Advertisement

- United States

- /

- Life Sciences

- /

- NYSE:WST

West Pharmaceutical Services (WST): Evaluating Valuation After Recent Momentum Shift

Simply Wall St

Reviewed by Simply Wall St

West Pharmaceutical Services (WST) has been under the spotlight as investors track its stock movement over the past month. Shares have seen a slight dip, even as the broader pharmaceutical sector continues to attract attention.

See our latest analysis for West Pharmaceutical Services.

Momentum for West Pharmaceutical Services appears to be fading a bit, with shares posting a one-year total shareholder return of -13.8%. This comes even after a solid 13.8% share price gain in the last 90 days. The latest stretch suggests that recent optimism is giving way to a more cautious outlook, as the market reassesses growth prospects and risk levels following a long period of expansion.

If you’re looking for other compelling opportunities in the healthcare space, check out the full list of innovators in our See the full list for free..

With shares trading well below analyst price targets and recent momentum stalling, the big question remains: is West Pharmaceutical Services undervalued at these levels, or is the market accurately reflecting its future prospects?

Most Popular Narrative: 21% Undervalued

West Pharmaceutical Services' current consensus narrative suggests that the stock is trading significantly below what analysts believe is its fair value. With a fair value estimate much higher than the last closing price, the story hinges on several potential catalysts driving future gains.

The continued growth in GLP-1s, which made up about 7% of total revenues in the first quarter, and the company's ability to capitalize on significant opportunities in this market could drive revenue and earnings growth. The introduction of an automated line for HVP delivery devices later in 2025 to early 2026 is expected to improve margins by driving operational efficiencies and scale, enhancing net margins.

Want to see the engine behind this bullish outlook? The narrative features ambitious financial projections and confidence in margin expansion, but not everything is as it seems. The numbers driving this fair value will catch most investors off guard. Check out how these bold assumptions fuel the optimistic price target.

Result: Fair Value of $350.77 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, ongoing executive changes and evolving demand for HVP components could pose real challenges. These factors could potentially derail the current upbeat narrative among analysts.

Find out about the key risks to this West Pharmaceutical Services narrative.

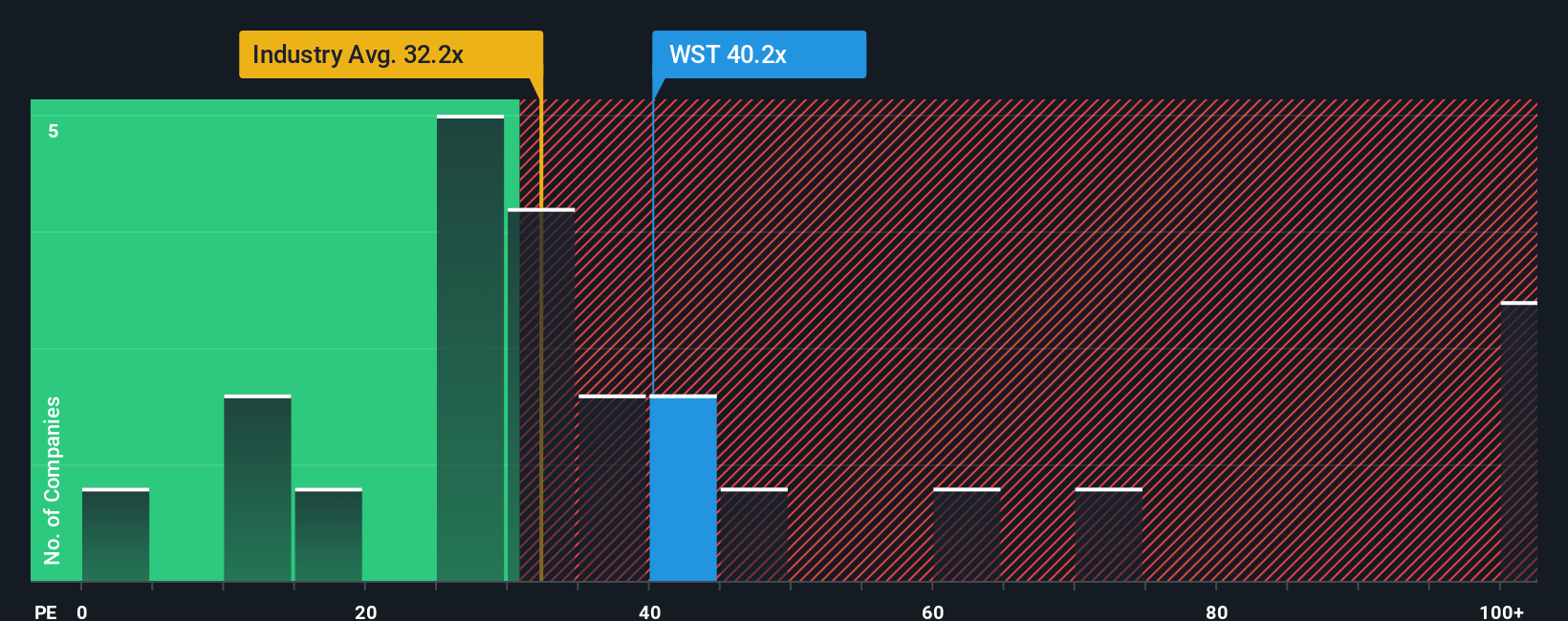

Another View: Valuation Based on Price-to-Earnings

Looking at valuation using the price-to-earnings ratio, West Pharmaceutical Services trades at 40.6x, which is well above both the North American industry average of 37.2x and the peer average of 31.3x. The company’s fair ratio, or what the market could move toward, sits even lower at 25.2x. This sizable gap highlights valuation risk; if market sentiment shifts or growth slows, shares could potentially rerate much lower. Does this premium indicate long-term confidence, or is there hidden downside?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own West Pharmaceutical Services Narrative

If you see things differently or want to challenge the consensus, it is quick and easy to build your own perspective in just a few minutes. Do it your way

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding West Pharmaceutical Services.

Looking for More Smart Investment Moves?

Momentum is not just for individual stocks. You can capitalize on emerging trends across the market. Uncover investment opportunities that others might overlook with these handpicked ideas below.

- Tap into massive potential by targeting value plays through these 919 undervalued stocks based on cash flows which is built exclusively around strong cash flows and attractive pricing.

- Capture future growth with these 25 AI penny stocks to connect with companies at the forefront of artificial intelligence innovation and disruption.

- Accelerate your search for reliable, income-generating assets by checking out these 15 dividend stocks with yields > 3% offering robust yields above 3% for long-term stability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if West Pharmaceutical Services might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WST

West Pharmaceutical Services

Designs, manufactures, and sells containment and delivery systems for injectable drugs and healthcare products in the Americas, Europe, the Middle East, Africa, and the Asia Pacific.

Flawless balance sheet with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

NI

niteco on Texas Instruments ·

Engineered for Stability. Positioned for Growth.

Fair Value:US$314.4446.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$28.1829.5% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

Bejgal on Fiverr International ·

Fiverr International will transform the freelance industry with AI-powered growth

Fair Value:US$36.8143.1% undervalued

79 followersusers have followed this narrative

7 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

109 followersusers have followed this narrative

10 commentsusers have commented on this narrative

21 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

939 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

145 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative