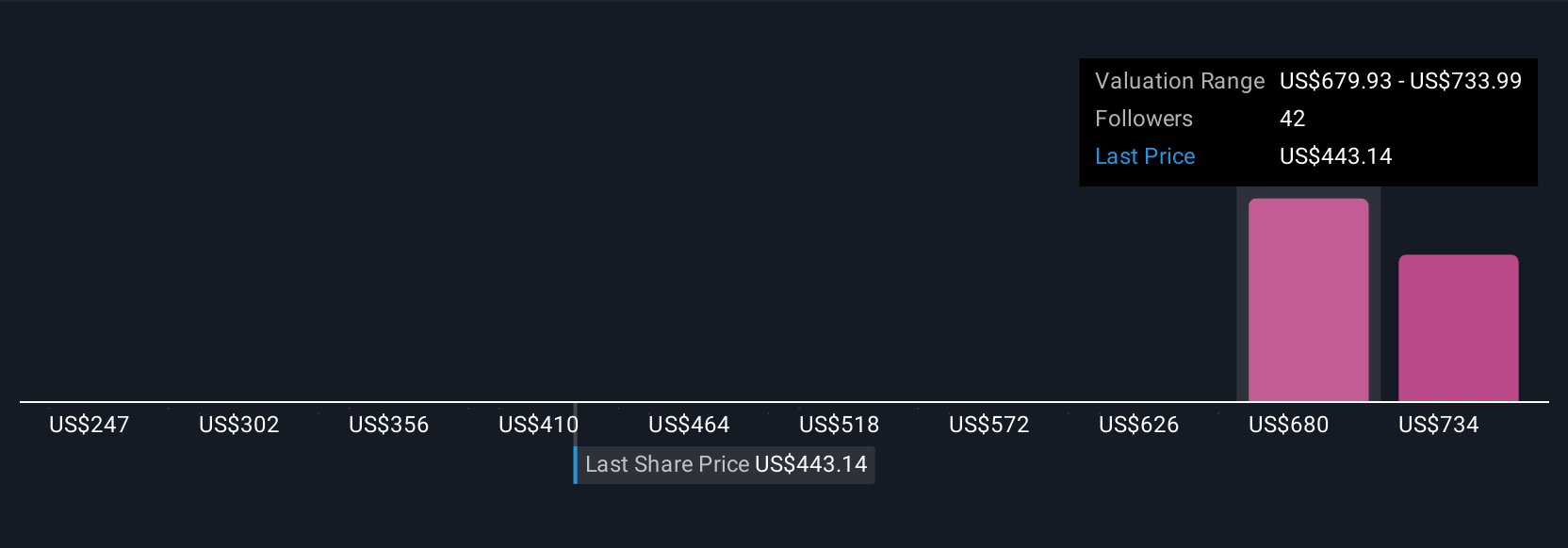

HubSpot's narrative projects $4.6 billion revenue and $388.4 million earnings by 2028. This requires 17.1% yearly revenue growth and a $400.3 million increase in earnings from -$11.9 million today.

Uncover how HubSpot's forecasts yield a $593.90 fair value, a 64% upside to its current price.

Exploring Other Perspectives

Eight individual fair value estimates from the Simply Wall St Community rate HubSpot between US$204.71 and US$593.90 per share. While many participants see upside, the early results of HubSpot’s AI monetization strategy remain pivotal for its future performance, so consider these varied perspectives as you weigh your next step.

Explore 8 other fair value estimates on HubSpot - why the stock might be worth as much as 64% more than the current price!

Build Your Own HubSpot Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your HubSpot research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free HubSpot research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate HubSpot's overall financial health at a glance.

Seeking Other Investments?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 35 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if HubSpot might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HUBS

HubSpot

Provides a cloud-based customer relationship management (CRM) platform for businesses in the Americas, Europe, and the Asia Pacific.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative