Advertisement

- United States

- /

- Software

- /

- NasdaqGS:BRZE

Braze (BRZE) Is Up 9.1% After Raised Guidance and Revenue Beat Despite EPS Miss Has The Bull Case Changed?

Simply Wall St

Reviewed by Simply Wall St

- Earlier this week, Braze reported strong revenue growth and raised its full-year guidance, but its EPS outlook came in below analyst expectations following its latest earnings report.

- Management highlighted ongoing momentum in enterprise and international markets, underscoring their confidence that current macroeconomic or industry risks are not expected to materially impact guidance.

- We'll explore how Braze's raised full-year guidance, despite an EPS shortfall, shapes its evolving investment narrative and outlook.

Braze Investment Narrative Recap

To be a Braze shareholder, you need confidence in its ability to drive consistent revenue growth through international expansion and enterprise momentum, while managing profitability challenges in a competitive software market. The recent earnings report, despite strong revenue and raised full-year guidance, does not materially alter the prevailing short term catalysts, particularly further adoption in enterprise verticals, or the primary risk around maintaining net margins as the company continues to scale and integrate new technology.

Of the recent announcements, the deepened partnership with Shopify most directly speaks to Braze’s catalyst for growth: expanding its reach and differentiation for e-commerce brands. This collaboration is intended to enhance real-time consumer engagement, which aligns with the company’s focus on boosting enterprise deal sizes and supporting vertical expansion, reinforcing the revenue growth story highlighted in the latest quarterly results.

Yet, in contrast, investors should not overlook the ongoing risks tied to Braze’s unprofitability and the potential impact of integrating OfferFit on net margins...

Read the full narrative on Braze (it's free!)

Braze's forecast envisions $944.1 million in revenue and $113.7 million in earnings by 2028. This relies on an annual revenue growth rate of 16.7% and an earnings increase of $217.4 million from the current earnings of -$103.7 million.

Uncover how Braze's forecasts yield a $53.14 fair value, a 84% upside to its current price.

Exploring Other Perspectives

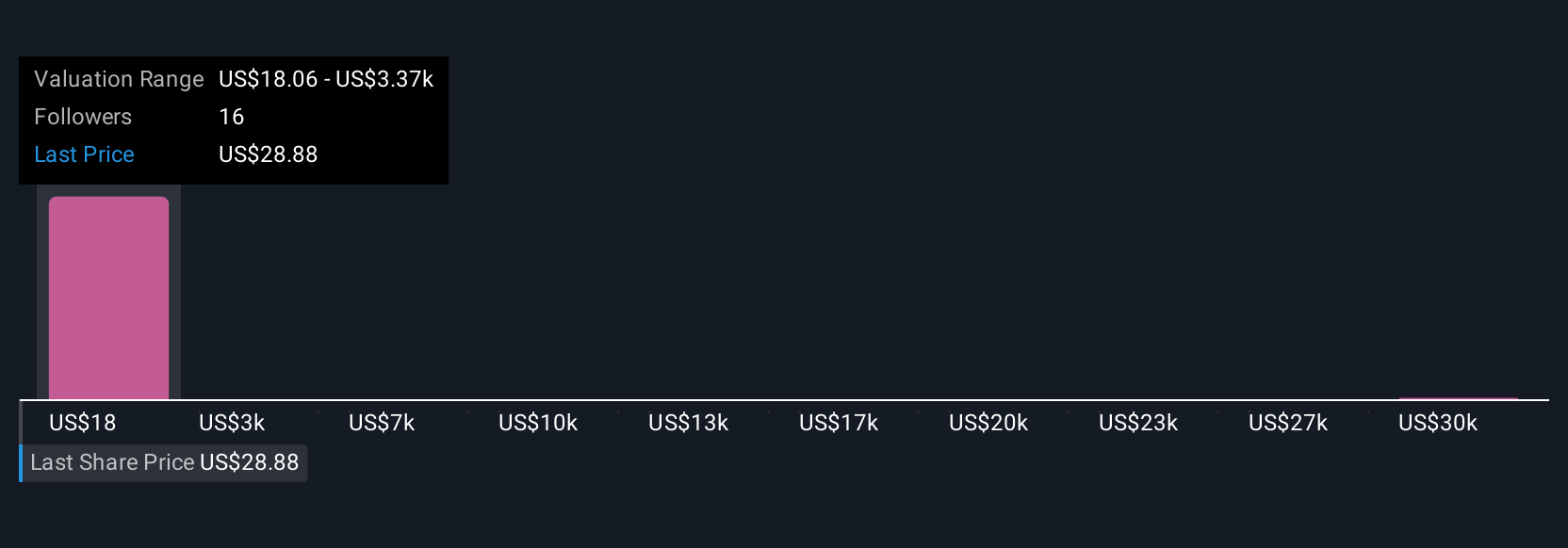

Simply Wall St Community investors provided three fair value estimates for Braze, ranging from US$18.02 to US$33,504.83 per share. With performance expectations shaped by international expansion, be aware that opinions differ widely, consider exploring alternative analyses and their implications for Braze’s path forward.

Build Your Own Braze Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Braze research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Braze research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Braze's overall financial health at a glance.

Want Some Alternatives?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- These 17 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The end of cancer? These 25 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Braze might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:BRZE

Braze

Operates a customer engagement platform that provides interactions between consumers and brands worldwide.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|36.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.0% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|46.4% overvalued

DA

Community Contributor