Advertisement

- United States

- /

- Specialized REITs

- /

- NYSE:MRP

Are Recent Strategic Partnership Rumors a Signal to Revisit Millrose Properties’ Valuation in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Millrose Properties could be a hidden gem or just another overvalued name on the NYSE? You are not alone. Savvy investors know that true value is more than just a stock price.

- The stock has climbed an impressive 38.8% year-to-date, though it has recently come off its highs with a 5.1% drop over the last month. This kind of movement catches the eye, whether you are chasing momentum or wary of shifting risk.

- Recent headlines have put Millrose Properties in the spotlight, with analysts and market commentators noting increased institutional activity and hints of strategic partnerships. These stories are fueling both optimism about long-term prospects and speculation about what might come next.

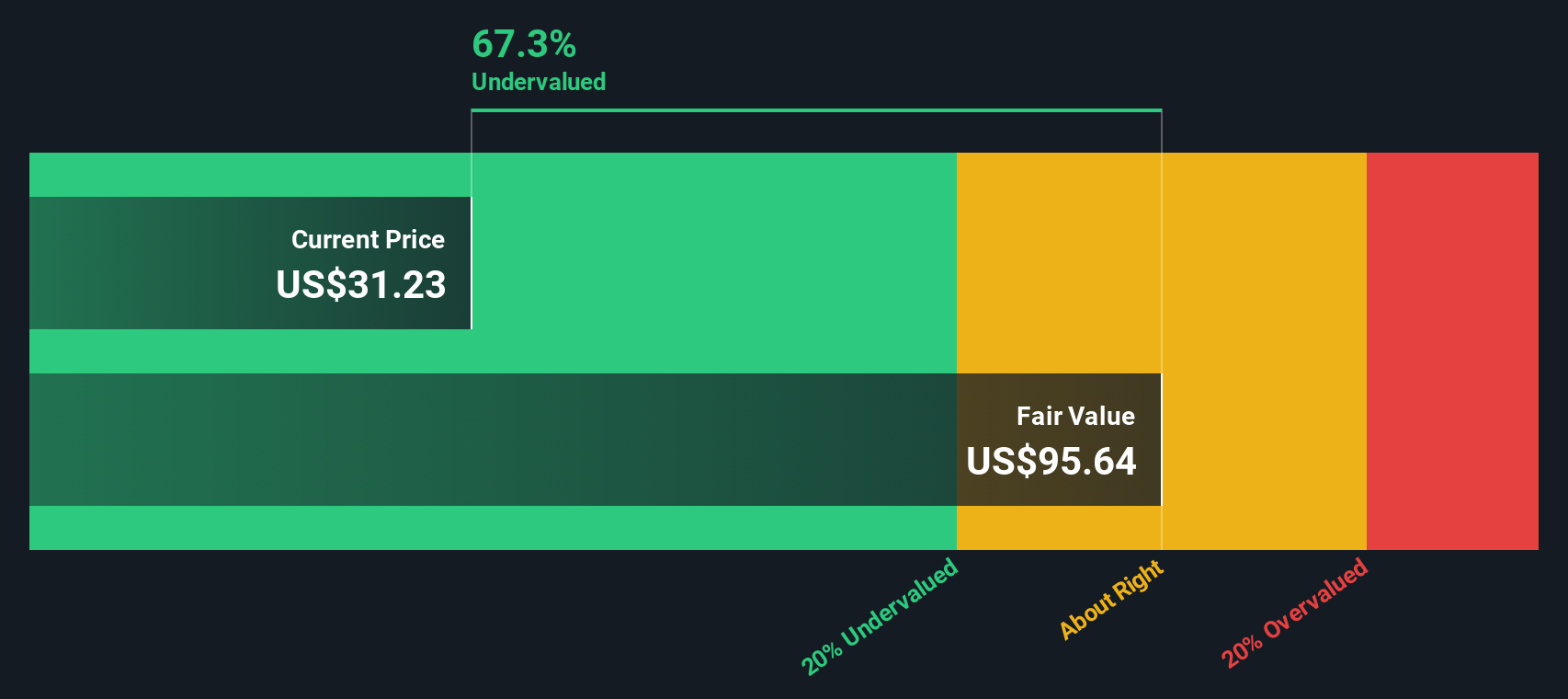

- When it comes to the numbers, Millrose Properties racks up a value score of 5 out of 6 on key valuation checks, signaling it is undervalued in most areas measured. In the next section, we will break down what drives this score across different valuation methods and, even more importantly, introduce an approach that goes beyond the usual models to truly understand the company’s potential.

Approach 1: Millrose Properties Dividend Discount Model (DDM) Analysis

The Dividend Discount Model (DDM) values a stock by projecting the stream of future dividends and discounting them back to their present value. This approach is especially relevant for companies like Millrose Properties, where dividends play a central role for investors seeking reliable income.

For Millrose Properties, the model uses a current dividend per share of $2.90. However, the payout ratio stands at an unsustainably high 106.6%, meaning the company is paying out more in dividends than it earns. The return on equity is negative at -2.41%, which reflects ongoing profitability challenges. Given these factors, the projected long-term dividend growth is virtually flat, calculated at only 0.16% annually.

Despite the weak underlying metrics, the DDM estimates Millrose Properties’ intrinsic value at $37.27 per share. This suggests the stock is 18.3% undervalued relative to its current share price. This significant discount may indicate that the market is underestimating the company’s ability to sustain its dividend or address its negative returns.

Result: UNDERVALUED

Our Dividend Discount Model (DDM) analysis suggests Millrose Properties is undervalued by 18.3%. Track this in your watchlist or portfolio, or discover 920 more undervalued stocks based on cash flows.

Approach 2: Millrose Properties Price vs Earnings

The Price-to-Earnings (PE) ratio is a widely used valuation metric for profitable businesses. It reflects how much investors are willing to pay for each dollar of company earnings. For companies like Millrose Properties that generate positive net income, PE provides a simple way to compare market pricing to actual profitability.

Growth expectations and company-specific risks play an important role in whether a “normal” PE ratio is high or low. A firm with robust earnings growth or lower perceived risk generally justifies a higher PE, while slow growth or higher risk pulls it down. Against this backdrop, Millrose Properties currently trades at a PE ratio of 23.33x. This is just under the peer average of 24.01x and sits notably above the Specialized REITs industry average PE of 17.20x.

To go beyond surface-level comparisons, Simply Wall St’s “Fair Ratio” is used in this case, a 61.62x PE. This proprietary metric sharpens the analysis by factoring in the company’s unique growth outlook, profitability, risk profile, market cap, and industry context. It reveals what a justified multiple should look like for Millrose Properties. While industry averages and peer multiples provide a quick reference, the Fair Ratio draws on deeper fundamentals, making it a more relevant standard for fair value.

With a Fair Ratio of 61.62x well above the current PE of 23.33x, the data strongly suggests that Millrose Properties is undervalued based on its earnings potential and risk-adjusted profile.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Millrose Properties Narrative

Earlier we mentioned there is an even better way to understand valuation. Let’s introduce you to Narratives. A Narrative is a story you create behind the numbers; you bring your own perspective to what you think Millrose Properties is worth by forecasting future revenue, earnings, and margins. Narratives connect the company’s story to a financial forecast and then to a calculated fair value, turning raw data into actionable insights.

On Simply Wall St’s platform, millions of investors use Narratives from the Community page to easily compare their stories and assumptions with others. Narratives provide a smarter, more flexible approach to investing, helping you decide when to buy or sell by comparing your Fair Value to the current Price. They also adapt automatically as new news or earnings are released. For example, one investor may expect Millrose Properties to outperform and estimate a fair value 40% above the current price, while another, more cautious Narrative might predict just a 5% gain. Narratives put the story and the decision power in your hands, making investment strategies clearer and more personal than ever.

Do you think there's more to the story for Millrose Properties? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MRP

Millrose Properties

Millrose purchases and develops residential land and sells finished homesites to homebuilders by way of option contracts with predetermined costs and takedown schedules.

Undervalued with high growth potential.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative