Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:KLAC

Should You Reconsider KLA After an 82% Rally and Analyst Upgrades in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

- If you have ever wondered whether KLA's rapid rise is justified and if there is still value to be found at these levels, you are not alone.

- KLA's stock price has delivered explosive returns in 2024, up 82.1% year-to-date and 80.7% over the last year. Recent weeks have seen a healthy pullback of 6.2% in the last month.

- Investors have been buzzing about KLA after a flurry of analyst upgrades and increased attention on semiconductor stocks, thanks to growing demand in AI and advanced manufacturing. New partnerships and expanding customer relationships have also helped push the stock into the spotlight, driving both optimism and some caution among the investing crowd.

- KLA currently scores a 1 out of 6 on our undervaluation checks, suggesting there are key factors still worth scrutinizing. Let’s explore the traditional valuation methods and stick around for a fresh perspective that could change how you assess the stock’s true worth.

KLA scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: KLA Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's value by forecasting its future cash flows and discounting them back to today's value. This approach aims to capture what the business is worth based on its ability to generate cash over time, rather than relying just on current earnings or book value.

For KLA, analysts estimate the company's current Free Cash Flow at $3.88 Billion, and project it to grow to $6.83 Billion by 2030. Over the next five years, forecasts show steady annual increases in Free Cash Flow, driven partly by ongoing demand in the semiconductor sector. Beyond 2028, additional years are extrapolated to provide investors with a longer-term look at the company’s earning potential.

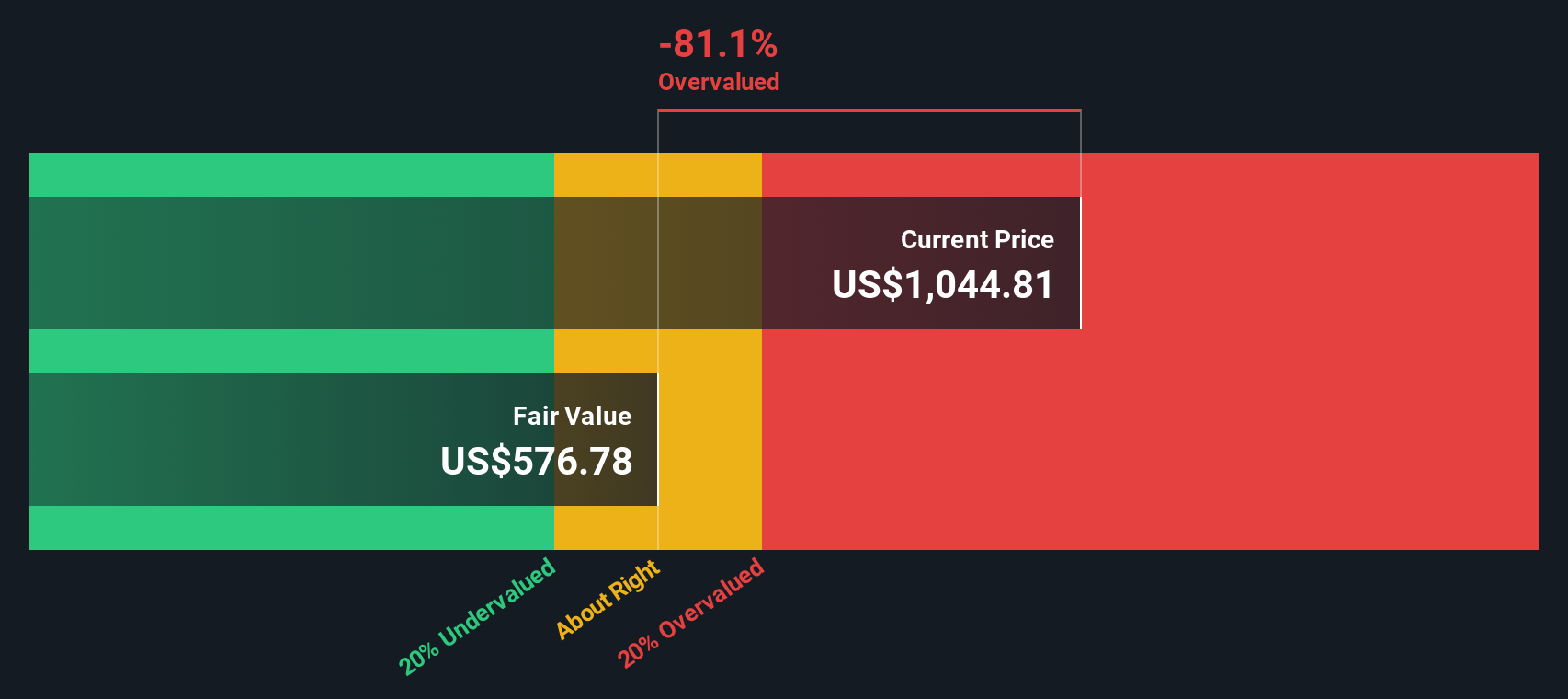

Based on these cash flow projections and discounting them to present value, the DCF model calculates KLA’s intrinsic value at $655.81 per share. Compared to KLA’s current share price, this suggests the stock is about 76.7% overvalued by this measure.

The takeaway is that even with optimistic growth, KLA’s share price currently exceeds its DCF-based fair value, suggesting investors should tread carefully at these levels.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests KLA may be overvalued by 76.7%. Discover 923 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: KLA Price vs Earnings

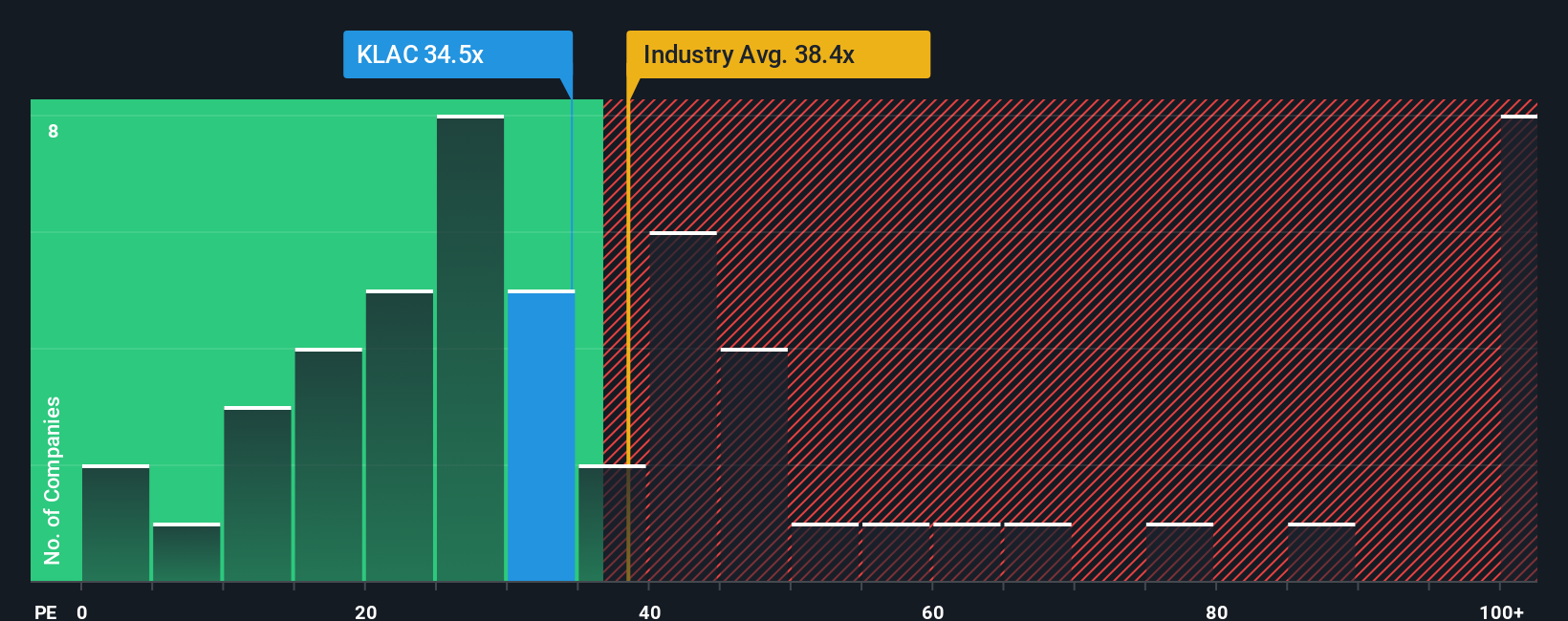

The Price-to-Earnings (PE) ratio is a widely used metric for valuing profitable companies like KLA. It tells investors how much they are paying for each dollar of earnings. This makes it an effective way to compare value among mature, profit-generating businesses.

Growth expectations and perceived risk play a big role in what counts as a "normal" or "fair" PE ratio. Companies expected to post stronger future earnings or with stable, low-risk profiles often command higher PE multiples. In contrast, slower growth or higher risk tends to lower the desirable PE.

KLA currently trades on a PE ratio of 35.9x. This is just below the Semiconductor industry average of 35.8x and slightly under the peer group average of 36.5x. However, simply comparing to peers or the industry can overlook important factors unique to KLA, such as its specific earnings outlook, risk profile, market cap, and profitability.

This is where Simply Wall St’s “Fair Ratio” comes in. This proprietary metric reflects the PE multiple you would expect given a company’s growth, profits, industry, and risk characteristics. For KLA, the Fair Ratio is calculated to be 33.1x. This is a bit lower than KLA’s current PE, indicating the stock might be slightly overvalued relative to what would be considered fair based on its circumstances.

Since the difference between KLA's current PE and its Fair Ratio is greater than 0.10, it suggests the stock is somewhat expensive at these levels.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1437 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your KLA Narrative

Earlier, we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is a concise story that expresses your perspective on a company, connecting what you believe about its future (like revenue, earnings, and margins) to a financial forecast and ultimately a fair value estimate.

With Narratives, you are no longer just looking at static numbers. You are expressing your reasoning and assumptions directly and seeing how they translate to a share price. Narratives make it easy for anyone, regardless of experience level, to test their ideas and understand what needs to happen for a stock to be a "good" buy or sell.

Available on Simply Wall St's Community page and used by millions of investors, Narratives let you compare your view side-by-side with others and see how your assumptions stack up. They also update dynamically whenever new information, such as news or earnings, comes out, so your valuation always reflects the latest facts.

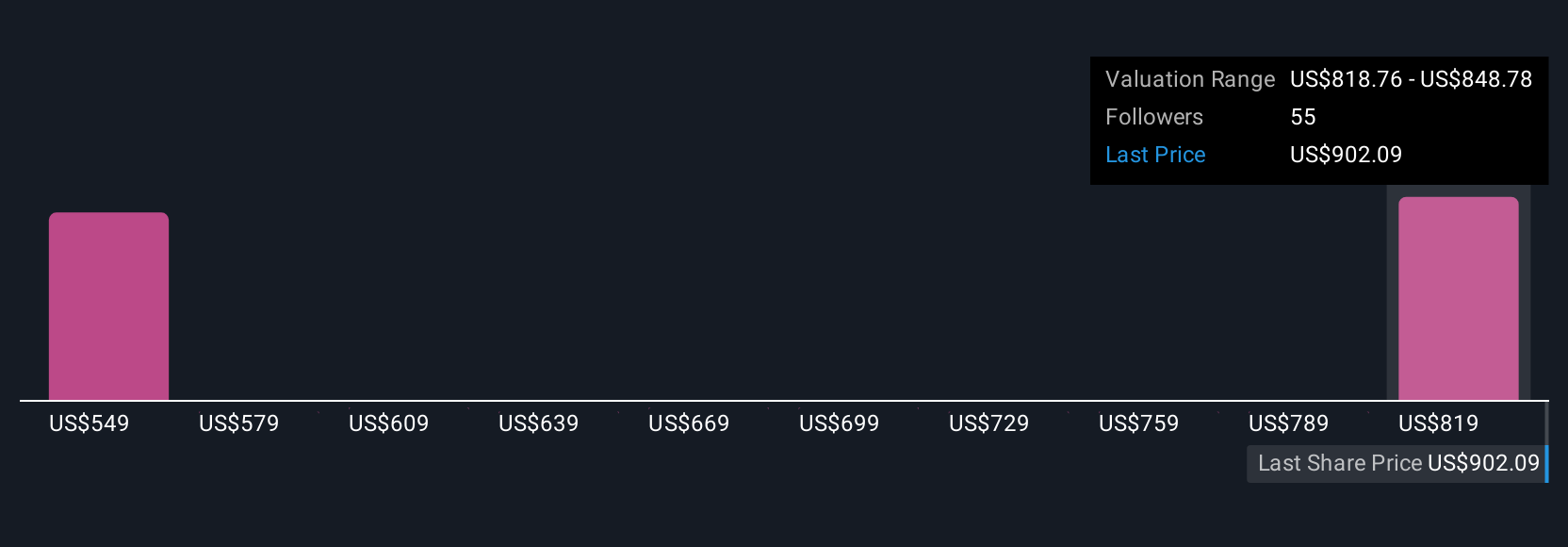

For example, for KLA, some investors with bullish outlooks for the AI and DRAM markets have Narratives that estimate a fair value as high as $1,075, while more cautious perspectives place it closer to $745. This enables you to see exactly what drives those differences and decide which outlook you agree with.

Do you think there's more to the story for KLA? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if KLA might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:KLAC

KLA

Designs, manufactures, and markets process control, process-enabling, and yield management solutions for the semiconductor and related electronics industries worldwide.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1359.3% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

99 followersusers have followed this narrative

10 commentsusers have commented on this narrative

19 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative