Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:CSIQ

Why Canadian Solar (CSIQ) Is Up 17.9% After Beating Q3 Revenue Forecasts and Securing Storage Deals

Simply Wall St

Reviewed by Sasha Jovanovic

- Canadian Solar reported third-quarter 2025 revenue of US$1.49 billion, exceeding analyst forecasts, alongside a return to net income despite a slight year-over-year sales decline.

- Recent large-scale energy storage contract wins in Canada, Germany, and Australia highlight momentum in the company’s e-STORAGE segment, with a contracted backlog of US$3.1 billion as of June 2025.

- We'll consider how Canadian Solar’s strong e-STORAGE results and new contracts could influence its long-term earnings outlook and growth narrative.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

Canadian Solar Investment Narrative Recap

To own Canadian Solar, one needs to believe in the global growth of renewables and the company’s ability to scale its energy storage segment faster than rising costs and industry competition can erode margins. The latest earnings beat and energy storage contracts are positive, but with fourth-quarter revenue guidance falling short of market hopes, they do little to ease immediate margin pressure from rising manufacturing and policy risks.

Among recent announcements, Canadian Solar’s e-STORAGE win for the massive Skyview 2 project in Ontario, a 411 MW/1,858 MWh system with a 21-year service contract, stands out. This contract adds long-term visibility and scale to the e-STORAGE backlog, reinforcing the segment’s role as a key growth driver and offset to manufacturing headwinds.

Yet, in contrast to the optimism, investors should be aware of ongoing margin pressure from rising input costs and intense module price competition...

Read the full narrative on Canadian Solar (it's free!)

Canadian Solar's outlook anticipates $8.0 billion in revenue and $201.9 million in earnings by 2028. This is based on a projected 10.4% annual revenue growth rate and an increase in earnings of about $208.8 million from the current level of -$6.9 million.

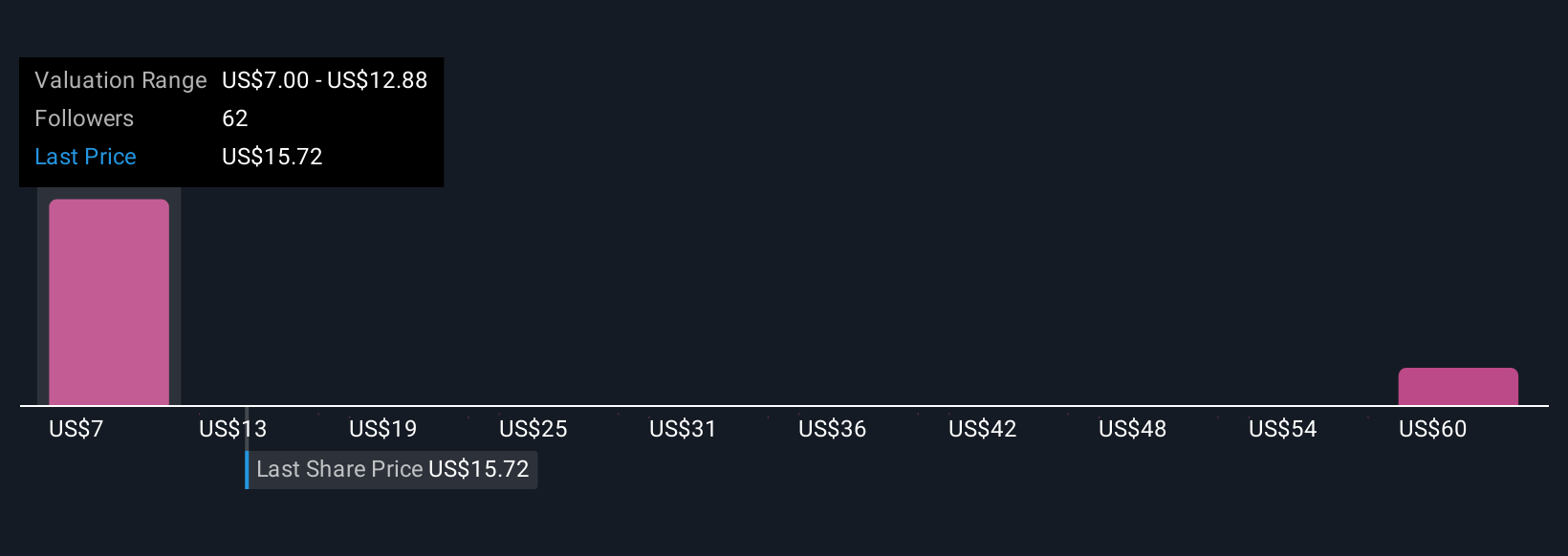

Uncover how Canadian Solar's forecasts yield a $13.26 fair value, a 61% downside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community estimate fair value for Canadian Solar, ranging from US$7 to US$65.75. While opinions vary, many remain focused on whether rising supply chain costs could weigh down profitability and future results, explore how these views could affect your perspective.

Explore 5 other fair value estimates on Canadian Solar - why the stock might be worth as much as 96% more than the current price!

Build Your Own Canadian Solar Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Canadian Solar research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Canadian Solar research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Canadian Solar's overall financial health at a glance.

Interested In Other Possibilities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Find companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 36 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CSIQ

Canadian Solar

Provides solar energy and battery energy storage products and solutions in Asia, the Americas, Europe, and internationally.

Undervalued with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor