Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:ARM

Is Rising Competition From RISC-V Challenging the Investment Case for Arm Holdings (ARM)?

Simply Wall St

Reviewed by Sasha Jovanovic

- In recent days, analysts and industry observers have highlighted Arm Holdings’ steep valuation, raising concerns about whether its business model and financial outlook can justify such a premium. A key point of discussion is the rising competitive threat posed by the royalty-free RISC-V architecture, which is being supported by major technology firms including Google and Meta.

- We will examine how growing investor unease over Arm's ability to deliver rapid profit and revenue gains amid structural competition risk could influence its investment narrative.

AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Arm Holdings Investment Narrative Recap

To be a shareholder in Arm Holdings today, you would need to believe that the company’s technology is indispensable for future AI and data center growth, and that it can defend premium royalty rates even as competition intensifies. The recent news highlighting Arm’s 200x earnings multiple and rising RISC-V adoption may add to concerns, but it does not materially affect the main short-term catalyst, AI-driven revenue acceleration, or the key risk presented by disruptive open-source alternatives.

Amid these headlines, Arm’s recent announcement of its strongest second quarter ever, with Q2 sales up to US$1,135 million and substantial operating income growth, remains highly relevant. This performance underpins the company’s AI narrative and signals that, for now, core demand is intact, even as questions mount around competitive threats and elevated expectations.

In contrast, investors should also be aware that accelerating adoption of open-source architectures by large customers...

Read the full narrative on Arm Holdings (it's free!)

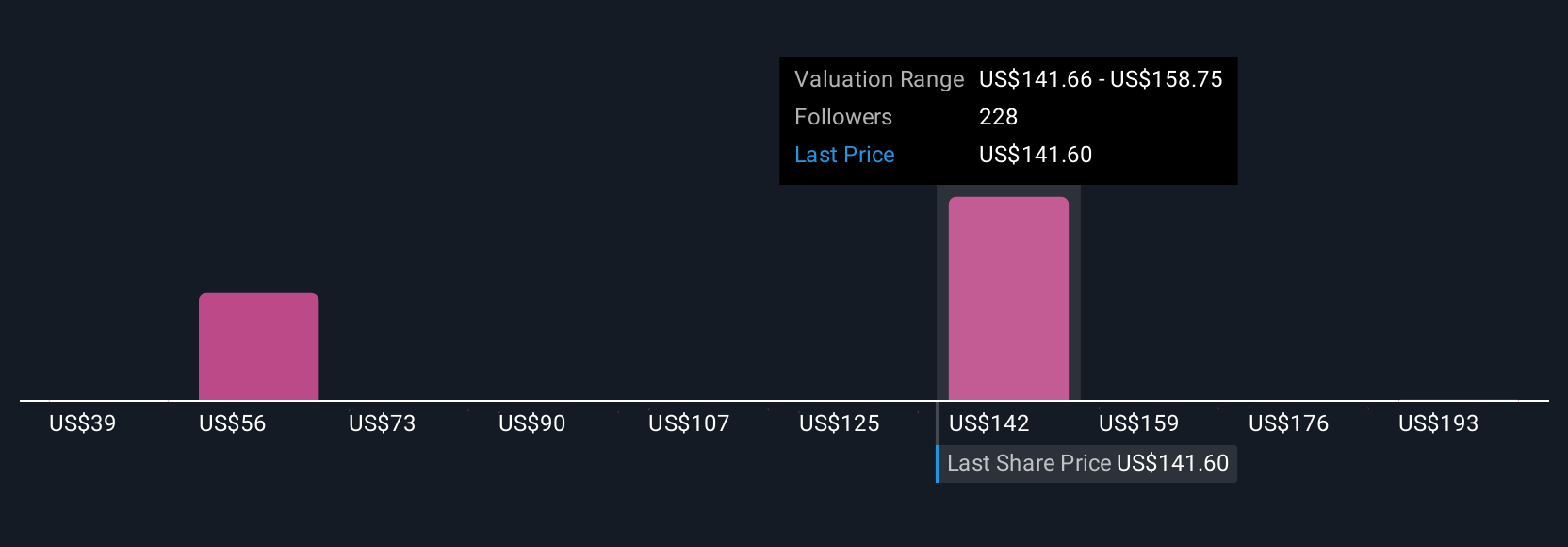

Arm Holdings' narrative projects $7.4 billion revenue and $2.3 billion earnings by 2028. This requires 21.5% yearly revenue growth and a $1.6 billion increase in earnings from $699.0 million.

Uncover how Arm Holdings' forecasts yield a $167.97 fair value, a 27% upside to its current price.

Exploring Other Perspectives

The most optimistic analysts were projecting Arm’s annual revenue could hit US$8.6 billion by 2028, but those forecasts hinge on exceeding even recent growth rates and facing less competition. If you think the news makes Arm’s risk from open-source rivals like RISC-V more pressing, it’s worth considering how sharply investor views and the company’s outlook might shift from here.

Explore 17 other fair value estimates on Arm Holdings - why the stock might be worth as much as 58% more than the current price!

Build Your Own Arm Holdings Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Arm Holdings research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Arm Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Arm Holdings' overall financial health at a glance.

Seeking Other Investments?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Outshine the giants: these 25 early-stage AI stocks could fund your retirement.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ARM

Arm Holdings

Arm Holdings plc architects, develops, and licenses central processing unit products and related technologies for semiconductor companies and original equipment manufacturers.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1359.3% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

99 followersusers have followed this narrative

10 commentsusers have commented on this narrative

19 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative