Advertisement

- United States

- /

- Specialty Stores

- /

- NYSE:BBWI

Can Bath & Body Works’ (BBWI) Holiday Discount Push Reveal More About Its Pricing Power?

Simply Wall St

Reviewed by Sasha Jovanovic

- Earlier this month, Bath & Body Works reported disappointing third quarter results and revised its 2025 full-year guidance downward, citing continued weak consumer demand and tariff pressures with expected declines in both net sales and earnings per share compared to the previous year.

- In response to consumer headwinds, the company simultaneously launched new low-cost holiday gift products and expanded promotional offerings in an effort to boost seasonal sales.

- We'll explore how Bath & Body Works’ lowered outlook, driven by soft consumer sentiment, may influence its longer-term investment narrative.

Outshine the giants: these 25 early-stage AI stocks could fund your retirement.

Bath & Body Works Investment Narrative Recap

If you are considering Bath & Body Works as an investment, the core thesis centers on the company’s ability to reinvigorate growth by reaching new customer segments and expanding its digital and distribution platforms, all while maintaining margin resilience despite external pressures. Recent downward revisions to 2025 guidance underscore the importance of restoring near-term sales momentum during key retail seasons, while margin risk, particularly from tariffs and declining consumer spending, remains at the forefront. On balance, these recent updates may affect the most important short-term catalyst, seasonal promotional performance, but do not fundamentally alter the primary longer-term risk around sustainable customer acquisition and margin management.

Among several recent announcements, the launch of new low-cost holiday gift items under current seasonal promotions is especially relevant, as it illustrates the company’s response to weaker consumer demand during critical periods. Such initiatives could have direct implications for near-term sales outcomes, putting a spotlight on how effectively Bath & Body Works can stimulate traffic and transaction volume in a tougher spending environment.

Yet, while these steps may drive short-term results, investors should be aware that underlying exposure to tariffs and shifting consumer trends still looms in the background…

Read the full narrative on Bath & Body Works (it's free!)

Bath & Body Works' outlook projects $8.1 billion in revenue and $860.7 million in earnings by 2028. This scenario requires a 3.1% annual revenue growth rate and a $132.7 million increase in earnings from the current level of $728.0 million.

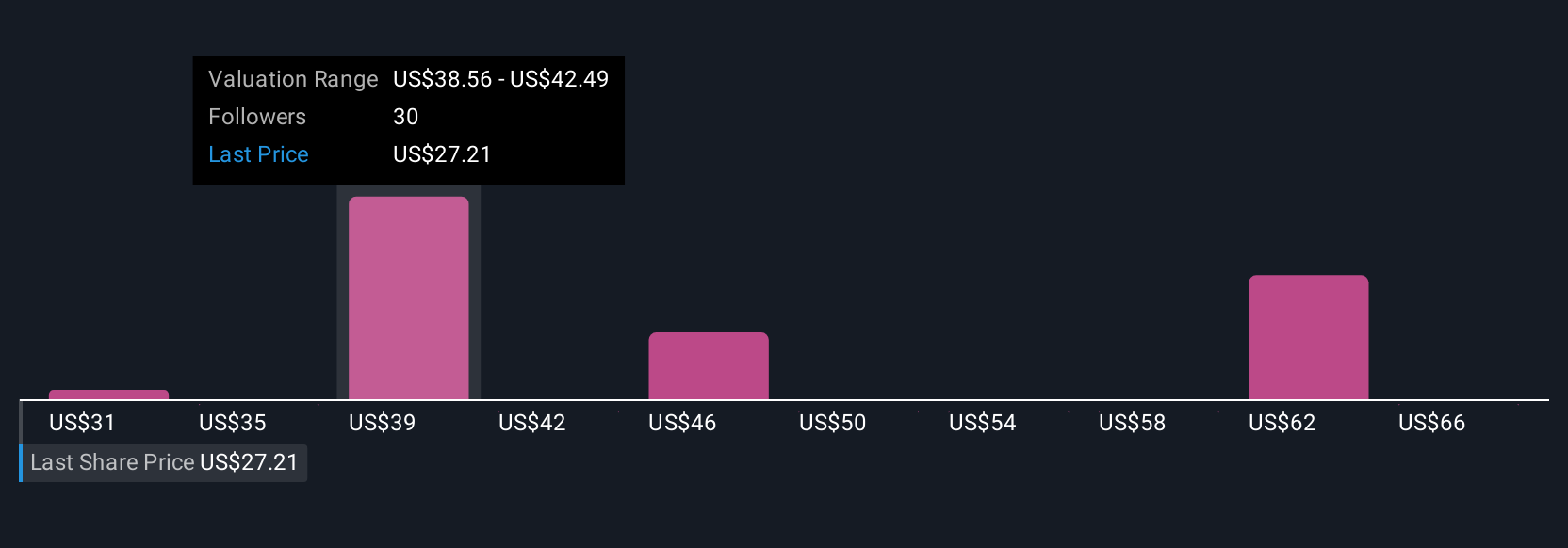

Uncover how Bath & Body Works' forecasts yield a $36.96 fair value, a 112% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members have shared 10 fair value estimates for Bath & Body Works, ranging from US$28.57 to US$64.56. While views differ widely, ongoing challenges in attracting younger shoppers and boosting digital sales remain crucial to the company's outlook and may shape where you see true value.

Explore 10 other fair value estimates on Bath & Body Works - why the stock might be worth just $28.57!

Build Your Own Bath & Body Works Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Bath & Body Works research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Bath & Body Works research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bath & Body Works' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bath & Body Works might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BBWI

Bath & Body Works

Operates as a specialty retailer of home fragrance, personal and body care, soaps, and sanitizer products.

Undervalued average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative