Advertisement

- United States

- /

- REITS

- /

- NYSE:WPC

How Recent Asset Acquisitions Impact W. P. Carey’s Valuation After a 24% Rally

Simply Wall St

Reviewed by Bailey Pemberton

- Ever wondered if W. P. Carey’s recent momentum means it’s a good time to buy or if you’d be paying too much? You’re not alone, and there’s more beneath the surface than the headline price suggests.

- W. P. Carey’s stock has climbed steadily, up 0.4% over the past week and 24.1% year-to-date, with a strong 25.2% gain in the last 12 months. This hints at renewed market optimism or a shift in risk perception.

- Recent headlines have focused on W. P. Carey’s strategic asset acquisitions and portfolio refinements. Analysts say these moves could enhance cash flow stability in an uncertain market. The dealmaking activity appears to be influencing investor sentiment and driving the share price higher.

- If you look at the valuation scorecard, W. P. Carey clocks in at 2 out of 6 for undervaluation checks. This is solid but not spectacular, and definitely worth a closer look. We’ll dig into traditional valuation methods next, so stay tuned for an even smarter approach to finding fair value by the end of this article.

W. P. Carey scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: W. P. Carey Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s true worth by projecting its adjusted funds from operations into the future, and then discounting those expected cash flows back to today’s dollars. This helps investors understand what the business is fundamentally worth, regardless of current market swings.

W. P. Carey currently generates free cash flow of just over $1 billion annually. Analysts forecast steady growth, with projections reaching around $1.37 billion by the end of 2028. Beyond the first five years, cash flow estimates rely on long-term trends and moderate growth assumptions, pushing projected free cash flow to approximately $1.91 billion in 2035.

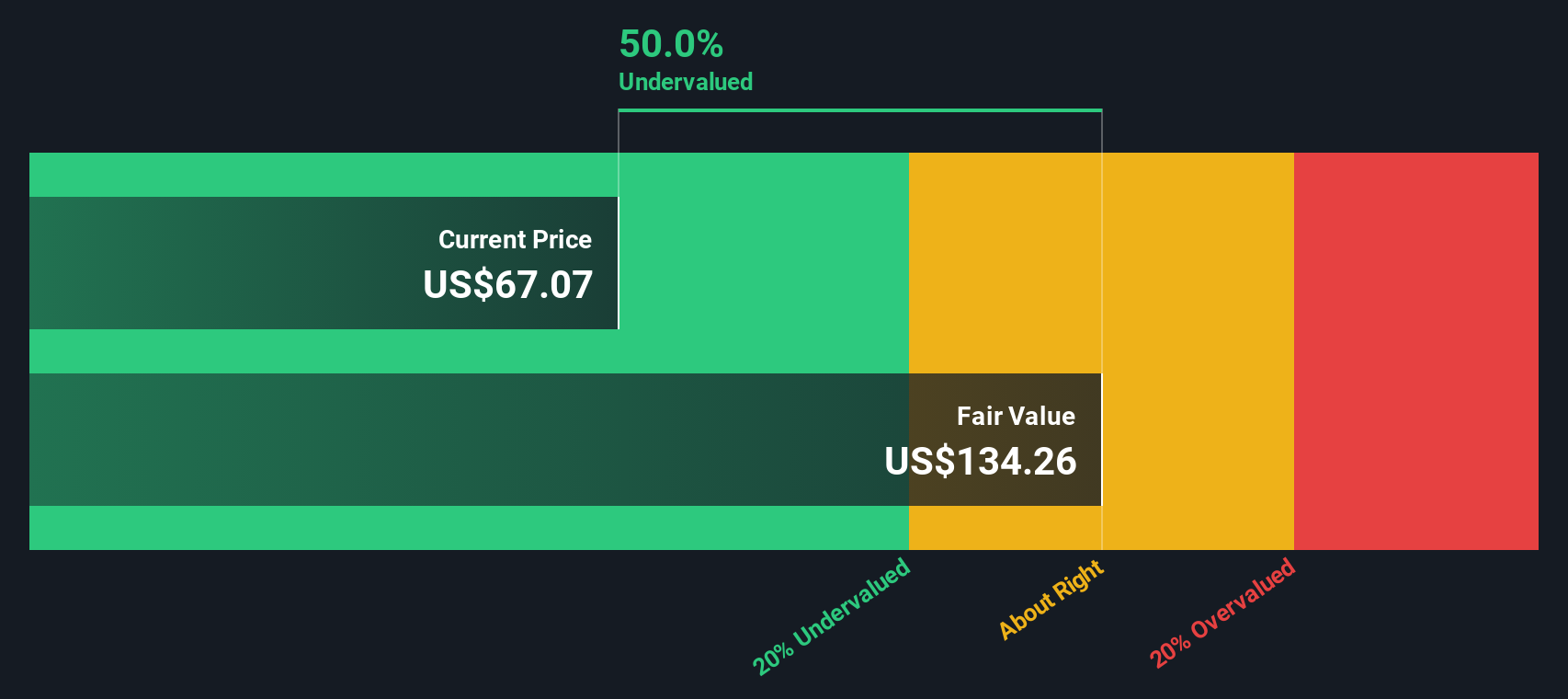

By discounting these future cash flows to the present, the DCF calculation lands on an estimated fair value of $150.56 per share. Given the latest trading price, this implies the stock is trading at a 55.3% discount to its intrinsic value, representing a significant margin of safety in today’s market.

For investors seeking value, this DCF suggests that W. P. Carey may represent an opportunity worth further investigation.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests W. P. Carey is undervalued by 55.3%. Track this in your watchlist or portfolio, or discover 920 more undervalued stocks based on cash flows.

Approach 2: W. P. Carey Price vs Earnings

The price-to-earnings (PE) ratio is one of the most widely used valuation tools for profitable companies like W. P. Carey. It compares a company’s current share price to its earnings per share, offering an accessible snapshot of how much investors are willing to pay for a dollar of profits.

Growth expectations and risk play a big role in setting what is considered a “normal” or “fair” PE ratio. Fast-growing, lower-risk companies usually justify higher PE ratios, while those with slower growth or higher risk trade at lower multiples.

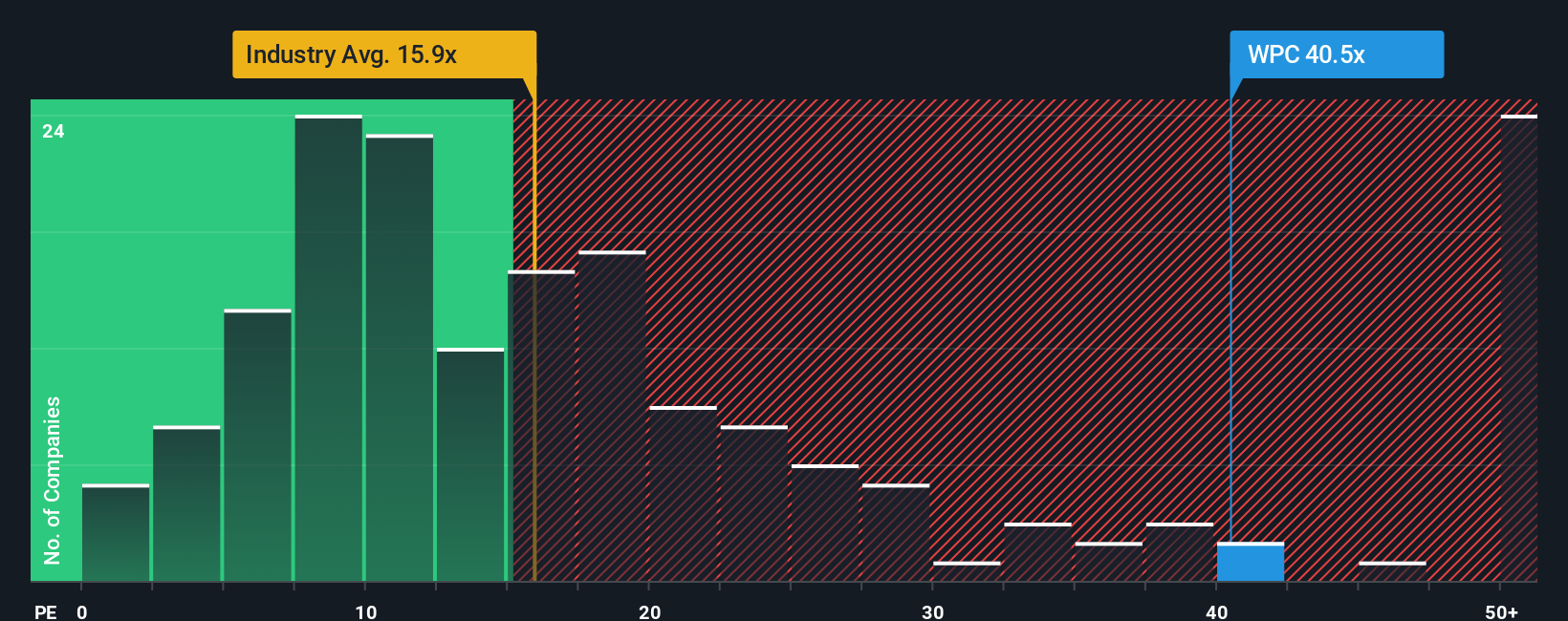

W. P. Carey currently trades at a PE ratio of 40.44x. For context, this is above the peer average of 29.28x and much higher than the REITs industry average of 16.04x. At first glance, this might suggest the stock is expensive relative to the broader sector and its direct competitors.

This is where Simply Wall St’s Fair Ratio comes in. The Fair PE Ratio for W. P. Carey is 39.30x, reflecting an in-depth assessment of the company’s growth, profit margins, risk, industry, and scale. Unlike a simple industry or peer comparison, the Fair Ratio reveals a more nuanced estimate of what investors should reasonably pay for the company’s earnings, factoring in its unique strengths and challenges.

With the current PE ratio just slightly above the Fair Ratio, W. P. Carey appears to be priced about right based on this approach. It is neither obviously cheap nor excessively expensive, suggesting the market is factoring in the company’s prospects quite efficiently at the moment.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your W. P. Carey Narrative

Earlier we mentioned there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your way of telling a broader story behind the numbers, combining your expectations for W. P. Carey’s future revenue, earnings, and profit margins with your unique perspective on the company’s business outlook.

Rather than relying solely on ratios or consensus figures, Narratives help you connect your understanding of W. P. Carey’s strategy, industry trends, and market risks directly to a dynamic financial forecast and a personally justified fair value. This transforms the investing process. Your view on catalysts, risks, and future growth shapes the valuation you use to decide when to buy or sell.

Narratives are easy to use and accessible on Simply Wall St’s Community page, where millions of other investors share their own stories and fair value estimates. When new news or earnings updates appear, Narratives update automatically, ensuring your view stays relevant and actionable.

For example, some investors may see W. P. Carey’s international diversification and industrial pivot supporting a bullish $75 price target, while others focus on tenant quality risks and limited upside, justifying a more cautious $60 view. With Narratives, you can evaluate both sides, compare Fair Value to the current price, and make confident decisions based on your own investment story.

Do you think there's more to the story for W. P. Carey? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if W. P. Carey might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WPC

W. P. Carey

W. P. Carey ranks among the largest net lease REITs with a well-diversified portfolio of high-quality, operationally critical commercial real estate, which includes 1,600 net lease properties covering approximately 178 million square feet and a portfolio of 66 self-storage operating properties as of June 30, 2025.

Moderate growth potential second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative