Advertisement

- United States

- /

- Specialty Stores

- /

- NYSE:CHWY

Will Upbeat Analyst Revisions Shift Chewy's (CHWY) Growth and Expansion Narrative?

Simply Wall St

Reviewed by Sasha Jovanovic

- Chewy's stock recently gained ahead of its December 2025 earnings report, with analysts revising estimates upward for revenue and earnings growth compared to the previous year.

- Positive sentiment among analysts reflects growing confidence in Chewy’s recurring-revenue model and anticipated expansion in both customer engagement and operational efficiency.

- We'll consider how heightened optimism from positive analyst estimate revisions may influence the company's investment outlook and ongoing expansion efforts.

We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Chewy Investment Narrative Recap

For those interested in Chewy, belief in the company's ability to retain and grow its active customer base is central, especially given the weight of its recurring revenue model. While recent analyst optimism points to expected near-term growth, modest customer acquisition rates remain the biggest short-term catalyst and risk; this news does not appear to materially shift that balance, as revenue growth is still forecast to lag broader industry trends.

Among recent company moves, Chewy's launch of Get Real™ fresh dog food stands out as most relevant in the context of anticipated revenue drivers, it's an example of product expansion aimed at boosting sales per active customer and making the business less reliant on Autoship subscriptions for growth.

Yet, despite favorable revenue outlooks, investors should also be aware of the continuing risk if customers’ preferences on subscription services change or growth in new active users...

Read the full narrative on Chewy (it's free!)

Chewy's outlook anticipates $15.1 billion in revenue and $467.3 million in earnings by 2028. This projection assumes an annual revenue growth rate of 7.7% and a $79.1 million increase in earnings from the current $388.2 million.

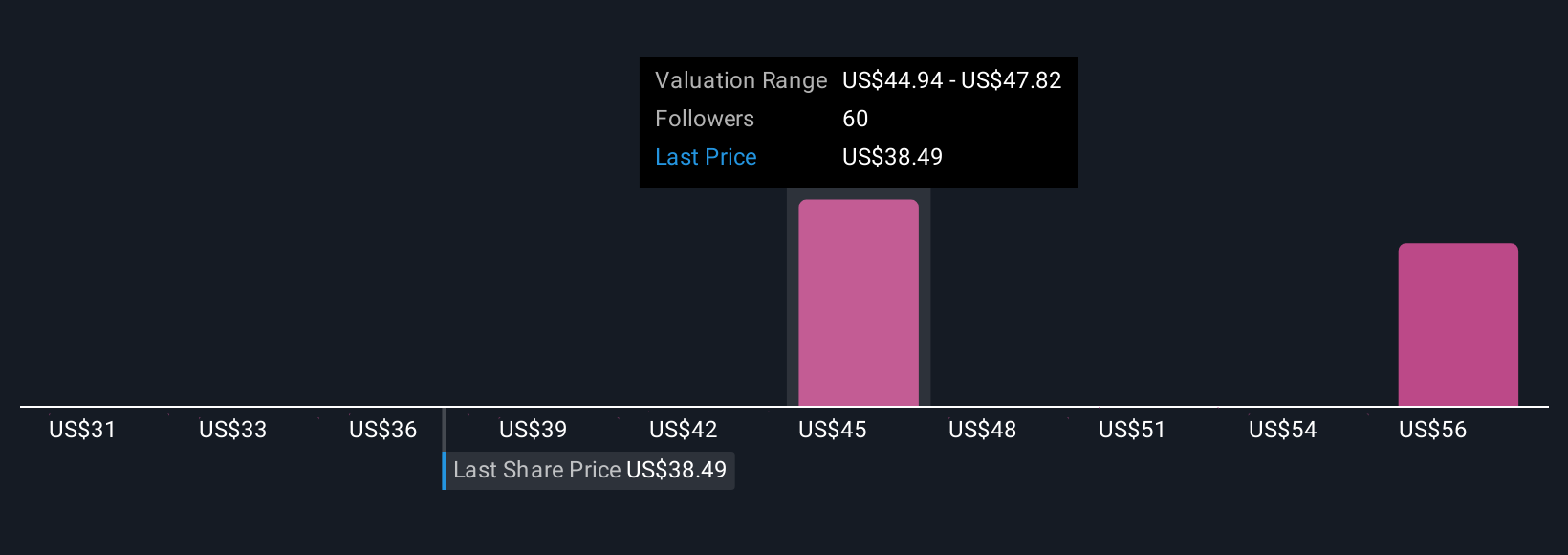

Uncover how Chewy's forecasts yield a $45.45 fair value, a 31% upside to its current price.

Exploring Other Perspectives

Seven individual fair value estimates from the Simply Wall St Community place Chewy between US$44.41 and US$59.46 per share. Many see opportunity from new offerings, but differing views reflect how much opinion varies when revenue growth comes in below sector averages.

Explore 7 other fair value estimates on Chewy - why the stock might be worth just $44.41!

Build Your Own Chewy Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Chewy research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Chewy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Chewy's overall financial health at a glance.

Looking For Alternative Opportunities?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Rare earth metals are the new gold rush. Find out which 35 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CHWY

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative