Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:MU

Is Micron’s Recent 14% Rally Justified Amidst New Memory Chip Breakthrough?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Micron Technology is really worth today’s price? If you’re sizing up the semiconductor giant, you’re not alone in wanting to know what truly drives its value.

- The stock has put on an impressive show, leaping 14.0% just this past week and rising 170.8% year-to-date, a trend that has caught the eye of growth-focused investors as well as those concerned about high valuation levels.

- Micron recently made headlines with major breakthroughs in memory chip development and new supply deals, which have been key factors in its recent climb. Industry reports about tight chip supply and strong demand for AI hardware have also contributed to the rally.

- Our latest check gives Micron a 3 out of 6 on our Value Score. This indicates it is considered undervalued on three of six checks, but there is much more to consider. Next, we’ll explore the different ways investors are evaluating Micron, and explain why a forward-looking perspective can be important.

Approach 1: Micron Technology Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by projecting its future cash flows and discounting them back to the present. This method focuses on what the business can realistically generate in the years ahead, making it especially useful for growth-oriented companies like Micron Technology.

Currently, Micron’s Free Cash Flow stands at $2.22 Billion. Analyst estimates show a sharp rise in Free Cash Flow over the next five years, with projected figures reaching $8.56 Billion by 2026 and as high as $10.60 Billion by 2030. Only the initial five years are based on analyst consensus, with the model extrapolating beyond that using historical trends and industry analysis. This reflects the cyclical but upward trajectory of the semiconductor market.

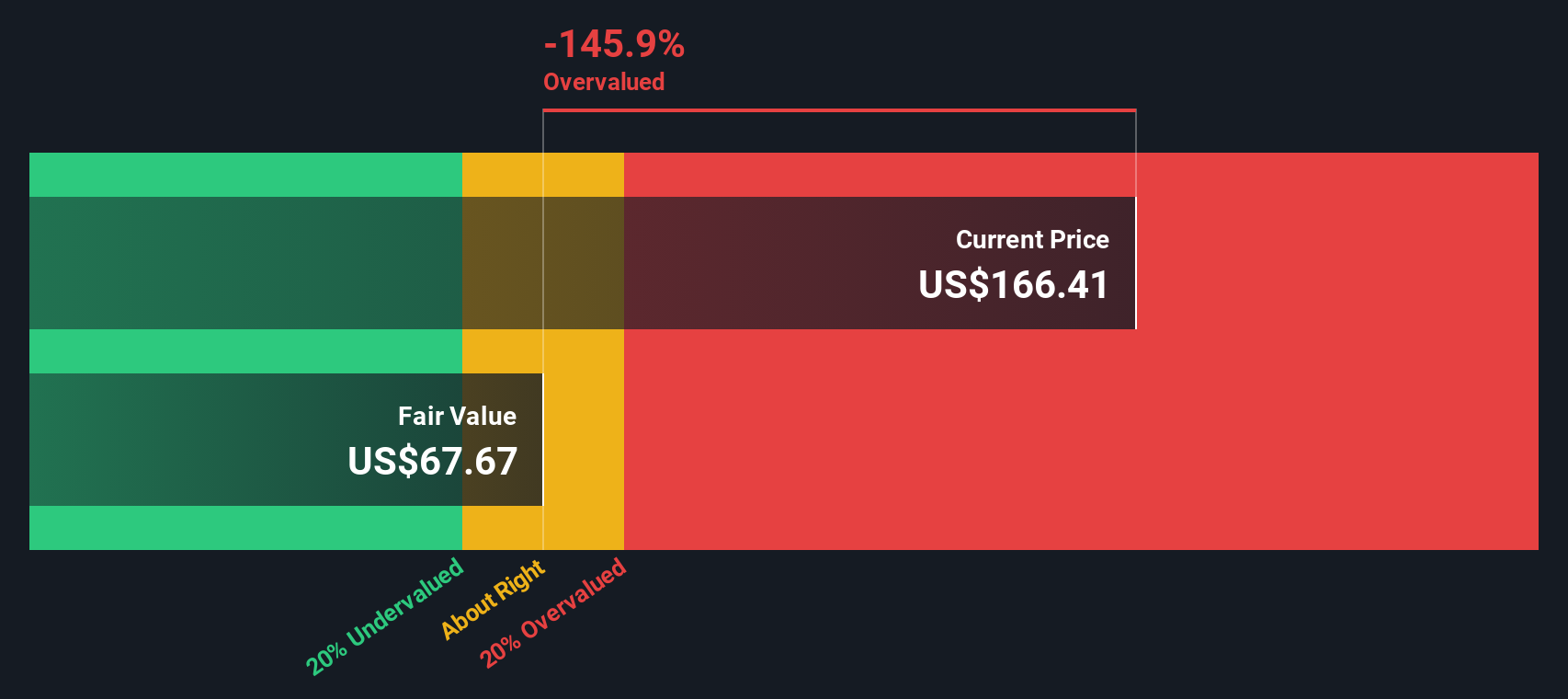

According to this DCF analysis, Micron’s intrinsic value is calculated at $103.86 per share. With its current market price trading 127.7% above this estimate, the stock appears significantly overvalued on a cash-flow basis.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Micron Technology may be overvalued by 127.7%. Discover 920 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Micron Technology Price vs Earnings

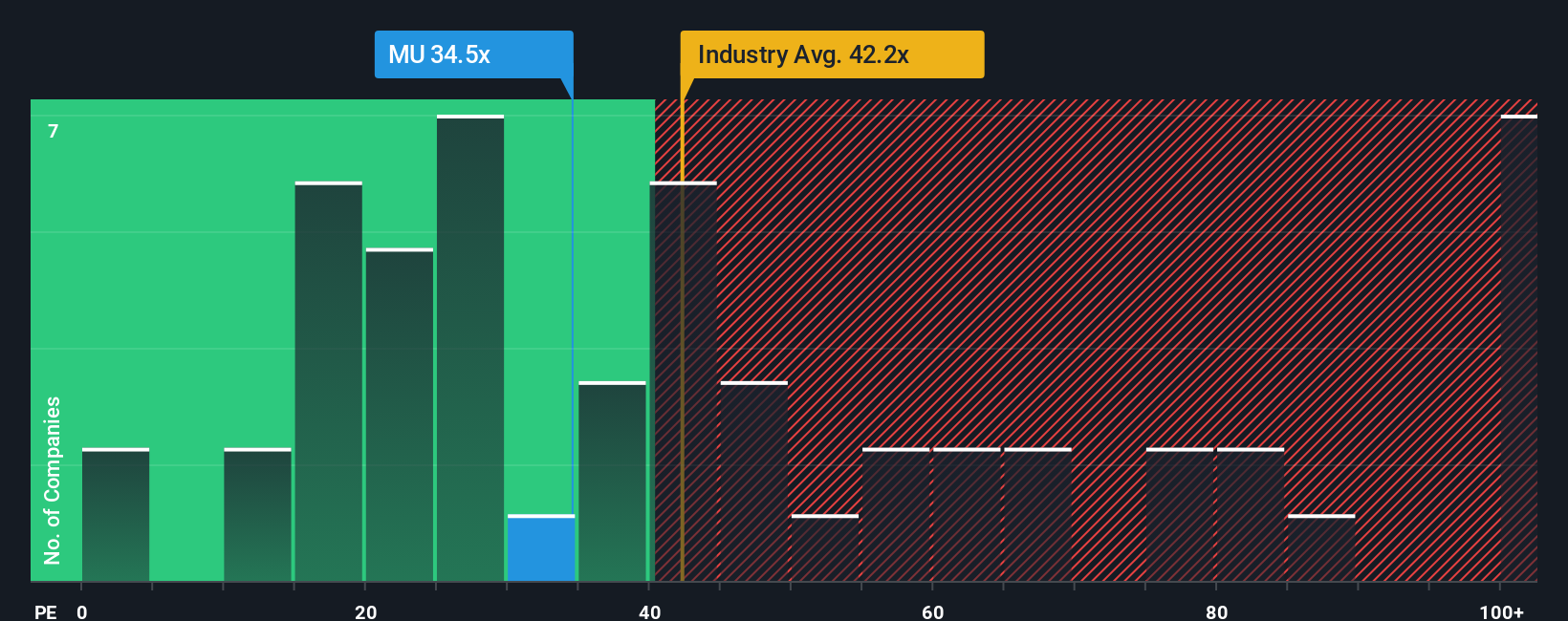

The Price-to-Earnings (PE) ratio is a useful way to assess valuation for profitable companies like Micron Technology, giving investors a quick sense of how much they are paying for each dollar of earnings. Since Micron has returned to profitability, using the PE ratio is especially relevant, as it reflects both current earnings power and market expectations.

Growth outlook and risk level are important when interpreting what qualifies as a “normal” or “fair” PE ratio. Companies with higher expected earnings growth or lower risk typically trade at higher multiples, while more mature or volatile businesses are assigned lower ones by the market.

Currently, Micron trades at a PE ratio of 31.1x. This is somewhat below the semiconductor industry average of 36.1x, but well below the peer group average of 87.3x. However, these simple comparisons can overlook important context about Micron’s individual growth prospects and risk factors. This is where Simply Wall St’s “Fair Ratio” comes in; this proprietary figure, 43.6x for Micron, distills information about its growth outlook, profit margins, market cap, and risk profile.

Unlike comparing to industry or peers in isolation, the Fair Ratio provides a more tailored benchmark for today’s market environment. Since Micron’s actual PE of 31.1x is noticeably below its calculated Fair Ratio of 43.6x, the stock appears undervalued by this measure.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Micron Technology Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is simply a story, or your personal investment perspective, that connects the numbers to what you believe about a company like Micron Technology: how its business might grow, what margins it could achieve, and what you think is a fair value based on your unique assumptions.

Narratives are powerful because they combine your understanding of Micron’s story with the hard data, linking forecasts to financial value, helping you see not just where the company is, but where it could go. With Simply Wall St’s Community page, millions of investors can easily create and share Narratives in just a few steps, even if you're new to financial analysis.

By building a Narrative, you can immediately compare your estimated fair value with Micron’s current share price, making it easier to decide when it makes sense to buy or sell. Narratives also update automatically when key events, such as earnings reports or big news, change the company’s outlook, so your analysis stays up to date without extra work.

For example, some investors now see Micron’s fair value as high as $203.92 per share, reflecting sustained AI demand. Others are cautious, valuing it as low as $95 and emphasizing competitive and macroeconomic risks. This highlights how different stories can lead to different investment decisions.

Do you think there's more to the story for Micron Technology? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:MU

Micron Technology

Designs, develops, manufactures, and sells memory and storage products in the United States, Taiwan, Singapore, Japan, Malaysia, China, India, and internationally.

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative