Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:ALAB

Astera Labs (ALAB): Evaluating Valuation as Analyst Praise and Azure Wins Highlight AI Data Center Momentum

Simply Wall St

Reviewed by Simply Wall St

Astera Labs (ALAB) is drawing attention after rolling out its Leo CXL Smart Memory Controllers in Microsoft’s Azure M-series virtual machines, marking a first for CXL-attached memory in the public cloud. Supported by notable revenue growth and deepening relationships with major cloud customers, the company is finding new momentum in AI-driven data center technology.

See our latest analysis for Astera Labs.

Astera Labs’ momentum has been hard to ignore, with recent product wins and strong analyst mentions fueling renewed optimism. After a mid-year pullback, the stock has rebounded, posting a robust 1-year total shareholder return of 49.4% as investors bet on generative AI tailwinds and new cloud partnerships to drive both short- and long-term growth.

If Astera’s surge has you eyeing other breakthrough semiconductors and AI tech plays, it makes sense to keep exploring. See the full list for free with our See the full list for free..

With analysts divided over Astera Labs’ valuation following its rapid gains and ongoing strategic wins, the key question is whether there is still upside left for investors or if the market has already priced in the next leg of growth.

Most Popular Narrative: 21.6% Undervalued

Analysts’ most closely watched narrative sets a fair value significantly above Astera Labs’ last close. This perspective is based on accelerating revenue and profit margin expansion through strengthened relationships with hyperscale customers.

*Strong early engagement with hyperscalers and AI platform providers on open, interoperable standards like UALink (which are still in the early adoption phase with projected ramp in 2027 and beyond) enables Astera Labs to capture the industry's shift toward open, multi-vendor AI Infrastructure 2.0. This ensures exposure to significant long-term market expansion and incrementally larger addressable markets, positively impacting revenue growth rates and future margin potential as adoption accelerates.*

Want to know which staggering growth assumptions power this bullish stance? The most popular narrative is betting on transformative earnings, increasing revenues, and an improved profit margin. Discover the bold quantitative forecasts underlying such a high conviction fair value—this could be the growth formula other chipmakers aspire to.

Result: Fair Value of $196.83 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, risks remain. Astera Labs’ reliance on large hyperscale customers and potential disruption from rapid technology shifts could challenge its current growth story.

Find out about the key risks to this Astera Labs narrative.

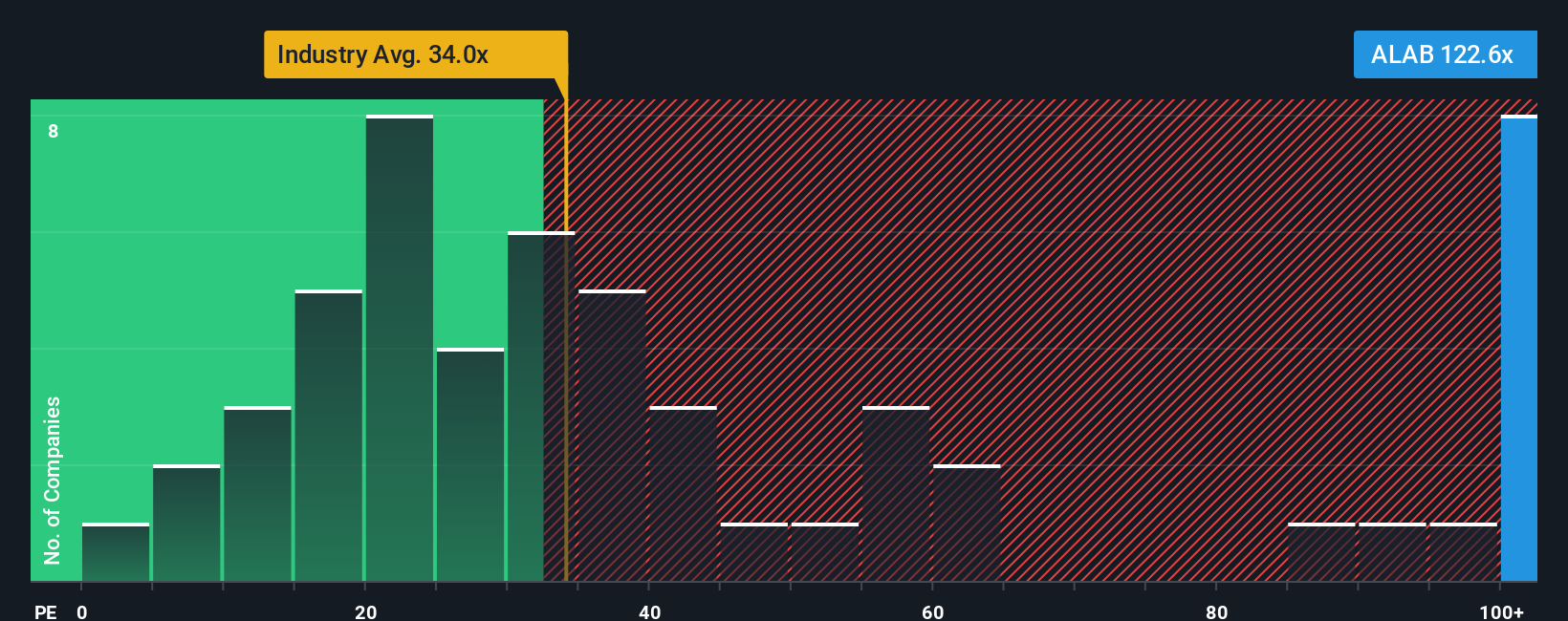

Another View: Multiples Paint a Pricier Picture

While the fair value model suggests Astera Labs is undervalued, traditional price-to-earnings analysis tells a different story. The company trades at 131x earnings, which is well above both the industry average of 35.8x and its fair ratio of 46.1x. Such a premium highlights significant valuation risk if future growth slows. Do these multiples reflect lasting demand, or is there downside if expectations reset?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Astera Labs Narrative

Not convinced by the consensus, or maybe you’d rather follow your own instincts? You can dig into the numbers and shape your own story in just minutes: Do it your way.

A great starting point for your Astera Labs research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready for Smarter Stock Picks?

Boost your odds of outperformance by using our screeners. Skip the guesswork and immediately connect with high-potential opportunities most investors never see.

- Unlock value by scanning these 922 undervalued stocks based on cash flows filled with companies trading below their fair price, offering you an opportunity to find attractive investments.

- Tap into growth by checking out these 25 AI penny stocks, which features companies advancing artificial intelligence and shaping tomorrow’s leading industries.

- Secure consistent cash flow with these 15 dividend stocks with yields > 3%, which includes options with yields above 3% for investors who want their portfolios to generate more income.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ALAB

Astera Labs

Designs, manufactures, and sells semiconductor-based connectivity solutions for cloud and AI infrastructure.

Exceptional growth potential with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative