Advertisement

- United States

- /

- Pharma

- /

- NYSE:PFE

Does the Recent 3.3% Rally Change the Picture for Pfizer’s True Value?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Pfizer’s current share price truly reflects its value? You’re not alone, and now might be the perfect time to dig into what the numbers are telling us.

- After a steady 3.3% gain this past week and 3.8% over the past month, Pfizer's stock is showing some signs of positive momentum, even though year-to-date performance remains a modest -3.4%.

- Recent headlines highlight regulatory developments and ongoing progress in Pfizer’s drug pipeline, both of which have fueled some renewed interest among investors. Partnerships and strategic announcements continue to keep the stock in the news and add context to the recent price movement.

- On our value score, Pfizer lands a 5 out of 6. This reflects that it appears undervalued on nearly every major metric right now. Next, let’s break down the valuation story using a few common methods. Stick around for what might just be the smartest way to assess fair value at the end.

Find out why Pfizer's 6.7% return over the last year is lagging behind its peers.

Approach 1: Pfizer Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by projecting its future cash flows and then discounting them back to today’s dollars. This method aims to answer what a business is worth based on its capacity to generate cash in the future.

For Pfizer, the DCF model uses a two-stage Free Cash Flow to Equity approach. Currently, Pfizer generates annual Free Cash Flow of approximately $9.95 Billion. Analyst-driven forecasts extend out five years, predicting steady growth, after which Simply Wall St extrapolates further. By 2029, projected Free Cash Flow is expected to rise to about $16.31 Billion, highlighting Pfizer’s continued earnings strength.

Using all these cash flow projections, the model estimates Pfizer's fair value at $62.11 per share. Compared to the stock’s current trading price, this figure implies Pfizer is trading at a 58.6 percent discount to intrinsic value, which indicates the stock may be undervalued by the market at this time.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Pfizer is undervalued by 58.6%. Track this in your watchlist or portfolio, or discover 927 more undervalued stocks based on cash flows.

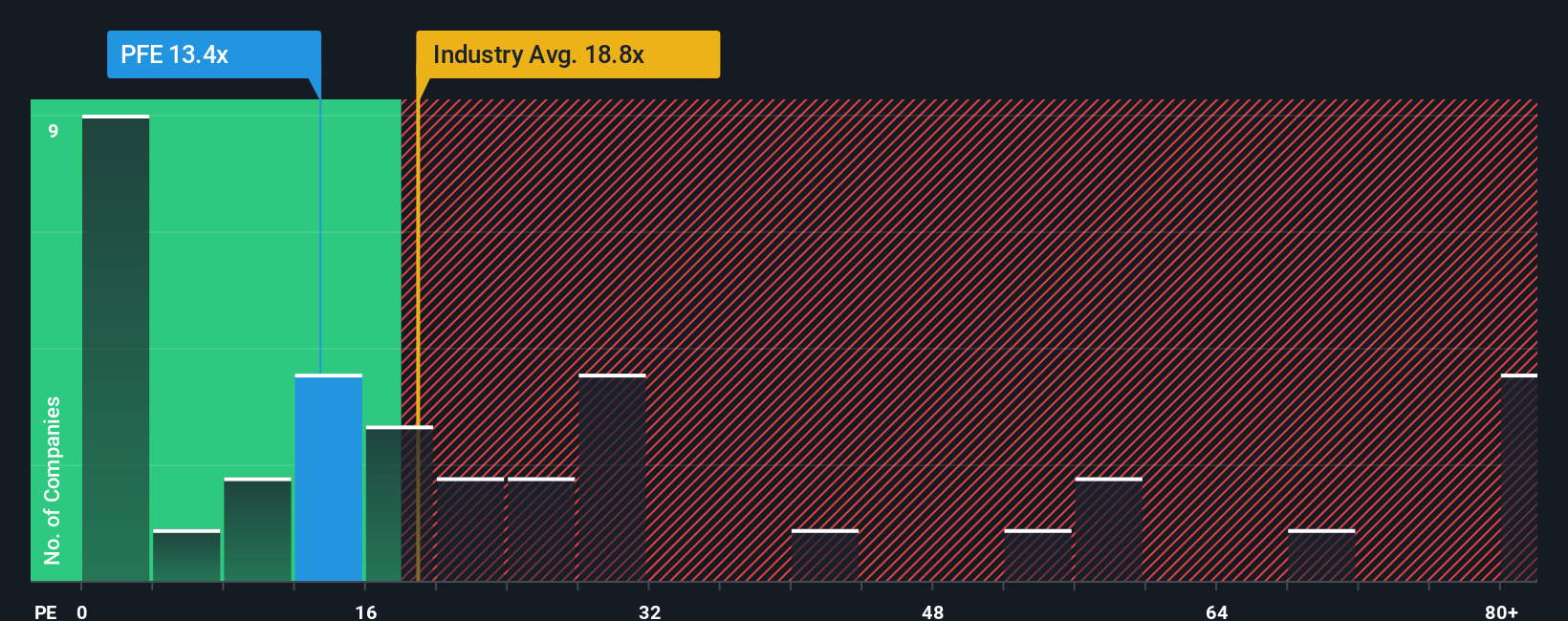

Approach 2: Pfizer Price vs Earnings

The Price-to-Earnings (PE) ratio is the preferred valuation tool for profitable companies because it captures how much investors are willing to pay for each dollar of earnings. It is especially useful when a business like Pfizer is generating steady profits, making it easier to compare valuation across companies and industries.

Importantly, a “normal” or “fair” PE ratio depends on two big factors: how fast a company is expected to grow, and how risky that growth is. Companies with stronger growth prospects or less risk typically deserve a higher multiple, while lower growth or more uncertainty pulls it down.

Pfizer currently trades at a PE of 14.9x. For context, the Pharmaceuticals industry average PE is 20.6x, and closest peers sit at 17.8x. This suggests Pfizer may be conservative relative to many industry names. However, there is more to the story than just comparing with averages.

This is where Simply Wall St’s “Fair Ratio” comes in. For Pfizer, the Fair Ratio is 24.2x. The Fair Ratio uses a combination of expected earnings growth, profitability (profit margin), risk, industry dynamics, and company size to calculate the PE ratio that truly makes sense for Pfizer’s current position.

Unlike broad averages, the Fair Ratio is tailored and forward-looking. It helps investors cut through generic sector benchmarks by considering factors that matter specifically to Pfizer, which provides a much clearer picture of value.

Comparing Pfizer’s actual PE of 14.9x with its Fair Ratio of 24.2x, Pfizer appears attractively priced at a significant discount to where it should be valued based on its fundamentals.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1433 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Pfizer Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. Narratives are powerful, accessible tools that let you define your own story for a company, connecting your views on its future prospects, such as revenue growth, profit margins, and fair value, to real financial forecasts.

Instead of just relying on static numbers or broad analyst consensus, Narratives allow you to integrate your personal perspective with financial data, providing a transparent path from your story of the business to a calculated fair value. This approach is available to millions of investors on the Simply Wall St Community page, making it easy for anyone to create, customize, and revisit investment cases as new information arises.

What makes Narratives especially compelling is their dynamic nature. They automatically update forecasts and fair value estimates whenever significant news, earnings, or company changes are detected, ensuring your view stays current. Narratives empower investors to decide when to buy, hold, or sell by comparing their own Fair Value outputs to the live stock Price, rather than being limited to one-size-fits-all analyses.

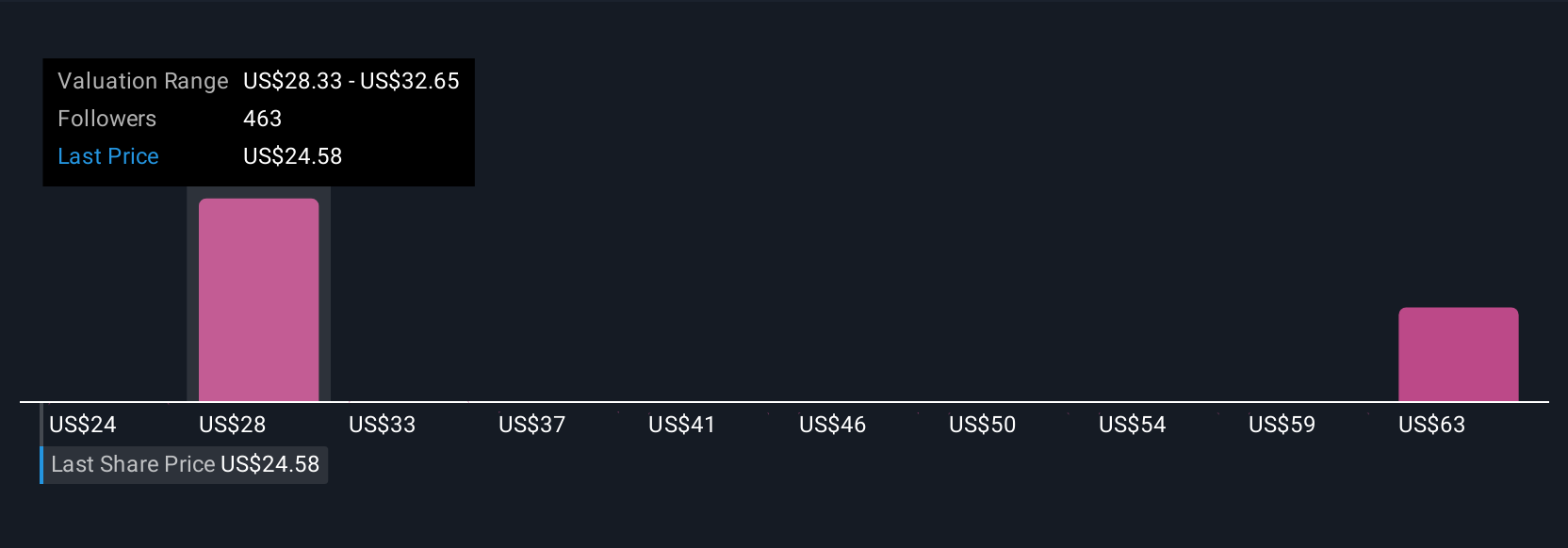

For example, some Pfizer investors currently see a fair value near $36 per share, banking on rapid growth from new therapies and emerging markets, while others are more cautious, valuing the stock closer to $24 due to regulatory and patent risks. Your Narrative can and should reflect what you believe is most likely.

For Pfizer, we'll make it really easy for you with previews of two leading Pfizer Narratives:

- 🐂 Pfizer Bull Case

Fair Value: $29.08

Current Price vs. Fair Value: 11.6% undervalued

Projected Revenue Growth (next 3 years): -2.66%

- Pfizer is positioned for long-term growth through late-stage pipeline expansion, business development, and increasing focus on innovative therapies and emerging markets.

- Ongoing digitalization and targeted growth in emerging markets are expected to drive operational efficiency, margin improvement, and revenue opportunities.

- Risks include regulatory pressures, patent expirations, and mounting competition. Analysts expect improved margins and a price target moderately above the current level.

- 🐻 Pfizer Bear Case

Fair Value: $24.00

Current Price vs. Fair Value: 6.9% overvalued

Projected Revenue Growth (next 3 years): -4.21%

- Revenue growth is expected to remain under pressure due to drug pricing negotiations, regulatory reforms, and significant upcoming patent expirations.

- Reliance on new R&D assets to offset aging blockbuster drugs creates significant risk if innovation does not keep pace with lost exclusivity and competitive threats.

- Despite investments in innovation and operational efficiency, the bearish cohort sees limited upside and believes the current share price is somewhat above fair value based on cautious long-term assumptions.

Do you think there's more to the story for Pfizer? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PFE

Pfizer

Pfizer Inc. discovers, develops, manufactures, markets, distributes, and sells biopharmaceutical products in the United States and internationally.

Undervalued with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

76 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

45 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative