Advertisement

- United States

- /

- Industrial REITs

- /

- NYSE:EGP

EastGroup Properties (EGP) Valuation After New ATM Equity Program, Shelf Registration and Fresh Term Loans

Simply Wall St

Reviewed by Simply Wall St

EastGroup Properties (EGP) just rolled out a new at the market equity program and shelf registration alongside fresh term loans, giving the industrial REIT more flexibility to fund projects, manage debt, and respond to mixed analyst sentiment.

See our latest analysis for EastGroup Properties.

The new equity program and term loans land after a solid run, with EastGroup’s 90 day share price return of 9.09% and five year total shareholder return of 55.86% suggesting momentum remains constructive despite recent mixed analyst calls.

If these capital moves have you thinking about where else growth and confidence might line up, it could be worth exploring fast growing stocks with high insider ownership next.

With shares already near record highs and trading at only a modest discount to analyst targets, the key question now is whether EastGroup still offers hidden value or if the market has fully priced in its next leg of growth.

Most Popular Narrative: 7.2% Undervalued

With EastGroup closing at $179.91 against a narrative fair value of roughly $193.84, the story leans toward moderate upside driven by earnings resilience.

Management's strong balance sheet, ample land bank, and ability to accelerate development starts when demand rebounds ensures the company can capitalize early on secular demand trends, translating to scalable FFO growth and further upside in earnings as market sentiment normalizes.

Want to see what powers this upside case? The narrative leans on steady growth, firmer margins, and a future earnings multiple usually reserved for market darlings. Curious which assumptions really move that valuation?

Result: Fair Value of $193.84 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upside case could unravel if industrial leasing slows further, or if higher for longer rates squeeze development returns and compress valuation multiples.

Find out about the key risks to this EastGroup Properties narrative.

Another Angle on Valuation

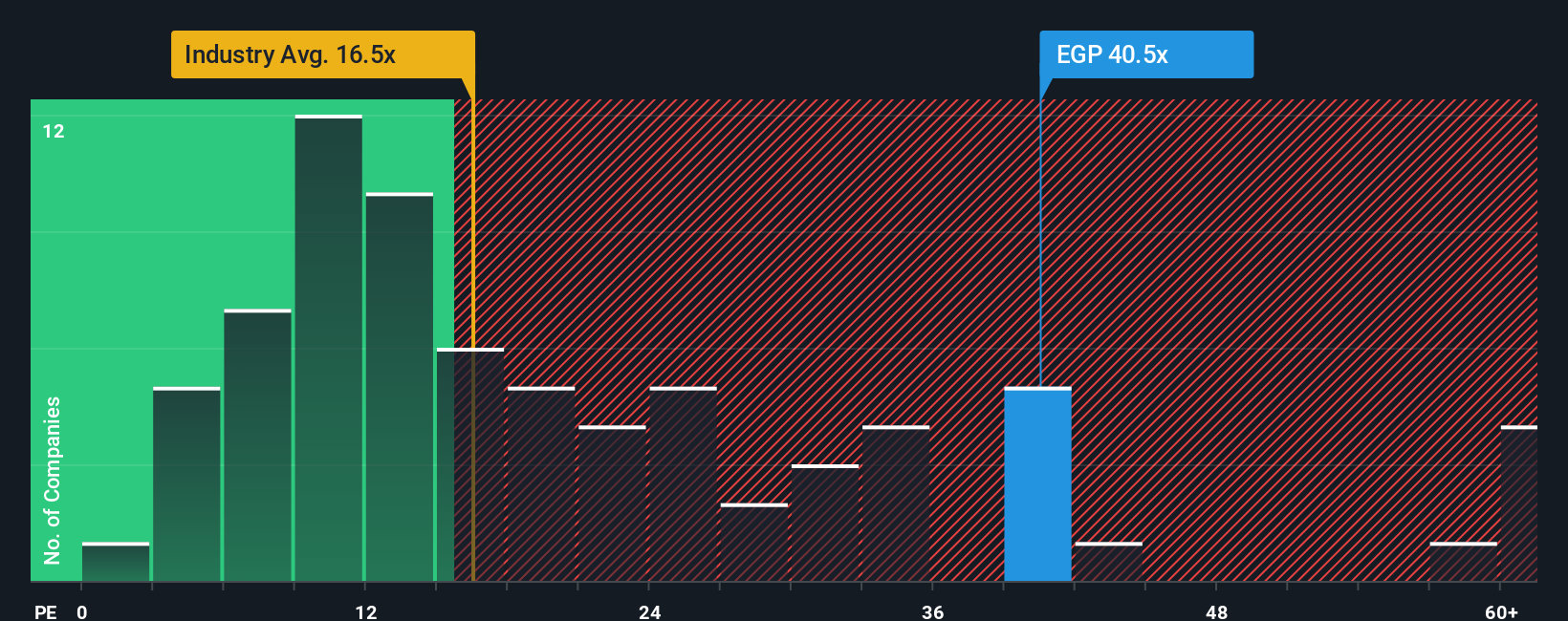

While the narrative fair value pegs EastGroup as roughly 7 percent undervalued, its price to earnings ratio of 38.6 times tells a tougher story. This multiple is well above the global Industrial REITs average of 15.9 times and a fair ratio of 33.5 times, which hints at less margin for error than the upside case suggests.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own EastGroup Properties Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a custom view in minutes with Do it your way.

A great starting point for your EastGroup Properties research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Before you move on, explore a few additional opportunities by scanning focused stock ideas from the Simply Wall Street Screener, tailored to different strategies and risk levels.

- Look for higher potential returns by targeting out of favor businesses that still generate strong cash flows using these 905 undervalued stocks based on cash flows as your hunting ground for potentially mispriced quality.

- Gain exposure to innovation by reviewing these 26 AI penny stocks, which covers companies using artificial intelligence in ways that may reshape industries and earnings profiles.

- Support your income-focused approach by considering these 15 dividend stocks with yields > 3%, which highlights stocks that combine dividend yields with financial characteristics often associated with more sustainable payouts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if EastGroup Properties might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:EGP

EastGroup Properties

EastGroup Properties, Inc. (NYSE: EGP), a member of the S&P Mid-Cap 400 and Russell 2000 Indexes, is a self-administered equity real estate investment trust focused on the development, acquisition and operation of industrial properties in high-growth markets throughout the United States with an emphasis in the states of Texas, Florida, California, Arizona and North Carolina.

Established dividend payer with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

66 followersusers have followed this narrative

7 commentsusers have commented on this narrative

20 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.9% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

EN

Enemy on Halyk Bank of Kazakhstan ·

Halyk Bank of Kazakhstan will see revenue grow 11% as their future PE reaches 3.2x soon

Fair Value:US$52.2351.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Magma Silver ·

Silver's Breakout to over $50US will make Magma’s future shine with drill sampling returning 115g/t Silver and 2.3 g/t Gold at its Peru Mine

Fair Value:CA$0.3534.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on SEGRO ·

SEGRO's Revenue to Rise 14.7% Amidst Optimistic Growth Plans

Fair Value:UK£9.3924.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

958 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

66 followersusers have followed this narrative

7 commentsusers have commented on this narrative

20 likesusers have liked this narrative