Advertisement

- United States

- /

- Software

- /

- NasdaqGM:DOMO

Domo (DOMO) Narrows Q3 Net Loss, Testing Bearish Profitability Narratives

Simply Wall St

Reviewed by Simply Wall St

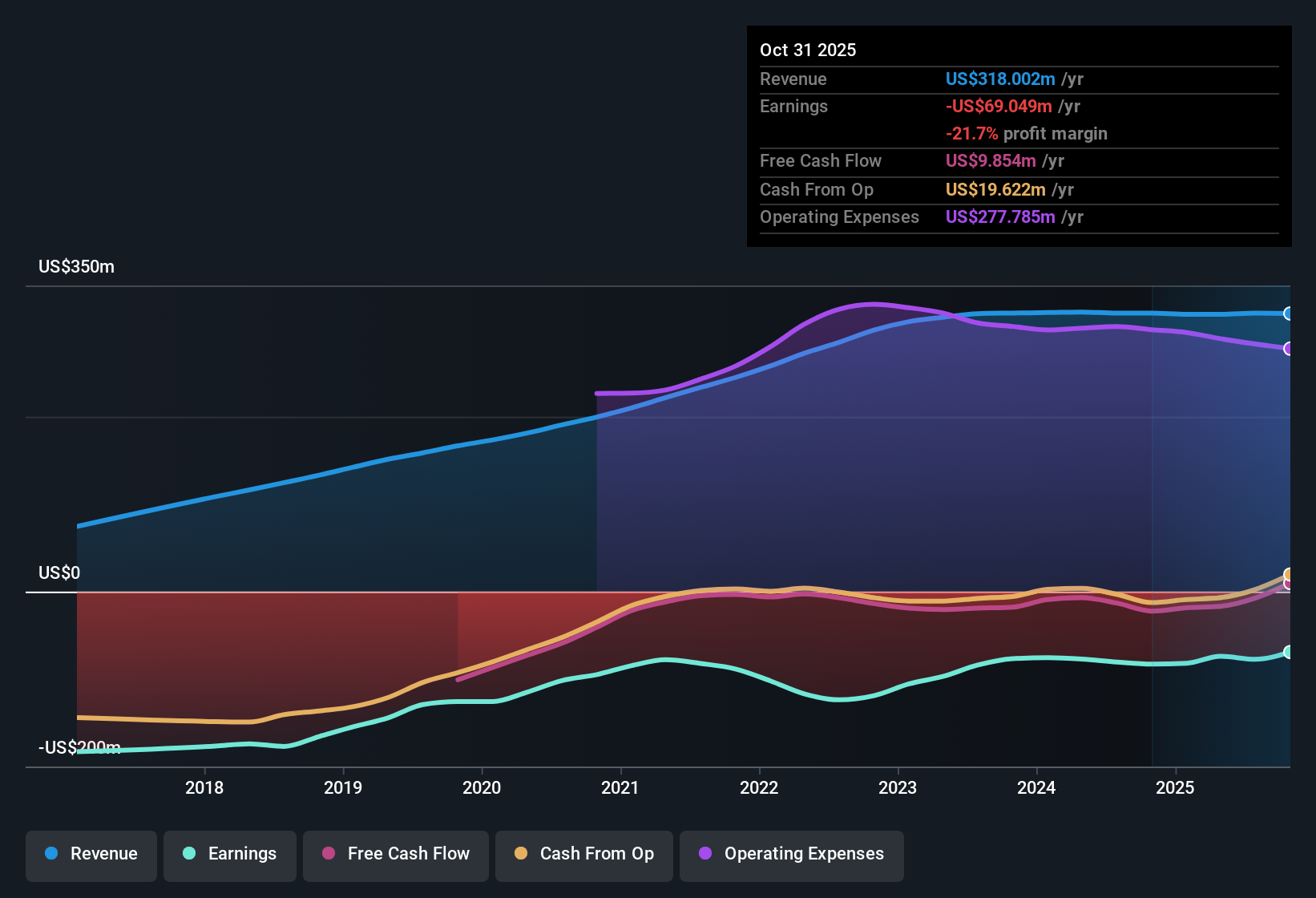

Domo (DOMO) has just put Q3 2026 on the books with revenue of about $79.4 million and a basic EPS loss of roughly $0.25, keeping the focus firmly on how efficiently the business is converting its topline into sustainable earnings. The company has seen quarterly revenue hover in a tight band around $78 million to $80 million over the past six reported periods, while EPS has similarly stayed in negative territory between approximately $0.25 and $0.56 per share, underscoring that margins remain under pressure even as the topline holds steady.

See our full analysis for Domo.With the numbers on the table, the next step is to see how this latest margin picture lines up with the dominant narratives around Domo’s path to profitability and long term growth on Simply Wall St.

See what the community is saying about Domo

Losses Narrow But Stay Meaningful

- Net loss improved to about $10.4 million in Q3 2026 versus roughly $22.9 million in Q2 2026, while trailing 12 month losses are still sizable at about $69.0 million.

- Bears argue that ongoing unprofitability and no forecasted break even over the next three years limit how much this improvement really helps, even with better quarterly numbers.

- The trailing 12 month net loss of about $69.0 million and negative Basic EPS of about $1.71 show that, despite a better Q3, the business is still far from positive earnings.

- With revenue over the last year at about $318.0 million and still no path to profitability in the forecasts, the concern is that margins remain structurally weak rather than just temporarily pressured.

Slow Growth, Attractive Sales Multiple

- Revenue has grown about 3.7% per year over the last 12 months, but the stock trades at roughly 1.1 times sales, well below peers at 1.9 times and the broader software industry at about 5 times.

- Supporters highlight that this lower multiple could matter if Domo can keep even modest growth going, despite the slower 3.7% revenue pace versus a 10.6% forecast for the wider US market.

- Compared with that 10.6% broader market growth expectation, Domo’s slower trajectory may explain the discount, yet the current 1.1 times sales still looks inexpensive against industry benchmarks.

- If the company continues to trim losses, as seen in the move from roughly $81.9 million trailing loss in 2025 Q4 to about $69.0 million now, investors could start to see more upside in that discounted sales multiple.

Balance Sheet Risk Versus DCF Upside

- The stock changes hands around $8.84 while the stated DCF fair value is about $11.28 per share, a discount of roughly 21.7%, yet the company also carries negative shareholders’ equity.

- Consensus style thinking is that this mix of a wide valuation gap and a weak balance sheet makes Domo a higher risk, higher potential reward idea rather than a simple value pick.

- The 21.7% gap between price and DCF fair value suggests room for upside if the business keeps reducing losses at roughly 5.3% per year as it has over the last five years.

- At the same time, negative equity and expectations of continued losses over the next three years mean that any move toward that $11.28 DCF fair value depends heavily on execution rather than balance sheet strength.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Domo on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers differently? Use that insight to quickly build and share your own take on Domo’s outlook in just a few minutes, Do it your way.

A great starting point for your Domo research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Explore Alternatives

Domo’s persistent losses, slow revenue growth, negative equity and lack of a clear path to profitability highlight meaningful financial fragility and balance sheet risk.

If that level of pressure feels uncomfortable, use our solid balance sheet and fundamentals stocks screener (1941 results) to quickly focus on companies built on stronger finances, lower leverage and more durable earnings power.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:DOMO

Domo

Operates a cloud-based modern AI and data products platform in North America, Western Europe, Australia, Japan, and India.

Fair value with very low risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4727.3% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$481.5% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative